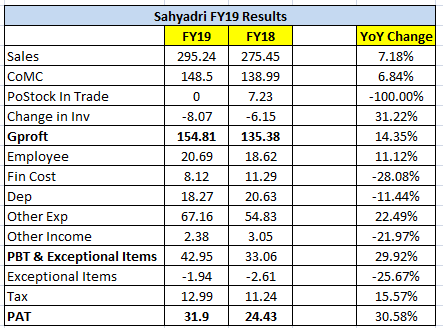

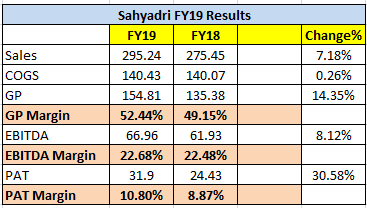

Good Q4 and FY19 for Sahyadri. Annual PAT increased by 30.58% and Borrowings went down from 88cr to 47cr (out of which ~40cr is from directors and promoters at 10.5%).

Ex-Power business, Building Material business has generated ROE of about 36% which is pretty impressive.

Stock still available at PE of 5 and P/B of 1

Would encourage and request others to share their scuttle-but findings on FCB adoption and acceptance among construction players. All views/comments are invited.

Currently problem with sub 300 crore cap stocks is low or no mf participation. Brokers and retail are shaping the price of these stocks. At 5 to 6 pe stock growing even @10% should not be a no brainerbut again compamies scaling capability seem to be visible problem. Management sharing 1 Rs seems peanut but reduction in loan a positive. At best hold and watch.

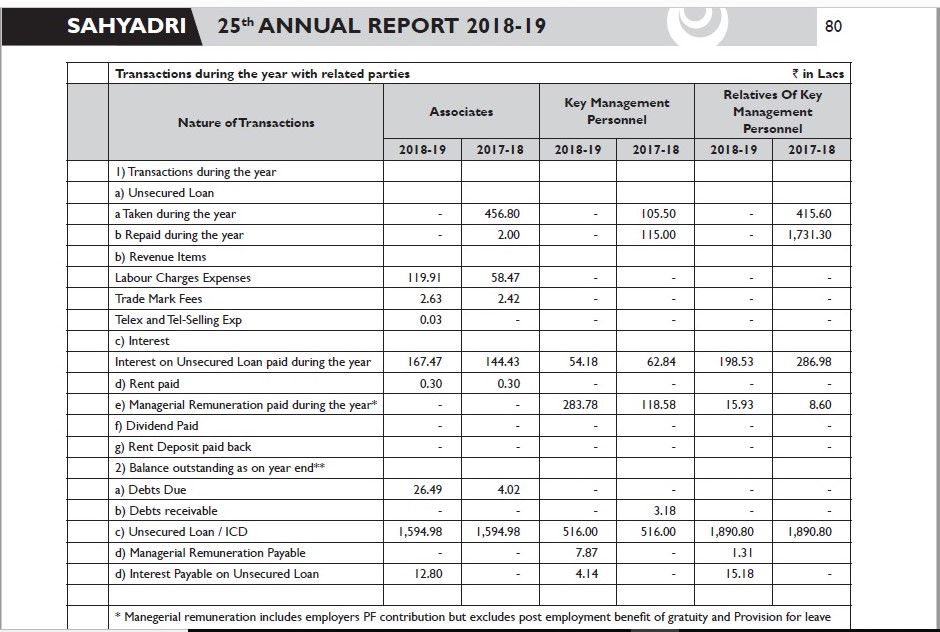

Did you try to calculate the rate of interest charged? Could you please help me that whether the interest paid as shown in the related party transaction should be taken to calculate rate of interest or otherwise? It seems that interest is not uniform.

The Chairman of the company and MD of the company hold directorship in other unlisted company “Poonam Roofing Pvt. Ltd”. I could not ascertain whether the business of this company is in the same segment or otherwise. If in the same segment, why they are running it separately?

