A FEW POINTS ON SANGHVI MOVERS

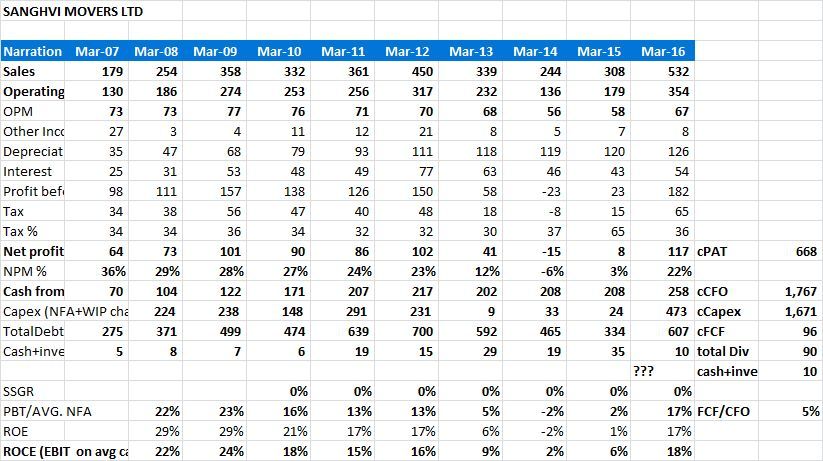

It has a roce of 20 and roe @16%.

The ebidta margin is around 66%.According to mngt it can go to a maximum of 70% only…

The capacity utilization of the cranes is around 83%…maximum utilization will not exceed 89% due to the nature of business…

57% of the turnover is coming from installation of wind turbines…this can even go up to 63-65%…the rest is from power, steel, cement etc No single client has exposure of more than 10% of the topline…

Debtor days in bad days if 2012 /2013 were around 240 days…now it has come down to 84 days…the company gives a 30 day credit…plus it takes another 30-35 days for payment to be released… hence it takes a minimum of 65-70 days…

The capacity expansion of 360 crores was completed in Q3…and the remaining 160 crores will be completed by Q4…all the cranes imported have gone directly from port to clients sites…all the capex is fully deployed… There is a huge demand from wind turbine makers for above 400tons category of cranes… they are scrambling to book the cranes for next year too…demand is also there from power and oil refineries.

Company now has a debt equity of around 0.75…it does not want to go up beyond 1…it has already repaid this year`s debt…and started paying back next years debt too…

The capacity expansion will lead to a good jump in topline in fy 2018…

Sanghvi has 75% of the market share in above 400tons capacity cranes…it has more cranes than all the competitors combined capacity…

There is still unmet demand from wind turbines but they wont go for next round of capacity expansion in a hurry…they need to see back to back booking for the next round of capex. And now the HDFC securities reports anther 300 crores of expansion planned for FY 2018 too…seems like the huge demand is pushing the company towards second expansion.

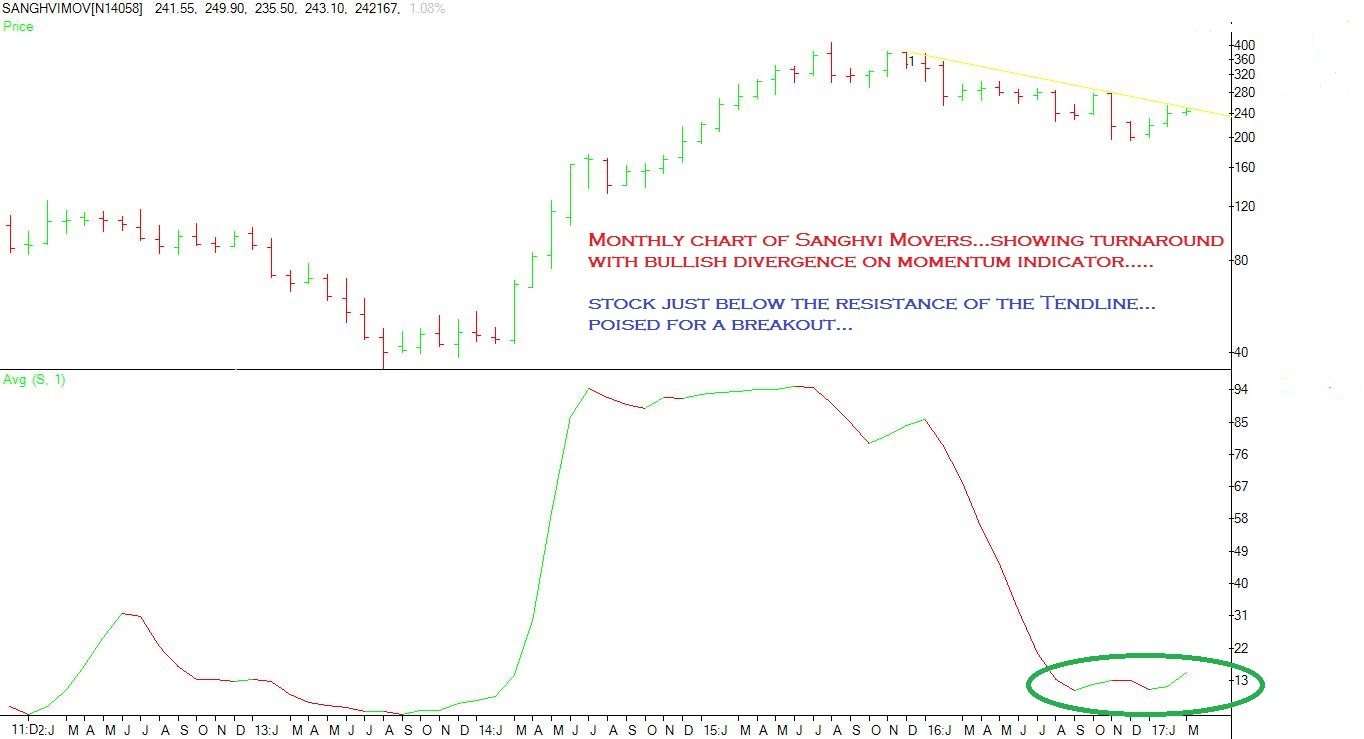

I am going into details of sanghvi movers…because it appears to a safe stock… with low downside risk…and quite high upside potential…there is also very good top line and eps growth visibility for next one year… It is trading at a low p/e…hence there can be both a growth of eps and also p/e multiple…making the stock a potential two or three bagger in the next 12-18 months…

Its a good stock to park a big portion of portfolio…but its a slow mover…may go up in a slow and steady manner… don’t expect fireworks here…its ideal only for proponents of slow and focussed investing only

Disclosure: Not invested…but watching it with considerable interest.

.

.