Saregama India Ltd. is an Indian music label and content producer for Indian television.

Its music catalogue consists of more than 117,000 songs in 14 languages built over a period of more than 100 years. It has daily and weekly TV shows currently on air with television networks[in India.

Saregama’s head office is located in Mumbai, with other offices in Kolkata, Delhi and Chennai.

It is listed on the NSE and BSE.

The company was founded in 1901. It produced the first song recorded in India and later moved into the production of cinema and television content, digital retailing, aggregation, radio programming and events.

History:

EMI

In 1901, operations started as the first overseas branch of Electrical & Musical Industries Limited, EMI London.

The company was incorporated on 13 August 1946 with the name of ‘The Gramophone Co. (India) Limited’. The name of the Company was subsequently changed to ‘The Gramophone Co. of India Limited’ effective 1 April 1956. It was converted into a public company on 28 October 1968 and consequently the name of the company was changed to ‘The Gramophone Company of India Limited’.

RPG Group took over the company in 1985 from EMI.

The name of the company was then changed from “The Gramophone Company of India Limited” to ‘Saregama India Limited’ on November 3, 2000

In 2005, the remaining EMI stake was sold off to the parent company.

HMV

The Gramophone Company is better known as HMV (His Master’s Voice) in India. RPG Group has been using the brand under license from the former parent company, EMI.

On 3 November 2000, RPG Group changed the company’s name to Saregama India Limited, and introduced a music label of the same name.

Dum Dum Recording Studio

The Recording Studio and the entire Dum Dum establishment of Saregama India Limited was built in 1928. It is one of the oldest studios in Southeast Asia. Nobel Laureate Rabindranath Tagore had recorded his songs and poems in his own voice at this studio. Rebel poet Kazi Nazrul Islam’s voice was also recorded here.

Artistes who have recorded at this studio include K.C.Dey, Hemanta Mukherjee, Sandhya Mukherjee, Manna Dey, Suchitra Mitra, Ustad Bade Ghulam Ali Khan, Pandit Ravi Shankar, and Ustad Bismillah Khan. Film director Satyajit Ray preferred to record his musical scores for his films at Dum Dum studio.

Television shows such as Dadagiri, Didi No. 1, Dance Bangla Dance and Saregamapa Lil Champs have been shot at the studio.

Operations:

Music audio

Saregama provides music repertoire across several genres and languages, including music of the first film made in Bollywood ‘Alaam Ara’ (1931) and artistes such as K. L. Saigal, Lata Mangeshkar, Madan Mohan, Shamshad Begum, Asha Bhosle, Mohd. Rafi, and Kishore Kumar.

In April 2014, Saregama entered into a partnership with an international digital distribution company, Believe Digital, for digital distribution of the entire music catalogue to the international market, especially to the Indian diaspora.

In March 2015, Saregama relaunched its online music store, consisting of more than 117,000 downloadable songs in 15 languages in lossless WAV format. It has four main sections – Hindi, Devotional, Regional & Languages in 35 sub categories with an added feature called ‘Experience 360’ which provides the users with information regarding the song, artists, artist biography and videos along with related songs.

Saregama has also established relationships with iTunes, OTT services (Gaana, Hungama, Wynk Music, Eros, Saavn, Biscoot & Guvera) TV channels[which?] and radio stations[which?]. Additional focus areas include direct-to-customer retail business via its website and applications, physical distribution, YouTube, and sales from reinterpretation projects, new Indian language television software.