It seems that the management is used to revise their minimum remuneration to higher side, whenever they feel there might be the case of inadequacy or absence of profits. Please refer to AR-2017-18 (Page no.2 to 5) as well as AR-2015-16 (Page no. 2-5). Although it was good to see that they have capped their remuneration at 10% of the NP and there exists a policy regarding management remuneration. Further, the management has also opted for HRA, LTC (once a year), Medical expenses (at actual), Free use of car with driver, Free telephone facility, Mediclaim for self and family, Yearly fees of the clubs subject to maximum of two clubs. Your views on this?

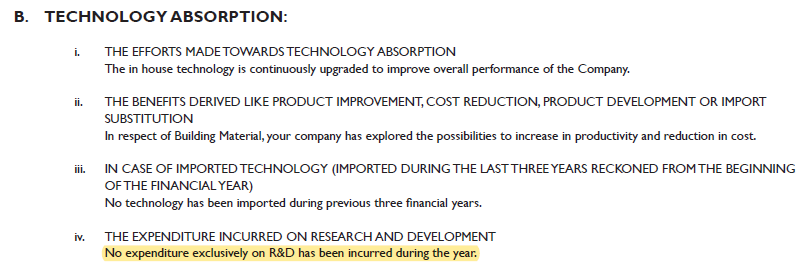

The company talks about R&D, please refer to page no. 30 of the AR-2018-19. However, they have never shown any expense towards R&D. Which kind of R&D are they carrying out? Any idea?

Its given under Notes 15.3 And if you calculate interest portion by unsecured loan amount in related party section, it comes out to 10.5%

Good question for AGM. I’d ask this question at AGM, but I won’t be able to attend. Do you plan to attend?

I’m happy they take it from front-end rather than from back-end using other means. Business is still generating good return ratios even after good paycheck and perks to senior management. I’m fine with it as long as return ratios are good.

They have confirmed on page 17 of AR that not a single dime was spent on R&D and I would not expect them to spend anything towards it in commodity business. It’s a statistical bargain in my view and I don’t have much expectation of it to become a compounder.

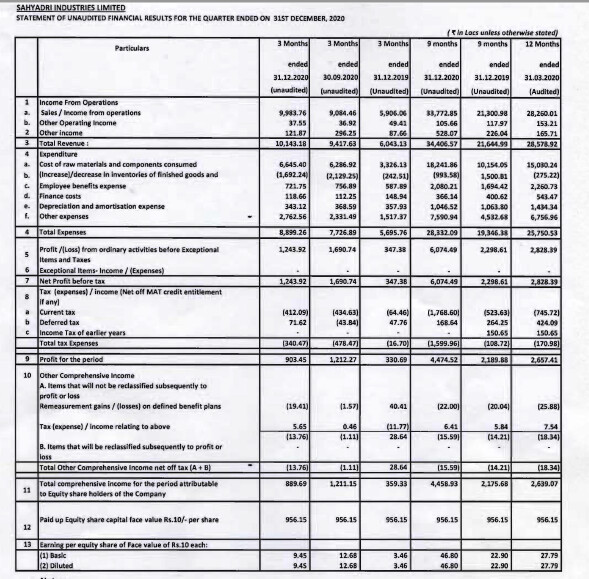

Fabulous results declared by the company in Q1 & Q2 . The half yearly EPS stands at 37.35 whilst the full year EPS of the FY 2019-20 was 27.8. The company has also declared an interim dividend of 15 percent.

