Hi everyone,

This is my first post here though I have used Valuepickr extensively in the past for my own research. First, my sincere thanks to all you guys! Please excuse me if something in my reply is against the forum guidelines.

I run a small rental company in another industry and hence, am interested in Sanghvi more out of curiosity. My opinion is from the perspective of a business owner. Please let me know where you think I could be wrong.

What I have come to believe is this - Sanghvi is a good business with a large market share, one that is useful to the society, has solid assets that have a long life… BUT… doesn’t earn good return on capital in the long run. Even if you buy it at a 50% discount to intrinsic value, in the long run, you are not going to earn great returns. When I say that, I mean returns are going to be under 12% or so in the long run. My justification below.

In any equipment rental business, these things matter:

- life of asset

- payback period (without considering opex)

- annual maintenance cost

- resale / residual value

- return on invested capital

Also, depreciation becomes a tricky thing. Few assets depreciate fast (electronic rentals), few slow (furniture, cars) and few actually appreciate in value. Going by the comments of management and few industry experts, I think cranes do appreciate in value to some extent (let us keep Chinese cranes out of equation for now, they dont have a track record vis-a-vis German cranes for example).

What that means to me - few of you are going to disagree with me - I am going to ignore depreciation.

That also means, I will use gross block instead of net block for asset value.

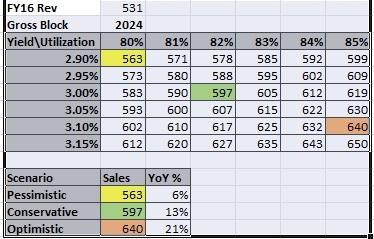

Sanghvi had a gross block of 2040cr as per last concall. In this business, more than 95% of the asset is the rental equipment and hence, let us simply consider the entire gross block as “productive asset”.

Suppose if I have to compete with Sanghvi, I have to put in atleast that much to buy new cranes to build similar capacity, or actually, much more because new cranes cost more. Now, does it make sense for me to do so?

In their last FY, they had 82% utilisation and 3.03% yield which I think is a decent figure and probably slightly above average for the industry. I think the upper end is established at something like 85% utilisation or yield of 3.3% (I think yield was ~4% for crane rental industry before 2008?). That means, you need to put in more than Rs 3 to earn Rs 1 - that gives an idea of how intensive capital requirements are.

On a gross block of 2200 cr, they had a revenue of 531cr and PAT of ~117cr. I am going to add the depreciation of 126cr to that as my asset is not actually depreciating. That is 243cr earned with 2200cr of invested capital - or roughly 12%.

I will repeat that - 12%.

That is a pretty modest return. And this is in what appears like pretty decent year - there have been worse periods for the company. (Honestly, the golden days of 4%+ yields are gone). I don’t think the company is going to earn much more than 10-12% in long run over invested capital.

Now, that brings us to the question of improving returns on shareholder capital (not entire capital). One way is to take loans and increase leverage. However, the interest rate on loans appear higher than 10% - which is what the business is earning. That is not going to bring any economic benefit in the long run as both cost of capital and earnings are roughly same.

Also, any profits from sale of cranes at higher price than value on books is not going to be materially impactful I think.

The other thing is blended yield. Since gross block carries a lot of cranes at lower cost, yield will appear inflated a bit (depends on what % of cranes are older). The newer cranes are actually getting yields of 1.5-1.8 I think. After operating expense and taxes, that will work out to less than 10% returns. That means return on incremental capex is going to be lower.

Which brings me to the opinion that Sanghvi is a good business (crane rental business is not going to go away anytime soon) with a solid market share that it is probably going to retain for a long time (as long as it keeps assets in good condition and invests steadily) - but shareholder returns in the long run are going to be unimpressive.

We can buy it at a good discount to intrinsic value and benefit one time, but that intrinsic value itself is growing at a very average pace.

Agree? If not, do let me know why.

Cheers,

Prem

Disclosure: Small investment to simply track rental companies