Will definitely take notes if I do manage to attend. Intend to do so.

1 Like

2 Likes

The power of compounding and growth shows up. But out human biases do not allow us to look even 1 year ahead. That’s the ooportunity

Satin AR Out. A good read.

- QIP due after 1 year of listing ie in August.

- Recent entry of Morgan stanley n DSP Blackrock shud lead to fancy n rerating

- BV cud rise to as high as 170-180 post QIP as dilution at high BV is good for NBFCs n Banks n PBV is high for SKS n other MFIs

- Awareness level still low for Satin

- Professional CA first gen promoters from service class back ground

- Huge opp size n good frowth in top n bottomline to make it standout

- Worlds top PE players specializing in MFIs invested in it since last few years n own nearly 50%

5 Likes

Great points Vivek. If I may add

on the promoter, they also have the highest promoter holding of all MFI’s - skin in the game. Highest by a huge margin.

Returns improving with scale

1 Like

On page no. 59 , on Risk and Concerns ,It was mentioned that

The mitigation plan of management for those mentioned risks is holding cash in balance sheet (~20% 0f Total Assets). IMO , that mitigation plan is not enough because NBFC/bank borrows up to 8 to 10 times of their net worth even small default will put them to greater risks which could not be solvable through that mount of cash . We, Investors in financial stocks should focus on banks that manage their risks better rather than the ones which remain focus on only growing their business through loan book and network expansion.

The risk are in details are

Financial an Funding Risk: The cost of Funds of Satin Care (14.5)is relatively much higher than the Peers. SKS is truly a market leader here because they are most Cost Efficient lender in the industry. Below are the Care rating assigned to company’s NCD. Better rating lesser cost of funds in money instruments

Operational and Political Risk: Loan portfolio is not well Diversified . UP alone holds 41 %, Bihar holds 18%,MP 16%, Punjab 13% (88% is concentrated in 4 states)of their MFI Portfolio as FY16 which is still Geographically concentrated. Any sort of black swan events in a particular state/region like drought, disease (63% of loan purpose in Agriculture and Animal Husbandry) could severely hit the operations. Unlike SKS, Ujjivan ,Equitas Satin’s Business is also not diversified , they primarily focused on GLP loanding. GLP is moat indeed but it is also single source of income for them.

Let me know your thoughts on these. Just to share, SKS AR is truly good to read . The risks and their mitigation plan is very well described ![]()

8 Likes

The rating cud improve after pending QIP.Presence of top notch PE players n FIIs gives lot of comforts.Only optimists survive

discl- Invested in it since Oct 2015 n no activity in last 30 days

2 Likes

For Satin funding cost is a huge opportunity. As scale increases, diversification increases, lenders get more comfort, ratings improve, costs of fundig improves, cost of lending lowers and growth improves. Virtuous cycle that will see ROA and ROE improve and support high growth. Unlike Equitas and Ujjivan who will see ROA decline and growth slowdown as they change business models.

“I skate to where the puck is going to be, not where it has been” -. Wayne Gretzky

In investing it helps to understand where the business wil be down the line, not where it is. Satin is in a virtous cycle. At 2x P/BV for FY18 for Satin current price is not factoring the improvement. This gives comfort on upside. Can’t say the same for equitas and ujjivan.

And on risk control, if some one is to form a view of under writing quality based o few lines in annual report then power to that investor and good luck

Disc: Invested

2 Likes

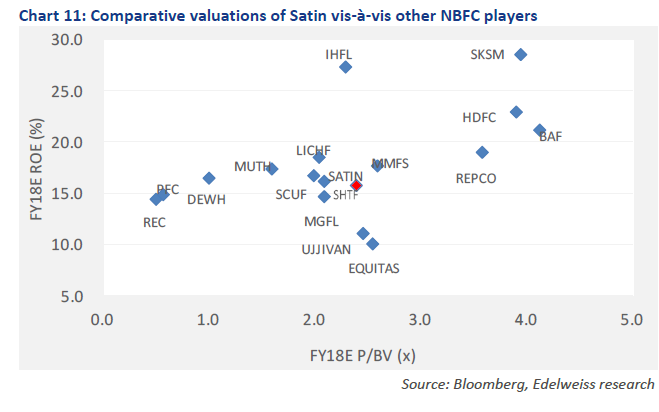

Edelweiss report on Satin, a good comparision on 4 MFIs Satin, SKS, Equitas, Ujjivan on various parametes!

4 Likes

Can you post the downloaded report?

Thanks Anjaneyulu.

Satin will really stand out on FY18 BV valuation terms. By my estimates ROE will be closer to 20% and growth >35%. One can compare with other NBFC’s and see the value for this growth, ROE and valuation. My view is 4x FY18 P/BV is fair vs other NBFC’s. Thats double current price! Key is execution over next year and QIP.

Diclosure: Invested

satin report already posted

Unlike Ujjivan and SKS, Satin appears to be lagging behind in terms of technology adoption. This is important because technology brings in a certain amount of transparency and gives some comforting factor with the numbers they claim. I understand both Ujjivan and SKS are using IBM provided cloud based solution. Ujjivan also has their field agents carrying hand held devices to capture data.

Agreed Madhu. They need to execute on this. They talk about it but

execution is the key. My guess is they were waiting to scale up before

taking this IT cost so that the base to take the cost is higher. Now they

should execute

Currently 5% of satin collection is cashless. They are working towards taking this proportion to 50% by the end of FY17. This front end digitization process will indeed help MFI loan officers and individual loan sales force. They can access and assess customer information, financial position and credit bureau details on real-time basis.

I was in a innovation conference yesterday and got a chance to hear someone from Paypal talk about future of payments in India. I asked him about microfinance and asked him how paypal was looking at this (opportunity) ? Sadly he dodged my question and he either did not had a answer or was unaware of what was happening in the MFI space.

I have read in Satin’s AR that they have tied up with ITZ Cash for cashless transaction. Can someone help me understand how this works in a little more detail?

I think that the graph made by the analysts gives a comparison of P/E ratios of these NBFCs. The slope of the line that fits the points in graph (regression line) is the average value of 1/PE of the NBFCs. This is because P/B = P/E * RoE, or RoE/(P/B) = 1/(P/E). It appears that the SFBs (Ujjivan and Equitas) are below the regression line and are valued at higher PE ratios, and SKS and IHFL are trading at lower PEs. Satin is somewhere in the middle. If one is positive at the Microfinance space, then the chart says that SKS should be looked at favorably too.

SKS has ~30% RoE and is trading at P/B of 4x. It is the largest MFI. Comparatively, it might be difficult for Satin to trade trade at P/B of 4x at RoE of only 20%.

2 Likes

Pratap what this graph misses, and we need a graph in 3d for that is

growth

Satin with its low base and penetration geog will have longer growth runway

of 30-60% than SKS also

Also one should adjust normalized tax rate for SKS as the tax beenify will

not last forever, not sustainable, to calculate comparable roe

Having said that SKS will always trade at a premium. Question is what’s the

right premium.