5G

1 Like

Just to add that the person name " Bipin Amritlal Turakhia" who own 2.56% shares in the Company and was in the Public Category got added to the “Promoters Category” hence that the change. Do we have any info who is this person is ?

From a safe dividend heaven for investors, Sasken has become a mediocre play.

-

Sasken Technologies Embarks On ‘5x5 Vision’; Stock Surges To 10-Year High

what happened to this vision by Sasken? Agree that the pandemic slowed growth but Sasken is not even near the halfway mark. Rather, their topline has been stangant - Topline growth is in negative or zero territory since last ten years. Bottomline growth is mostly Sasken milking its top 10 customers which form bulk of their business (70%). Is the bottomline sustainable considering the Topline is under extreme stress?

- Total active clients over $1m have reduced from a high of 22 in Q3 2020 to 16. Not a single 10m client. This despite the huge overhaul and new hirings in the top management.

Buzzwords like connected car tech, 5g and ev are not bringing in the desired revenue.

Investors prefer that Mr. Mody walks the talk.

1 Like

I am happy with the margin expansion and higher profits. My concerns are with flat revenues and loss of clients.

The article IS from 2017, indeed. But, it is talking about Sasken’s 5 year plan or the future. Here is another link on the same.

“Sasken has embarked on a new journey, as outlined in our 5x5 vision, to build a robust organization as well as achieve profitable growth and revenues of $250 million by 2021."

Considering the Pandemic and it’s aftereffects, Sasken has not been able to move it’s sales needle in more than a decade now. Let alone closing in on the target. Mr Mody never mentioned the 5x5 vision again post 2018. Does this not mean the company has failed to capitalise on its future plans?

The increase in profits and margins is a sign of a strong business, yes but future growth needs to be considered too via a vis the competition. We need to compare how Sasken has performed against the competition.

Holding and hopeful but not positive on Sasken until topline grows.

3 Likes

Is anyone tracking recently, I am curious about it.

Any views will be highly appreciated

1 Like

Not actively tracking as there is nothing to track. The only time Sasken has been in the news has been for results.

Otherwise, my last post still holds true. No topline or bottomline changes since about a decade now.

It would be good to see an acquisition or a merger in the coming times. Most newer businesses vhave overtaken Sasken now.

1 Like

The company is into very niche sectors like

BLOCKCHAIN

5G

AI & ML

V2X

IOT

Some time back there was some news on takeover by JIO.

Hopefully in time to come some big giant will takeover Sasken.