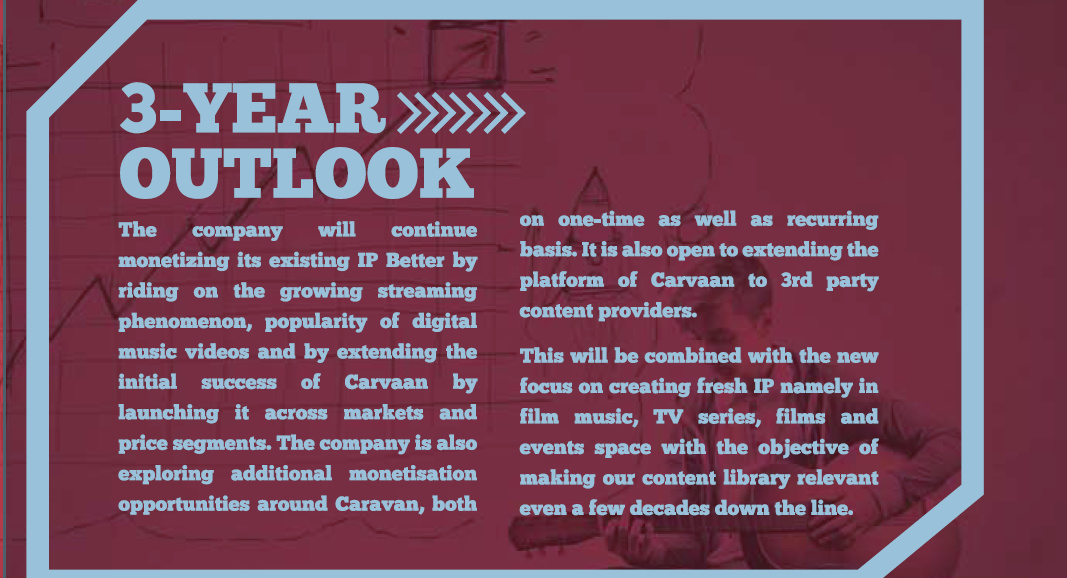

Saregama Carvaan

Continuing with its mission of offering music in both digital and physical formats, Saregama is launched a global first, a portable digital audio player with in-built stereo speakers and 5000 evergreen Hindi songs inside. Branded as Carvaan, this audio player combines the best of digital technology with the convenience and ease of use of a physical form factor. These 5000 songs available on Carvaan have been handpicked using big data and categorised based on singers, lyricists, music composers, moods etc. Each category can be selected by turning a jog-dial. With a simple turn of a knob, one can switch from Kishore Kumar classics, to R.D Burman’s pulsating hits, to timeless love songs or to soulful Sufi tracks – all in their original versions, back-to-back without any ads. Carvaan’s music collection also includes the entire Ameen Sayani’s Geetmala countdown collection spanning 50 years. With the option to tune into FM Radio, Carvaan doubles up as a home radio too. It’s possible to enjoy one’s personal collection of songs by plugging in a USB drive or streaming songs from a phone to Carvaan via Bluetooth. It works on a rechargeable battery that lasts up to 5 hours. The product is backed by an all India service network, providing 1-year doorstep warranty support.

