Saregama Carvaan takes a technology and content leap with Carvaan 2.0 by giving access to hundreds of daily updated Wi-Fi based audio stations along with 5000 evergreen pre-loaded songs… https://indiantelevision.com/television/tv-channels/music-and-youth/saregama-reinvents-carvaan-with-hundreds-of-podcasts-190618

1 Like

I am posting the stock idea presentation I did in VP meet in Goa this year. It was on Saregama. Will be happy to answer any queries on the same.VP_Meet_2019_Presentation_Saregama.pdf (902.7 KB)

11 Likes

Dhwanil,

One question which i have been struggling is, The customers to whom Saregama is Licencing and streaming are very large and powerful organizations like Amazon & Google. While the growth in terms of viewership may continue to happen, however do you see a risk, that Amazon and Google may decide to bring down the total payout using their size advantage. Saregama may become a price taker in few years time.

Even I do not have an answer to your question but I feel that situation that you are describing is surely a risk that is real few years out as the streaming platform players get into consolidation mode. On the other hand, catalogue (content) part is also consolidated and there are only 4 large players contributing to 90%+ of the catalogue collection. Hence they are not pushover either. It will be interesting to see how the whole dynamics play out

1 Like

Sure. another stuff that i found troubling was the pseudo options allotted to the CEO. As the profitability goes up it will impact the bottomline significantly. However you brought out a interesting perspective “Skin in the game”. Their is a keyman risk with too much riding on the CEO but he may be here for long if i try to think from the skin in the game perspective.

Nice presentation Dhwanil.

Had some questions -

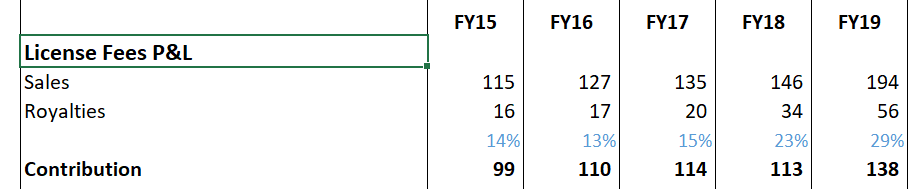

- Why has royalty as a % of license fees gone up substantially & how is this expected to trend? Are there any industry benchmarks we can compare this to?

- Why is gap between NPS (100 crs+ since FY15) and Saregama’ s EBITDA so wide? Is this not a case of a bloated cost structure or capital mis-allocation?

I have 3 queries that could be significant positives for Saregama excluding core operations:

1.have you got any update regarding monetization of real estate assets of 200cr as per last AR

q3 concall they give replied work is going on

2.What about 149cr of share of group companies they are holding in book

3. there was some mention about transfer of non core Open magazine(loss making) operation to other group companies

Disclosure( Holding 5% in portfolio)

1 Like

Hi, was anyone able to attend the AGM? Wanted some perspective on the future investments planned by the company

I think this company has been transformed in an excellent way by the new management. I feel they are taking all the right steps.

- Launch of Carvaan and variants around it

- Changing the culture of the organisation by hiring lots of people from outside

- Start acquiring new music and starting it slowly so that they don’t blow up big time

- Produce concept-based digital films for OTT apps

- Vikram being pro-active in sitting with the board of PPL & IPRS

The story is very good so far. For me, the key monitor-ables would be

- Quality of music content they are acquiring

- Quality of movies being produced

- A&P expenses as part of sales.

- Finally sales of Carvaan. Sales of Carvaan I believe will eventually go down in the next decade assuming they don’t come up with some extra-ordinary idea. May be they can postpone the decline by a few years, but it will eventually happen in the next decade.

- New innovation which provides continuous stream of revenue that can replace Carvaan eventually

Management mentioned that they are coming up with something very interesting for FY20 in Conf Call of Q3FY19. He said he’ll announce that at the end of the conf call, however, he couldn’t get the opportunity to announce his closing statements.

If anyone is already aware of any hints towards that, request you to share. My speculative guess would be along the lines of launching Carvaan globally in other countries with their local retro music for elderly people.

Though I’m fairly convinced about the new management’s capabilities and excellent business prospects for the future, I’m unable to understand how Saregama accounts its operations.

- New Music Rights: 66% of the cost is charged off in the first year. According to Q4FY19 presentation, they have spent 32.4 crores in acquiring new movie rights in FY19. This leads to 22 crores of line item in expenses. However, I don’t find any such expense in the P&L statement.

- Following up on the next previous point, how is remaining 33% treated? We should see a cash outflow of ~11 crores as even though it is not charged as part of P&L statement, the company should still see its cash going away from its bank accounts as it acquires movie rights. Again I don’t understand how this is accounted as part of cashflow statement.

