I agree with you on the importance of growth. Growth is an important determinant of P/E; not to forget, Risk is another important determinant. The discount rate (risk including corporate governance) and growth both jointly determine the P/E multiple.It is a subjective call whether SKS or Satin has higher risk.

1 Like

Religare has a negative view on MFI sector in its Aug 15 report but holds 3% stake in Satin…funny!

1 Like

Best part is people quote Religare report and half baked mint article to express their bearish view ![]()

6 Likes

2 Likes

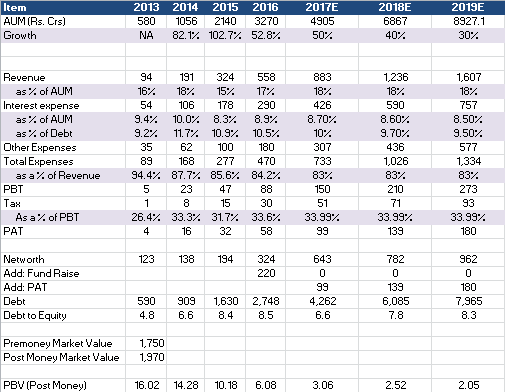

Here’s a basic analysis of the financials.

Have assumed an AUM growth rate of 50%, tapering down to 30% in 2019. PBV has been calculated assuming a 220 Cr fund raise this fiscal. After today’s run up, the stock is available at 2.5x FY18E BV. Looks like all short to medium term triggers/positives are fairly priced in (even a possible above expectations Q1).

Disc: Invested, with ~20% portfolio

2 Likes

- I would assume another equity raise in FY18 given teh growth so BV would be higher

- If you are in March 2017 and looking at FY18 2x FY18/BV for 40%+ growth and 20%+ ROE business is too low - one could pay 4x. While valuations are hard to argue, I would just compare them to other NBFC’s and easily justify 4x

Just a thought- would you also want to look at the RoAs, given that most of this high RoE is due to the over leveraged position of the MFI. SKS, Equitas, and Ujjivan all have a Debt to Equity of 3-4 times.

1 Like

I would look at ROE’s. Lower leverage gets offset by higehr ROA’s owing to higher NIM’s as cost of funding from equity is zero.

ROA is also an important parameter. Satin’s ROA of 2.2%, though lower than SKS microfinance, is as good as most of the banks and Housing Finance Companies.

Good to see your estimation.

I think you have not factored operating leverage benefit. As scale of operation increases, cost to income ratio would come down and profit would be much higher than your projections.

Thanks for the feedback. At the moment I have assumed it to be 83% (ie total expenses including interest expenses as a % of revenue). But you are right, massive operating leverages will kick in as average ticket sizes increases and loan disbursement per branch/employees increases. This number should be scaled down gradually (interest itself is coming down by 0.5% in the model). If I assume it to be 82% this year and 80% next year, the FY18 PBV works out to 2.43 (on a premoney market cap of 1,750 Crs; but the stock is now trading at ~1,950 Crs premoney, so thats 2.67x)

Today, MORGAN STANLEY ASIA (SINGAPORE) PTE bought 3,23,000 shares at 579.48.

4 Likes

Hold Satin from 300 levels and the 5-20% moves every other day is difficult to understand. Also don’t like the kind of growth expectations that are getting priced in at current levels by the market and any slow-down on those growth rates (along with stable credit quality) will be punished badly.

Disc: 5% of portfolio

Hi Gurjot - I am curious. If you are so uncomfortable with valuations, why still hold?

Also could you quantify what do you think market is factoring ion on growth in your view? And why is it uncomfortable. For context would be intesting vs SKS mgmt commenst in MFI thread which suggests Satin can grow even ahead of SKS owing to smaller base and North exposure:

SKS Mgmt:

Strong growth to continue - 50% CAGR for next 2 years and 35% CAGR on 5 year basis is the target. This will be driven by 15-20% CAGR in Ticket size growth and 25-30% CAGR from newer customer.

Next set of growth will come from northern states like UP, Bihar and even Orissa. Southern states are mostly saturated now.

I’ve learnt the hard way that over-valuation (this is extremely subjective and I’m only talking about my opinion) is never the right reason to sell a good business. Should only sell when the investment thesis is no longer valid (in Satin’s case, big slowdown in growth or asset quality deterioration). Plus, the re-investment risk is too high in this market i.e. finding good businesses with a decent margin of safety.

An example of my hard-earned valuation lessons:

Tasty Bite - Bought at 900, sold at 1700. 4 months later today at 3000

Coming back to Satin, my view is merely a word of caution for people evaluating Satin at current levels. I haven’t done an in-depth analysis of last quarter’s numbers, but when I bought this in March around 300, my expected book value for FY16 was around 100 i.e. 3 times P/B and it was comfortably met. So based on TTM financials, it’s 6.5 times P/B at current levels - which is reasonably expensive IMHO. Now I know markets are always forward looking and keep on discounting 1-2 year earnings in the price but I don’t. And I’d rather base my future loan book growth estimates at 30-40% rather than 60-70% at which Satin has been growing at. As an investor, it’d be way better to get a positive surprise than a negative surprise from the future performance especially for very high-growth companies. I know this will lead to many mistakes of omission, but I’d much rather make those than mistakes of commission. Also, this is just my way of analyzing the business and my approach has evolved significantly over the past 2 years. Wrong or right - time will be the best judge

9 Likes

Thanks Gurjota. Just one comment on Satin, if you do the numbers assuming 250 cr equity raise at ~600 Rs per share in August, and 1000 cr pat for FY17 you will get more comfort on valuation based on P/BV My estiomates are at cmp ist 2.5x FY18 BVPS

Agree risk is growth slowdown and credit cost spike. But pointing valuation is not a concern right now imho if you are forward looking

2 Likes

Very right. Sold very good business early…like Ajantha pharma, Symphony,

Bajaj Finance, Indo count etc… They are up several times after the

sale… Do not want to repeat the mistake. Satin can be the next Bajaj

Finance if the management acts right…Discl 3% of PF in Satin

there is a report released by by axis stating microfinance can grow the housing finance way…if anyone has it please share.

I agree with Gurjota. The stock running up 10-20% on a regular basis is something thats a little difficult to digest. A couple of days back it ran up because MS Singapore Pte bought some 3 lakh shares of the floor of the exchange (no block, no bulk deal). I would also attribute today’s run up to something like this (wouldn’t be surprised to see if the buyer is MS SGP only). Now I think this MS SGP PTE is a PNote and could or could not be holding the stock for genuine investor.

We have often seen in the past that stocks run up quite a lot just before a QIP based fund raising takes place, as it increases the minimum floor price as per SEBI formula (average of min and max of last 7 days and min and max of the 7 days before that). We all know that the company is working with a top Investment Bank on the street. They have also gone on the road to market themselves (details of meetings were disclosed on BSE last month). They are targeting a fund raise in the first week of August, which makes the last two weeks of July critical, from a pricing perspective.

3 Likes

But what next for investors… I missed the bus at 400-500 levels and have been waiting for a entry point but this run up is outrageous & frankly I find this to be really overvalued at this point of time.