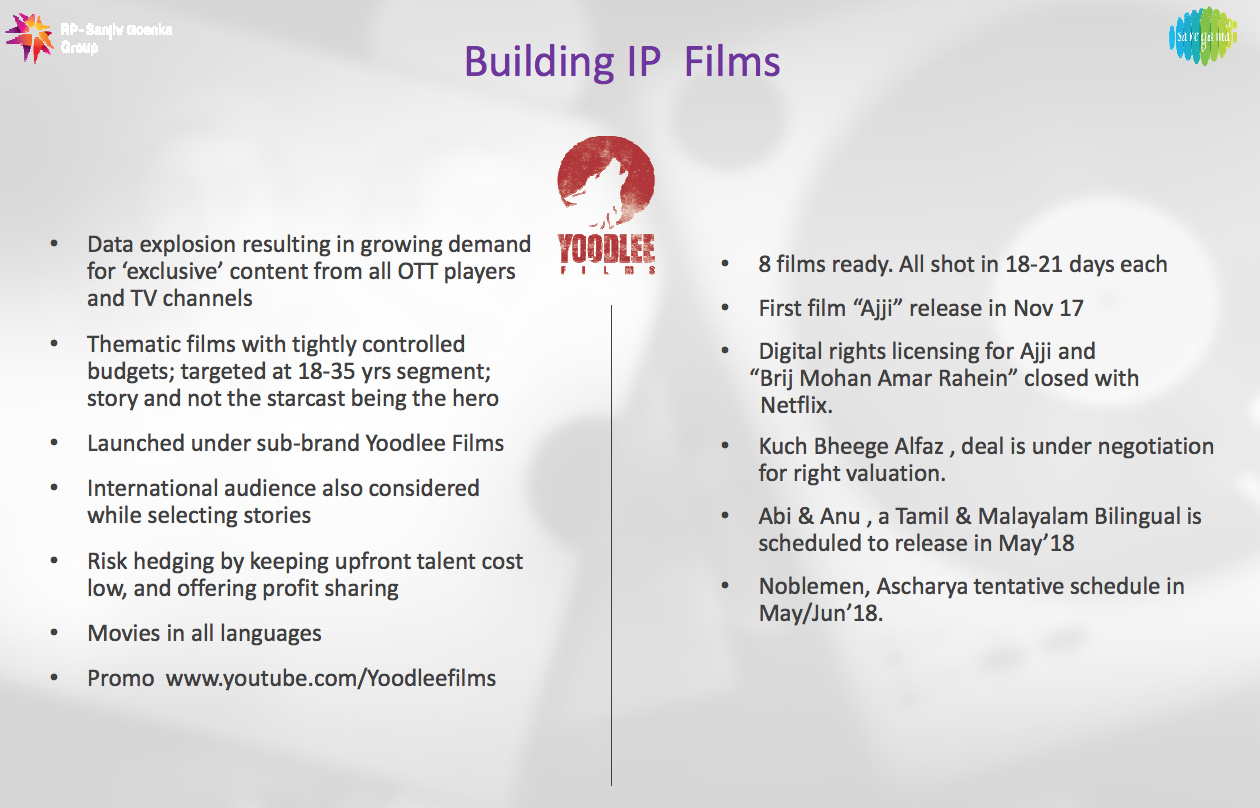

Yoodlee Films

While Indian cinema is gradually finding acceptance from a global audience, funding and support for Independent cinema in India is hard to find. Commercial Indian cinema, colloquially known as ‘Bollywood’, does not serve a large swathe of the domestic audience and has limited resonance with the global viewer. Through Yoodlee, Saregama wishes to fill this gap with stories that are driven by strong themes and entail a “no compromise” approach of fearless filmmaking. Driven by powerful stories and not by stars, the passion of the filmmaker is the starting point for everything in a Yoodlee film. Yoodlee desires to bring a heightened sense of realism to films which are: shot in real locations, with sync sound, on the best camera technology available. Yoodlee wants to take on themes and deal with stories that others may balk at, allowing a whole generation of Indian filmmakers to find their own authentic voice.

Saregama Classical Mobile Application

Saregama India launched a subscription based mobile application in September 2015 which features its catalogue of Indian classical music. The app, named ‘Saregama Classical’ has more than 10,000 musical works of over 400 classical music artistes in three major subgenres of Indian Classical music, i.e. Hindustani, Carnatic and Fusion. It also has a curated list of 50 artiste-based stations.

The app consists of works from artistes such as Pt. Jasraj, Ustad Zakir Hussain, Pt. Ravi Shankar, Begum Parveen Sultana, M S Subbulakshmi, Karaikudi Mani, N. Ramani, and Pt. Bhimsen Joshi. It supports offline listening where the app allows users to download its songs on the phone, so that the user can listen to it later without any data charges.

Saregama Classical is available worldwide on Apple and Android stores. It is a free to download app with a seven-day trial period. Customers then have an option to choose from monthly, semi-annual or annual subscription. The payment can be made either through the iTunes for Apple users or the Google Play store for Android users. Customers can also pay via their telecom operator or through their credit card/net banking/debit card.

Saregama Shakti Mobile Application

Saregama India launched another subscription based mobile application in January 2016. The app is called ‘Saregama Shakti’ and it offers a large collection of devotional music, videos on demand and high quality wallpapers. The bhajans on the app are sung by renowned artistes like Lata Mangeshkar, Anup Jalota, Suresh Wadkar, Jagjit Singh, Asha Bhosle, Anuradha Paudwal and Sadhna Sargam, amongst many others. The app also offers audio recitals of granths like Tulsi Ramayana, Geeta Govinda, Sundar Kand, Satyanarayan Katha, Sai Satcharitra Granth and Krishna Charit Manas etc. Along with the content of various Hindu dietie, the app features the entire content catalogue of Art of Living and offers the largest collection of audio, videos of various techniques of Art of Living like Sahaj Samadhi Meditation, Bhajan & Chanting, Yoga, etc. Along with the teachings of Sri Sri Ravi Shankar, Saregama Shakti recently added the largest collection of content from the Chinmaya Mission.

