Arre boss, in a lending business borrowings are the raw material. The Company is in the business of borrowing at 12-13% and lending at 24-25% so it is a 10-12% gross margin business (to take a manufacturing analogy).

If it disburses more than it collects in any given year cash flow will be negative but that is not a negative thing unless you start seeing bad loans rise. If your concern is that borrowings are locked with bad customers then you should look at the provisions line (which is less than 0.1% here).

Focus on growth and focus on ROE. ROE summarises all the key metrics - lending rate, cost of funds, operating costs, provisions and leverage.

ROE is not actual metrics for these kind of business —Key metrics is ROCE which adjusts the debt also and further Provisions are at mgmt discretion they roll over always which i have seen during my audit of one NBFC-Bharatiya samrudhi finance ltd.

Always discount capital risk when evaluating these kind of business. Please comment.

Don’t disagree on importance of ROCE, in which case you should look at the ROA metric in this case which is the right equivalent to ROCE in a manufacturing or services business.

Provisions are actually not at the discretion of management anymore (they used to be pre 2012) since RBI requires these businesses to report all loans that are over 30 days past due (30 DPD).

BASIX is a bad example and the reason that company has massively declined is because of its past practices which all blew up during AP crisis in 2011/12.

@mani you are cluttering the thread. This is not a lending 101 thread and ask how lending business work and what to look for. Pls start a separate thread for that. Request moderators to note and delete irrelevant posts diluting the purpose of this thread, which is to separate the wheat from the chaff for satin credit…

RBI only asks to disclose…but provisioning is at the judgement of management based on past realisations with the customer . ROA is another matrix in service and less borrowed company , as most of expense is employee cost.

Yes friend, I have doubts on financials…not the business model, Its my profession to read on financials and understand risk in financial statements. I have audited NBFC companies and sharing over here . Further current discussion is gng on why Gross NPA & NET Npa is rising .

Shehzada is promising massive loan waiver to farmers in UP ahead of elections. Not sure it would work but does that pose any threat to Satin’s biz model?

sumi00, v4value, peguy and admin - at this moment I am more concerned about the relevancy of this thread than anything else. This is an eye opener for me that a person who claims to have audited NBFC is concerned about growing debt of a NBFC. If NBFC would not increase the debt then what else is the business? How the NBFC would earn profit other than it would take loan at lower interest and give it to the customers at higher interest. We all know and its discussed on this thread that optically NPAs very slightly up because NPA recognition date is reduced to 90 days from 120 days.

@sumi actually this is quite positive in the short term if it happens for lenders and farmers, bad for tax payers. This is how. Waivers means the government will repay farm laons to banks. There is extensive communication between RBI and governments on this , you need to just Google . PSU banks are very happvy because this means zero npa and 100% collection in a normally very dodgy portfolio. Farmers are happy off course. Satin like players should be happy - though they do not lend directly foro farming there is allied activity exposure(buying cows for example), as farmer balance sheet is cleaned and delevered chances of default reduce and ability/appetite for future debt from players like satin improves.

Basically the only ppl getting screwed here are tax payers. In the long term one could argue about the impact this has on credit culture for farmers.

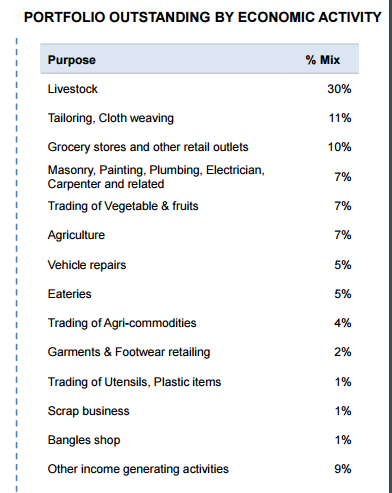

@sumi further on the farmer question, below is the portfolio of SKS (Bharat FIn, from their ppt) by end use. SKS is more rural based (75% of book) and end use shows no direct farm loans but indirect dependence:

My concern was regarding credit culture. If the govt. keeps waiving loans, there is always a risk of over borrowing like it has happened in the past. When UPA 2 waived farmer loans, farmers defaulted on many other loans as well and led to deterioration of credit culture. I have seen MFI biz very closely as one of my close relative was promoter of one the MFI and had to sell the portfolio (~100cr) and run after Andhra crisis. Collection went down to 75% despite borrowers having no reason to default apart from the contagion from Andhra. All big banks worth its name including foreign ones were our bankers (Citi, HSBC etc) and they looked like fools after the crisis. They were trying to plug their gaps in their priority sector obligations. That is one reason I stayed away from MFI boom this time. I may be wrong and biased here.

There is no doubt that waive off of the loans sets wrong precedence. However there is difference between private lending and government lending. This difference in my humble opinion is very fundamental in nature and the loan taker understands it. Just to drive the point, select set of people ( I would not dare to generalize)are comfortable defaulting on electricity bills or paying less income taxes, but the same set of people are much more careful about not defaulting on private loans. Somehow not paying or delaying dues to government is not seen that bad in our society as not paying to private lender. Maybe because the private lender would knock on your doors sooner than government does. Maybe sometimes government does not knock on your doors ever. May sometimes leaders opportunistically get the government loans waived off.

The root reason behind Andhra originated MFI crisis were different (discussed on multiple threads on this forum) and personally I do not see this move from a political party meaningfully impacting the industry dynamics.

@Krishna to add to your point - credit burequs for retail and MFI NOW present are a structural change that enforces credit behaviour for private lenders.

Satin has disclosed their Sep qtr share holding today. While a bunch of Foreign Institutional investors have come in, presumably in QIP, what is interesting is domestic mutual funds have taken a 6% stake. I will be curious to see who they are…