- The management has said that they run on Cash & Carry distribution model for Carvaan. I believe such models have very low receivable days as they require upfront payment before distributing their products. However receivable days for the company is two months which is poor. It is possible that Carvaan’s receivables are good and the receivables are actually dragged by the other businesses but that would mean 110 crores of receivables on 300 crores of revenues (excluding Carvaan). Again that looks bad to me.

- Financial investments: I don’t understand why the company’s funds are locked in CESC shares and the freehold land. Someone tried asking the management during the conf call and the management just said it will be locked that way and can turn out to be gold mine in the future. Not convinced.

- Re-evaluation of land: The company went through the re-evaluation of its land in FY19 and increased its value in PP&E by 12 crores. Correspondingly it has been updated in the balance sheet, sounds good. But why did the company lose the cash for the same in cashflow statement? It has not spent new cash of 12 crores to acquire the same land no? Why did they re-evaluate it if they anyways don’t plan to sell it in near future? Is it to help themselves to siphon off these 12 crores? If the company really did buy new land and this additional 12 crores is not due to re-evaluation, then the question is why does the company need the new land for its daily operations?

- Legal / Consultancy Expenses: Legal / consultancy expenses of 15 crores? This was around 4% of revenues till FY18! And still 2.2% of revenues in FY19! Understand entertainment industry has lots of legal issues however if you want to benchmark against Shemaroo Entertainment which is also in a similar field and revenues in similar order, its legal expenses are around 5 crores, which is 1/3rd compared to Saregama.

- Advertising and Sales Promotion: This was already questioned by Dhwanil in one of conf calls and management mentioned that they are aggressive to get Saregama the right base and it should not be so much in the future. I’m still not happy with management’s answer but we can move on to the next one

- Travelling & Conveyance Expenses: Again, this is about 1% of sales! It used to be 2% just two years back. I’m unable to comprehend why 6 crores would be needed for travelling and conveyance for such a small company. To give you a perspective, in FY17, PAT of the firm was 8.64 crores and travelling expenses were 5 crores.

- Printing & Communication: Same story

. In FY17, PAT was 8.64 crores and printing expenses were 4.38 crores. However, good thing here is, this is decreasing in % of sales as well as absolute numbers.

. In FY17, PAT was 8.64 crores and printing expenses were 4.38 crores. However, good thing here is, this is decreasing in % of sales as well as absolute numbers. - Royalties: This is about 9% of sales. Why is it so high? Which stream of business do we pay royalty for? What is the industry standard, like how much royalty do we pay to the singers even after acquiring the music rights?

Overall, one can notice that the company is very extravagant in its spending in ‘Other Expenses’. I’m afraid this can be a good way to siphon funds off the company. Given the turnaround the management has done, I think we can consider giving the management the benefit of doubt too. Above issues identified could be due to my inability to understand accounting. However, I believe a shareholder of the business should find out answers to the above questions. Requesting fellow VP’ers to help with the same.

Discl: No holdings. Don’t see myself buying unless I have answers to above concerns.

Additional Discl: I hold Shemaroo Entertainment. So my views may be biased.

16 Likes

Are results that bad if YoY the exception income of last year were to be removed? LC is overreaction or just Mr Market is sensing something else? Fellow boarders your thoughts?

Hello Dhwanil,

Wanted to know your thoughts on Saregama’s latest result and the market reaction. Heard the concall, I feel was the major change is the plan to spend more on Carvaan marketing, the management not committing any change in capital allocation isn’t something that happened “right now”  .

.

So what has changed is the expected cashflow from Carvaan not coming. Or is the market worried that the “marketing expense” on Carvaan may be another way to subvert capital.

Thanks

This is interesting read on how buffett thinks about media businesses -

https://wordpress.com/read/feeds/59790521/posts/2378812759

Market spooked by low single digit pat margin on car aan. Continue higher marketing cost. Now STORY of carvaan looks less promising to market. I am still holding on base of movie making model, in which one or two hits can change everything. Carvaan as vikram said not making losees. If management care about minority share holder, they should sold open magazine and land.

Disclosue: invested.

The most worrying aspect is substantial watering down of outlook for this year and the next. The tone of Vikram Mehra was quite defensive and acceptance of the cluelessness of Caravan’s financial impact.