The app supports offline listening where the app allows users to download its songs on the phone, so that the user can listen to it later without any data charges.

Saregama Shakti is available worldwide on Apple and Android stores. It is a free to download app with a 1-day trial period. Customers then have an option to choose from monthly, semi-annual or annual subscription. The payment can be made either through the iTunes for Apple users or the Google Play store for Android users. Customers can also pay via their telecom operator or through their credit card/net banking/debit card.

Saregama Music Cards

Saregama launched its retail product named ‘Music Cards’ in March 2016. It is a credit-card-shaped 4 GB USB memory stick which is pre-loaded with 150 HD-quality songs of various genres. The genres which were launched in phase one include ‘Legends’ (The best songs of Hindi Cinema from artistes such as Kishore Kumar, Lata Mangeshkar, Mohd. Rafi, etc.), ‘Romance’ (The best romantic songs of the Golden age of Hindi Cinema), ‘Jagjit Singh’ (150 of the best songs, film and non-film, of the Ghazal maestro), ‘Shakti’ (The best devotional songs and bhajans) and M.S. Subbulakshmi (A collection of the best tracks of the iconic Carnatic vocalist).

Music publishing business

Saregama’s works with television channels, advertisers, film producers, radio stations, film and television production houses for use of its content. Collaborations include the song Fifi from Bombay Velvet, Hungama Ho Gaya from Queen and the Mahindra Rise Kisi Se Kam Nahi TV advertisement.

Television software

Saregama produces content for TV channels in Hindi, Tamil, Telugu, Kannada, Malayalam and Bengali.

Hindi

Saregama’s debuted on National TV at prime time with “Prayaschit”, a Crime-based show for Sony. This was followed by “Police Files” season 1&2 and “Pyar Ya Dehshat”, both 100-plus episodes each on BIG channels. Currently Saregama has two shows running on Doordarshan at prime time, “Stree Shakti” and “Jab Jab Bahar Aayi”. Along with TV shows, Saregama also produces vignettes based on the speeches of leaders including Mahatma Gandhi and Jawaharlal Nehru for EPIC TV. Saregama has been a regular producer of Savdhaan India on Life OK, producing over 175 episodes and eight Maha movies. Currently it is producing for the Maharashtra Fights Back series. Other shows includes:

• Savdhan India, Maharashtra Fights Back

• Daffa 420

• Jab Jab Bahar Aayee

• Prayaschit

• Police Files Season 1 & 2

• Pyar Ya Dehshat

• Stree Shakti

• Vignettes

South

The South TV Division of Saregama was started in June 2001 and has since then produced approximately 4,000 hours of TV content which has been telecast on Sun Network. Saregama has produced serials in genres including socio mythology, family soaps, fantasy fiction, and horror, in four South Indian languages.

The serial Athi Pookkal has broadcast over 1000 episodes in the noon band of Sun TV. Saregama has also produced several non-fiction shows where film celebrities such as A.R.Rahman, Vasunthara Das, Shivmani, Lawrence, Mumtaz, Malavika have participated as judges. Saregama currently has eight hours of programming per week on Sun TV out of which two are daily soaps (‘Chandralekha’ and ‘Valli’), one is a horror fiction (‘Bhairavi’), and one is a family game show ‘Chellame Chellam’.

Tamil shows include:

• Muhangal

• My Dear Bhootham

• Pondatti Thevai

• Kuttees Choice

• Athi Pookkal

• Valli

• Pillai Nila

• Chandralekha

• Soolam

• Velan

• Raja Rajeshwari

• Veppalaikari

• Bhairavi

• Mirinda Ooh La La La

• Close Up Super Dancer

• Masthana Masthana

• Rani Maharani

• Chellame Chellam

• Johnsons Baby Kuzhandai Paramarippu

• Jollywood Express

• Pepsodent Kids Khiladees

Telugu shows:

• Iddaru Ammayilu

• Jeevitha Chakram

• Namo Venkatesa

• Super Boy

• Kasi Majililu

• Close Up Super Dancer

• Rexona Evergreen Athithilu

• Jollywood Express

• 7 Up Ooh La La La

• Johnsons Baby Sisu Samrakshana

Kannada shows:

