got this reply from the cs when enquires about the investment in applewoods estate

Dear Sir,

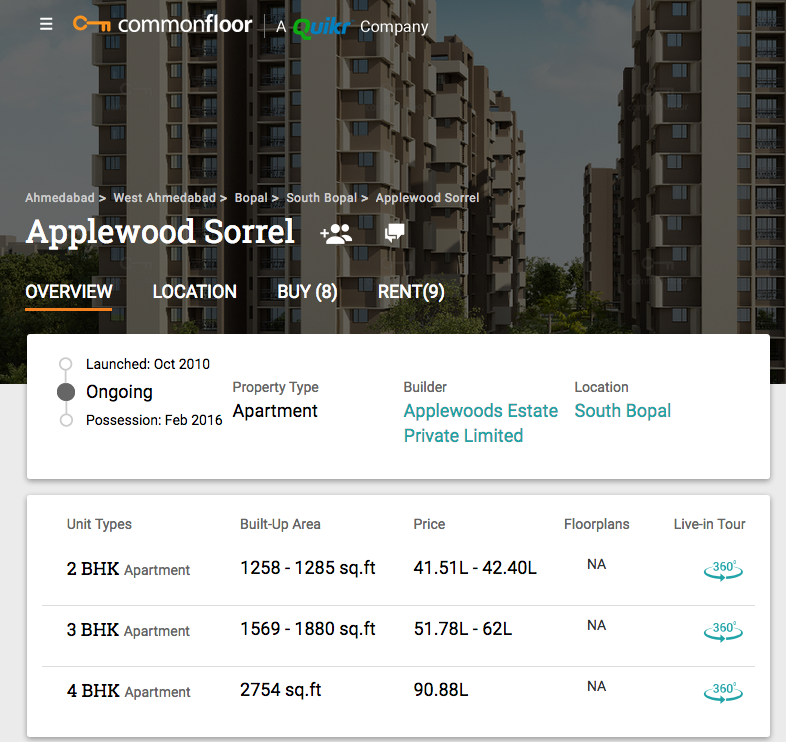

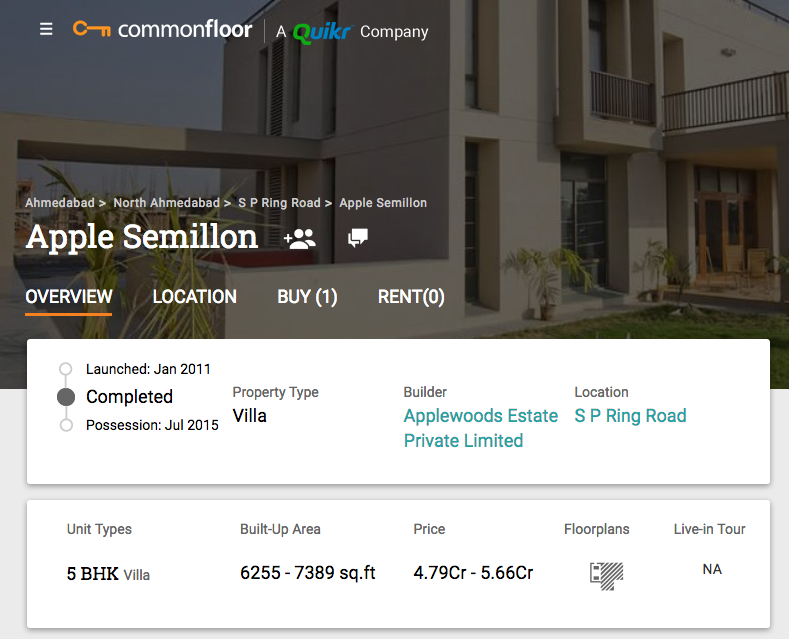

The disclosure to the stock exchanges was made in accordance with the extant regulations and the prescribed format. The details of the investments, as required in accordance with the applicable provisions, made by the Company have been provided in its financial statement. The Board of Directors considering various financial aspects declared the interim Dividend for the F.Y. 2015-2016 @50% (Rs.5 per Equity share of Rs. 10/- each). Few of investors in Applewoods Estate P. Ltd. were willing to sell FCCDs carrying coupon rate of 15.50% p.a. Your Company found coupon rate attractive and purchased these FCCDs from investors. Thereafter, the Company has not invested / purchased on YOY basis in FCCDs of Applewoods Estate P. Ltd. Further, the Company has no plan to invest in Applewoods Estate P. Ltd. in the near future. FCCDs of Applewoods Estate P. Ltd. were compulsorily convertible into equity shares of Applewoods Estate P. Ltd. Hence, on account of conversion of FCCDs into equity shares at a fair value determined by an independent Chartered Accountant, the stake of the Company into Applewoods Estate P. Ltd. has increased and as per the provisions of the Companies Act, Applewoods Estate P. Ltd. has become an Associate Company. Applewoods Estate P. Ltd. is developing an integrated residential Township in the City of Ahmedabad, which is well planned and designed. This Township is spread over ~one hundred twenty eight Acres of land on a prime location on the S.P. Ring Road, Ahmedabad. Hence, the Company believes that the value of its investment in Applewoods Estate P. Ltd. will be enhanced and it will also be beneficial to all the shareholders including minority shareholders of the Company.

Trust this clarifies,

Let’s Achieve,

| Dhaval Pandya | Company Secretary | THE SANDESH LIMITED | Address: “Sandesh Bhavan”, Lad Society Road, B/h. Vastrapur Gam, P. O. Bodakdev, Ahmedabad – 380 054 (Gujarat-India)

Disclaimer:

The message is intended for the address only and may contain privileged/confidential information. If you are not the intended receiver, any disclosure, copying to any person or any action taken or omitted to be taken in reliance on this e-mail, is prohibited and may be unlawful. You must therefore delete this email. Internet communication may not be secure or error free and may contain viruses. They may subject to possible data corruption, accidental or on purpose. The views expressed in this email are solely of the sender and may not be the views of Sandesh as a Company.

From: MrRavikum visitkumaresh@gmail.com

Date: 8 September 2016 at 6:19:15 AM IST

To: cs@sandesh.com

Cc: investorsgrievance@sandesh.com

Subject: Advance intimation for investors query regarding investment

Mr.dhaval Pandya

Respected sir, please refer to my earlier email in this regard even after repeated reminders I have not got any reply from your good office and once again kindly request you to provide some information to my email.

Sir as per your recent disclosure you have informed the exchange that you have acquired the shares of apple woods estate Pvt ltd by way of conversion of the FCCB at a rate of approx Rs 6800 per share.

As a minority share holder of your esteemed organisation I have earlier requested for some clarification in this regard which you have not provided till date.

As per companies act 186 you are supposed to provide the details of the investment made and also the particulars of the investment and some detail about the company in which investment are made.

You have provided about the turnover of the company Apple woods estate Pvt ltd but whereas no details is available about its balance sheet or profit loss statement or even the dividend policy of the company.

Based on the conversion rate the market capitalisation of the Pvt ltd company works out to nearly 1300/1200 cr.

For a minority share holder can you please give some information as regards what kind benefit this will have on the parent company Sandesh ltd. will Sandesh ltd Yoy go on investing its fund in this real estate company were in the promoters have a huge interest.

Sir I once again humbly request you to give some additional information in this matter and or else I would also like to have inform in advance that would be raising this point in your forthcoming AGM.

With regards

R.kumaresh