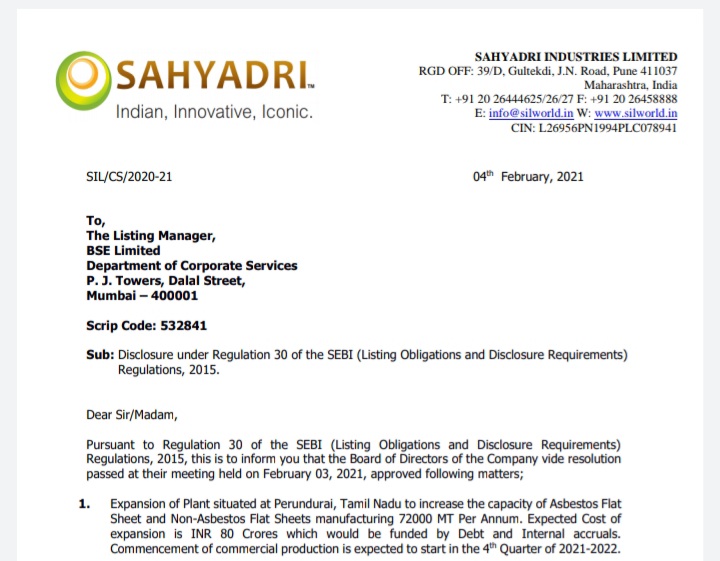

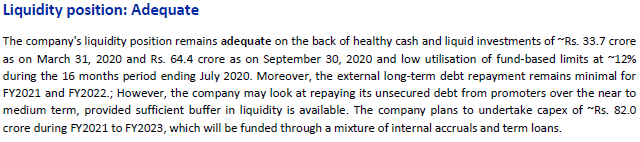

I was reading the recent credit rating report of the company. Here is the report.Sahyadri Industries Limited-crdit-rating-report.pdf (248.0 KB). What I found (a) It becomes debt free, and (b)82 Cr capext plan for next two FY. From Credit rating:.

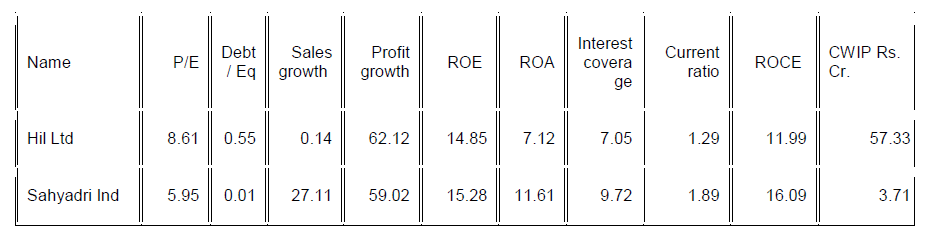

. (from screener).In my opinion, Sahyadri is undervalued compared to Hill Ltd. The positive thing about Hill is it has a CWIP of Rs. 57 Crores. However, it shows 53 crores of other income. I did not study much on this.

My view on the company-One of the reasons for the improvement in the operational performance of the company, is they inducted a professional CEO in January-20 , Mr Maheshwari who has relevant industry experience , who has managed to increase the sales of the company in a short span , which in turn lead to better capacity utilization as a consequence of which all the ratios have started improving. Also they have appointed 2 additional external directors in Oct-20 to strengthen the board, which is also an improvement for better corporate governance going forward as traditionally the mgmt and the board was more family driven.This shows the change in the mindset of the owners of the company , who are willing to change with time and take professional help to run the company and the benefits are seem in terms of all round improvements in the performance of the company.

It is a matter of time, before the company will get re-rated, as the company prefers to maintain a low profile.

Also unlike its peers, it is strictly in roofing products, unlike HIL which has managed to increase its product base in lat 5 yrs , with the result that roofing contributes to less than 40 % of its sales. In roofing business, Sahyadri have performed much better than market leaders like HIL , Visaka and Everest in this financial year. Going by the investor concall of both HIL and Visaka post the latest quarterly results, the roofing business is doing good and considering that Jan-June is traditionally the best period for this industry and with the good growth in rural India, Sahyadri is set to deliver very good numbers going forward, and going by the trend of last 2 quarters , likely to outperform both HIL and Visaka in terms of sales growth and profitability.

Probably they need do a few investor calls going forward for the stock to get re-rated.

Disc- Existing shareholder.