• Rathnagiri Rahasya

• Golmaal Gowramma

• Henne Nee Jaane

Malayalam shows:

• Aayilyam Kaavu

• Rani Maharani

• Jollywood Junction

• Mummy and Me

• Johnsons Baby Sisu Samrakshanam

Management

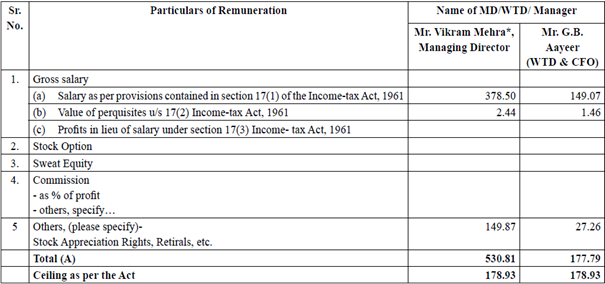

Mr. Vikram Mehra has been the Managing Director of Saregama India Limited at RP-SANJIV GOENKA GROUP PRIVATE LIMITED since October 27, 2014. Before joining Saregama, Mr. Mehra served as Chief Marketing Officer and Chief Commercial Officer at Tata Sky Limited until October 2014. In his decade-long stint at Tata Sky, he was responsible for subscription revenue management, brand marketing, new product development, customer analytics, interactive service operations, consumer research and PR. Mr. Mehra has a wealth of experience in handling the ever developing digital platforms. His deep understanding of various aspects and facets of digital media spearheads the growth momentum at Saregama of transforming and expanding the music label into a digital business. He started his career with Tata Consultancy Services as Senior Systems Analyst. After spending two years there, he moved to Tata Administrative Services as a Manager. He has also worked with Tata Motors during his seven year stint with Tata Group. Prior to joining Tata Sky, he was with News Corp owned STAR TV from 2000 to 2004 as Vice President, where he led its foray into DTH and cable services in India. He has been a Director at Saregama India Limited since October 27, 2014. Mr. Mehra holds MBA from IIM Lucknow and a B.Tech in Computer Science from IIT Roorkie

Scuttlebutt

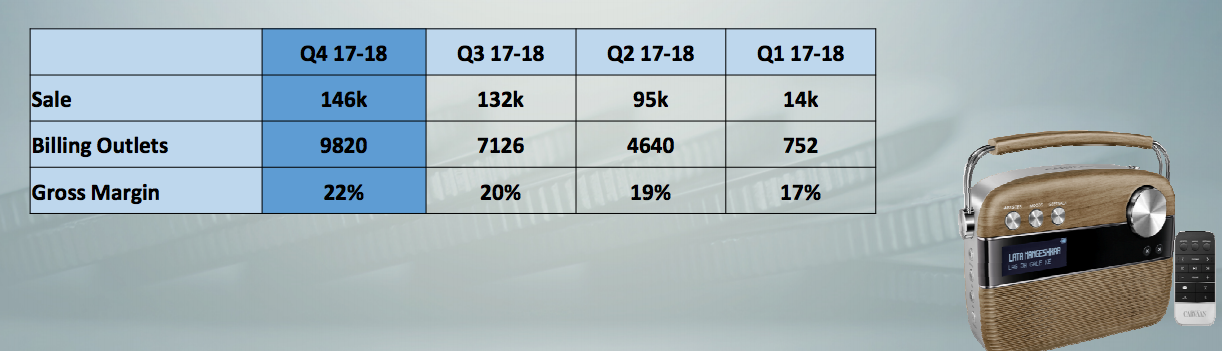

Have gone to meet some of the dealers in Punjab to have an insight on the success of the product: CARVAAN (Launched on 4th May 2017)

Got to know, that the dealers pay advance to the company to get the product and they have got bookings done in advance till Diwali which is a good sign from working capital point of view on the part of Saregama Limited.

Some more positives

Promoter holding decent at 59.14%

Mr. Vallabh Roopchand Bhansali holds 1.48% (From the data available it seems he bought in quarter ending March 2016)

Company is paying regular dividends since 2013

Debt on Balance Sheet is NIL

Disclosure

Invested 7% of my portfolio recently.