Source: screener.in

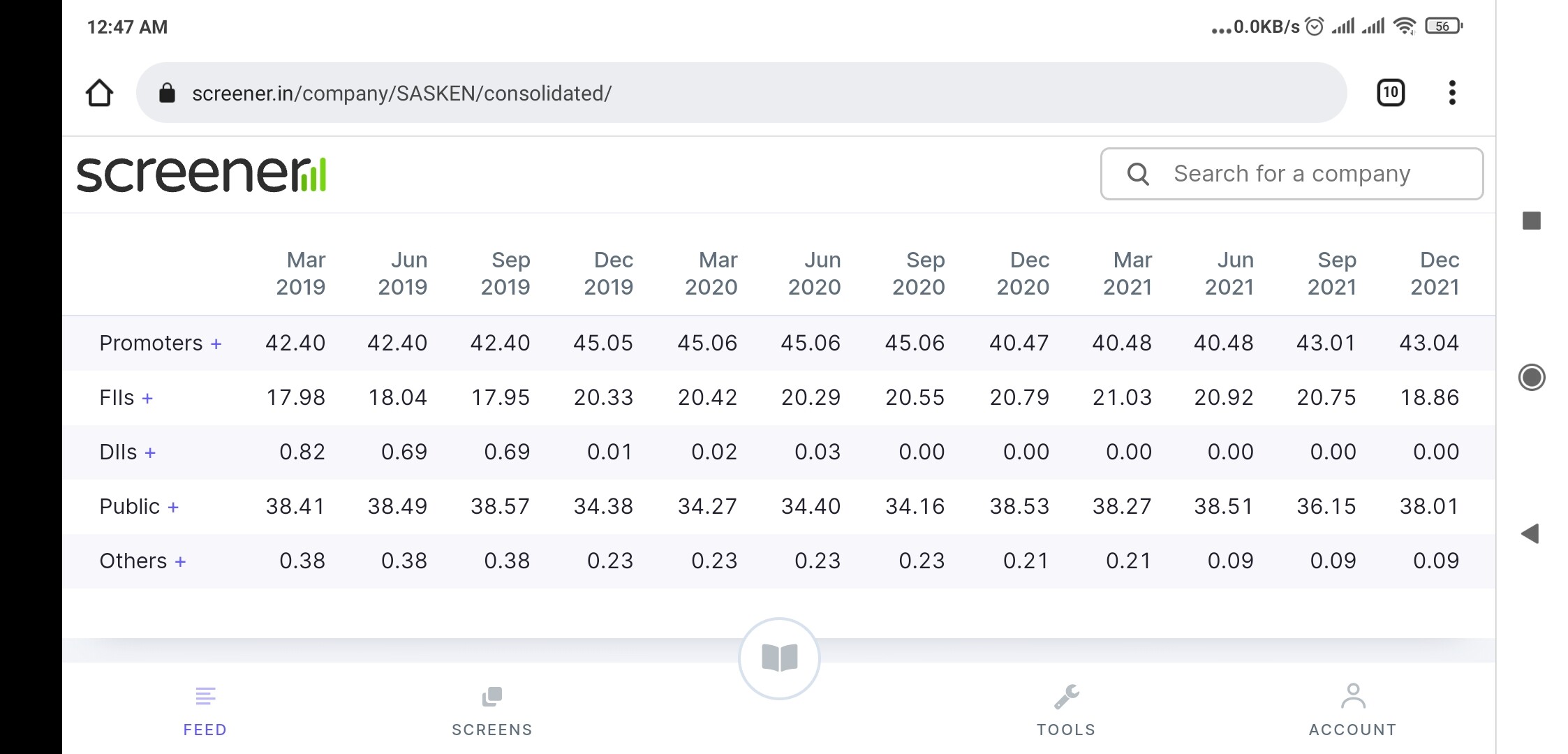

Interesting share holding pattern for Sasken.

Promoters increased stake from 42.4% to 45% in Dec 2019 qtr.

Then reduced to 40.5% in Dec 2020 qtr.

And increased again to 43% in Sep 2021 qtr.

Instead of concentrating on business sales and revenue increases they have been playing with share holdings.

Disc:

Invested since 2011 at 85 in small qty.

1 Like

If you notice the shareholding pattern changes, the promoters have only proceeded to reclassify family members as retail shareholders.

The actual promoter holding remains the same.

As far as rewarding shareholders, I would rather have a buyback than dividend with flat revenues and profits. They can issue bonus shares in the future if and when revenues breakout of the 10 years stagnation.

2 Likes

Article mentions Sasken Technologies’ foray into Cyber Security, primarily into Android. It stresses on the company’s efforts post the pandemic. Whether this is backed by data or generic statement cannot be confirmed.

3 Likes

Sasken has announced flat results again.

A few positives.

- Mr. Mody has accepted that results have been flat. Acceptance means corrective action.

- Customer for Sasken seem to be sticky. Repeat business and margins point toward customer loyalty.

Threat.

-

Mr. Mody also accepted that competition is heating up. Remains to be seen how they navigate in the next few quarters.

-

Attrition rate at 36% is concerning.

Very poor execution by company. Another company in same business has completely different story to tell

2 Likes

Even With the pedigree, technology and Patents, A newer entrant like Elxsi has outdone Sasken. Clearly, a laggard. The company needs a change of guard, mindset, operations and goals.

But since Mr. Mody has an iron Hold, we will not be seeing any major changes to the organizational operations. Investors hardly get to see news on acquisitions, orders, concalls or press releases.

The only way I see it surviving long term is by getting acquired.

1 Like

It is not just Tata Elxsi even LTTS has shown very good growth.

With 36% attrition their survival will be challenged. More tech driven company is more you depend on your people. No biz growth means no career growth. Promoter should have brought in professional management. Too late. War for talent is real and is going to hurt smaller player with poor growth badly.

Yes, getting acquired is only viable option before it is too late.

There is a change in leadership team . . .

Ltr_to_SE_on_outcome_of_BM_10Aug2022.pdf (hubspotusercontent-na1.net)

It seems, the change is seen constructive in terms of stock’s price action.

1 Like