The main reasons highlighted in the credit rating for degradation are as follows:

(1) The improvement in the business risk profile

(2) steady growth in revenues maintaining healthy profitability.

(2) Revenues are expected to improve in fiscal 2021.

(4) Demand from the rural market may increase as normal monsoon leading to better crop

output and thereby higher disposable rural income.

(5) Profitability is also expected to remain healthy for fiscal 2021 despite an increase in raw

material prices & depreciating rupee due to an increase in realizations and an increase in

the overall scale of operations.

(6) SIL’s increasing penetration in southern markets and government thrust on rural housing

(7) The lockdown did not have any major impact on the SIL’s operations as demand is mainly

driven by the rural market. Risks:

(1) Dependence on rural spending, and exposure to intense competition from peers and substitute products

(2) Exposure to the regulatory threat of a ban on manufacture or use of asbestos in end-user markets and in key asbestos- producing nations: SIL remains vulnerable to the risk of a ban on mining and use of asbestos in Kazakhstan or Russia (which are the largest exporters of the mineral).

Revenue at INR 99.83 crores up by 69% YoY basis

PBT at INR 12.43 crores up by 258% YoY basis

PAT at INR 9.03 crores up by 173% YoY basis

EPS at INR 9.45 up by 173% YoY basis

If you look at QoQ then it is slowing down

June > Sep > Dec.

I just followed the result trend and mentioned here.

There is no intention to offend anyone.

Please note that sales trend of this industry is seasonal being related to rural india. The sales increases in March qtr and peaks in June qtr , with Sept qtr being offseason due to rains.

Going by the current trend , the company should be able to do 20 % higher sales in March qtr , with better margins , so can easily end the year with EPS of Rs 62-65 . Also its Net Profit margin of close to 10 % , which is better than its peers. With rural India doing well, it is quite likely that this sector might outperform in the next few years , as with increase in steel prices , steel roofing becomes more expensive alternative, leading to better demand for these companies.

So , all the companies in this sector- including Visaka and HIL will be giving extremely good results in next 2 quarters with better margins.

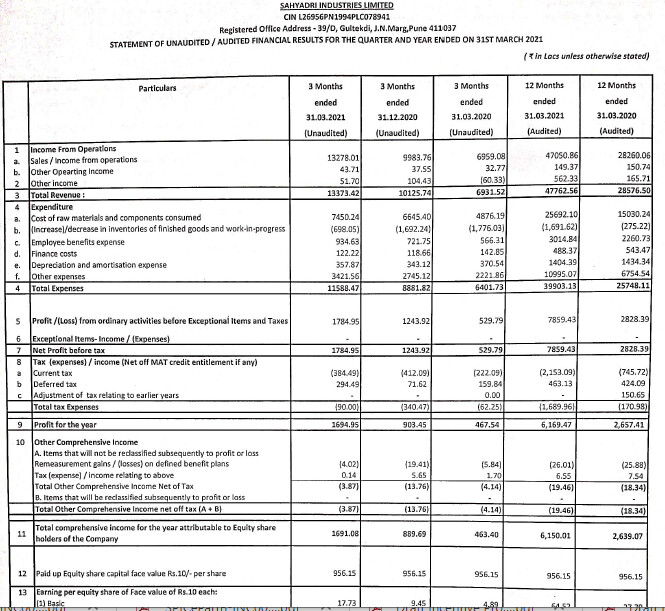

Yes, good set of results and considering the fact that June quarter is the peak season for asbestos roofing industry quite likely that company can post sales of Rs 175 crs plus in the current June-21 qtr ( PY- June qtr-147 crs) , so EPS of Rs 70 plus for FY-22 is easily achievable. So there is scope for company to get re-rated from current level.

Also the balance sheet looks good , with substantial reduction in debt and receivables at around 30 days offers comfort. Given the inventory as on 31st Mar,21 of Rs 113 crs , they should able to give a reasonably good results in the current June quarter.

.

.