@sarthakkumar19_

As we can see the current result was impacted by extra spend on below the line marketing that they did for Caravaan. Even though management had indicated in last call too that they need to spend money on creating awareness in tier-3, tier-4 towns to keep the momentum going, market did not pay attention until the amount was spent and was reflected in P&L. From business perspective, I don’t think there is anything wrong in spending money if they see large potential in product and long runway for growth. Having said that there remains a risk where even after spending money on advertising, the growth is not commensurate or the profitability is not adequate to warrant decent payback for Caravaan. However, it is a business call and only management who is privy to lot many variables can take the call judiciously. My sense is Vikram is quite realistic in what can be achieved and hence he will be prudent in spending money and/or doing course correction if he realizes that the money spent on A&P is not generating the requisite traction.

For me the most ineresting part of Saregama story is the streaming revenue and tailwind that segment has in current environment. I do not think there is any change in that thesis. What has changed is that if some one had assumed that Caravaan cash flow will be available for music content acquisition, they may have to realign those assumptions for the time being as Caravaan will remain in investment mode for some time.

Discl: Invested with small allocation. I am a SEBI Registered investment advisor with registration no INA000012388 and views expressed here shall not be construed as investment advise or recommendation to buy/sell. Please do your own due diligence and/or consult your investment advisor before making an investment decision.

5 Likes

Long trapped in a vicious circle of piracy and big Bollywood studios, the music business is breaking free of its shackles under sustained push from the growing band of audio over-the-top (OTT) brands. Keen to muscle their way into the multi-lingual listening routines of audiences with varying tastes, Amazon Music, Spotify, YouTube and local players Gaana, Jio Music and Hungama are using data and technological innovations to package their music for audiences across age and income groups. But as they do that, the big challenge will be differentiating the listening experience even as they spin their music from a common spool.

“In India, we’ve customised our pricing for two reasons. First, the consumer is value conscious, and second, India is yet to transition from a largely piracy-based market to one that streams music legally,” says Amarjit Batra, managing director India, Spotify.

The Indian music market holds out huge potential. A recent report by Deloitte (Economic impact of music) estimates the valuation of the audio OTT industry in India at Rs 2,700 crore and its annual revenues at Rs 270 crore. Experts say that audio OTT brands expect the market to grow from 150 million users now to 400 million users over the next two years. While there is ample room for growth, the brands are also conscious of the need to keep an unrelenting eye on affordability.

The market has shifted significantly from earlier years as says Siddharth Roy, CEO, Hungama that was one of the early investors in the business, “The Indian consumer today is comfortable with streaming music. Increasingly, this consumer is opening up to the idea of paying as well.”

However, the other challenge is classifying the Indian customer. Music is accessed in many languages. Also listeners are fickle, switching between brands while seeking a cheap entry into the ecosystem. The apps therefore have to offer a wide variety of packages; on Spotify there is a free (ad driven) or a subscription (ad free) model that is further sliced into daily, weekly, monthly, and annual plans, starting from as low as Rs 13, Batra said.

At Gaana, where CEO Prashan Agarwal says, subscriptions have boomed under increased adoption of digital payments, there is significant experimentation with innovative monetisation models. “I feel the Indian consumer is not price-conscious, but value-conscious. If we’re able to deliver significant value for their money, they will be more than happy to sign up,” he says.

All OTT brands are using data to profile their listeners. Agarwal says, “Data goes a long way in evaluating our business decisions. For example, we know that more than 80 per cent of our listeners listen to music in two languages. We curate language packs and target those segments,” he adds.

That Hindi is not the only language spinning the music tracks for Indian listeners is well known. However the data sets gathered by the audio companies helps them classify audiences more finely. For instance, Bhojpuri audiences tend to be single-language users while the rest are largely two-language listeners. The South Indian languages make an easy combination for most too.

Regional music also helps build up content at a fraction of the cost of building the Hindi music library. Many are also looking at launching new artists in different languages. Agarwal says that this is a good way to offset costs of acquiring Hindi film music, which still has the largest share in the consumption pie.

Apart from advertising, the platforms are also looking at monetising their libraries and product assets through brand partnerships and sponsorships. Hungama for example has branded playlists where a product or service is integrated into the playlist. Others use podcasts for the same.

“We do see immense potential in the podcast domain. According to a global research in 2018, half of the podcast listeners said that podcast ads are more relevant, seamless, or entertaining. In India, maybe it’s a bit early, but yes, we’ve had brands and advertisers show interest,” Batra says.

2 Likes

In addtion to above link where they plan to foray in web series, they have launched saregama carvaan brand to make carvaan lounge similar to coke studio and mix tapes from T- series. At first look, this looks very good move, where company can have increased brand value, retain new IP and free advertisements.

https://www.youtube.com/watch?v=dQQH5fMo4c4

Disclosure:

Invested.

Old but detailed view on it

1 Like