Did anyone attend the AGM.

AGM is on 28th Sep and has not happened as yet.

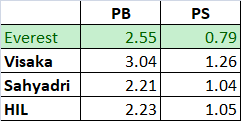

I believe Everest Industries seem to be well positioned for the next few years. In terms of valuation, Everest is better than Sahyadri with respect to their capacity and size.

The govt’s solar project might hugely benefit Everest.

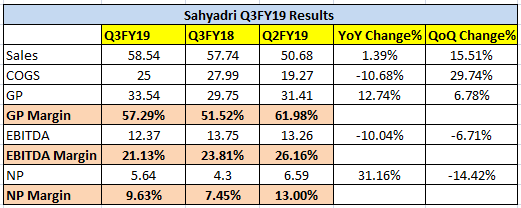

Sahyadri posted very good numbers, however, I am confused about the Excise Duty. It was a big component until last year but this year there is no excise duty, any idea why? This is one of the reasons for good results.

Increase in product awareness and adoption of higher margin Fibre Cement Boards (FCBs) lead to recent run-up in Indian roofing businesses. I dug deeper to find whether FCB has potential to be a game-changer in construction building material industry. If you are interested to read what I put together, please click here. I am looking forward to any questions/comments.

Disc: holding Sahyadri.

3 Likes

Looks like 2016 numbers had excise and 2017 are net of GST. Superb performance by Sahyadri.

Disc: Invested

The presentation material has been nicely done. You can maybe add the sales revenue and margins for the companies to give a better perspective as to how the individual company and the industry is growing in the past 5 years . Today Visaka mgmt came on CNBC and indicated a topline of Rs 1000 crs for current year, so it seems the industry is doing well.

My view is that Sahyadri should end the year with sales of Rs 275 crs of sales with EPS of Rs 30 and cash EPS of Rs 50 . It has an upside potential of 50 % from current levels over the next 6 months.

2 Likes

Visaka Inds-Q3 Update.pdf (1.1 MB)

The enclosed report contains useful data on the future growth prospects of FCBs and detailed data on market share of the industry players.

1 Like

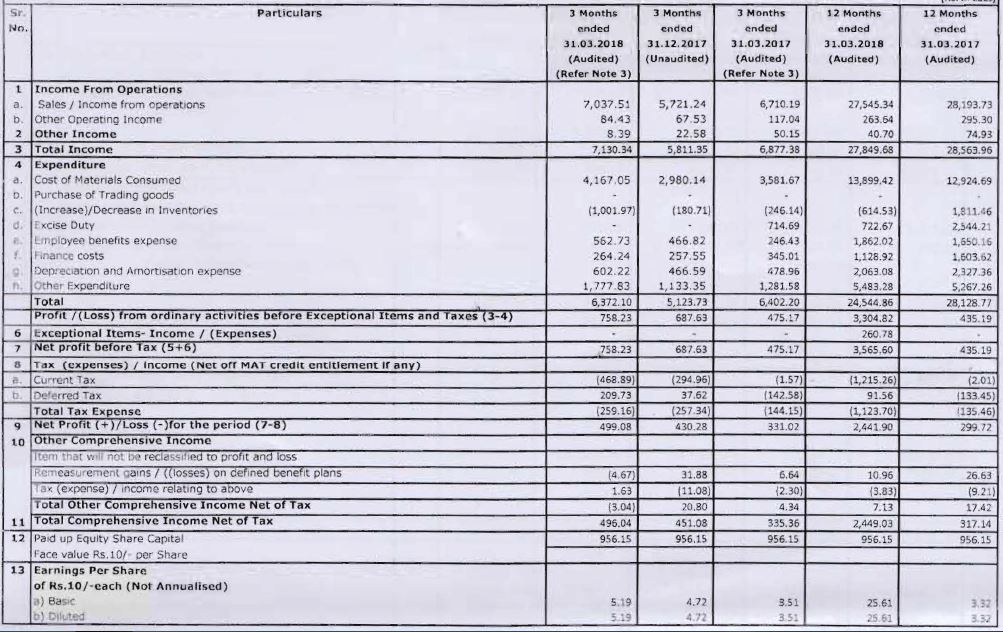

Results are out and they seem to be pretty decent. Though the market reaction isn’t positive and the stock is getting beaten down consistently since the results.

Any thoughts on the results and the ensuing stock price meltdown?

Yes, this is after long time that company has not posted loss in 5 consecutive quarters. Seems like young management is turning around the business in right direction. IMO - stock price is being dragged down along with ongoing mid-cap and small-cap correction.

Disc: invested

The company’s sales and profits are at the same level as these were way back in 2010. Valuation optically looks cheap with a PE of 8.11. Is this a typical cyclical business where low PE ratio means the end of a favorable period because of the disproportionate expansion in the earnings in the upturn of the cycle? OR the company is moving towards having sustained sales and earnings growth and on the path to achieve traits of non-cyclical business?

Price as on 21st Aug 2017 was 143 translating into the then PE of ~16. Today price is 239 with a PE of 8.11. Over the last 12 months, the stock price moved from 143 to over 300 while the PE ratio kept declining.

Request senior members such as @ayushmit to throw some light on the inherent business model of the company.

2 Likes

I have looked into the roofing players (Sahyadri, Visaka, HIL, Everest) and will share my understanding of the business model here.

Big portion of their revenue comes from roofing business. Demand for roofing products is mainly driven by rural areas and the demand is mainly dependent on 1) Housing for all initiative 2) Rural economy 3) Prevailing Steel prices (substitute product; steel metal roofs) 4) Rain. So because of above dependencies the demand follows rural cycle making roofing business cyclical in nature. On top of the business being cyclical - there is overhang of asbestos fear in the mind of market participants keeping overall valuations lower.

Lately there has been acceptance and adoption of Fiber Cement Boards (FCB) & Panels in the construction market. There are many applications for FCBs and can prove to be a game-changer for sluggish roofing businesses. It is a higher margin product when compared to roofing products. FCB industry today is at ~1000cr and has grown at 15-20% CAGR over last 5 years. Below are few links/sources that should help to understand the possible potential of FCB industry. Third item is my post on FCB opportunity on my blog.

- http://www.plyreporter.com/article/10019/fcb-fibre-cement-board-the-fast-emerging-interior-exterior-panel-product-at-plywood-retail

- In Q1FY19 Everest’s earnings conf call, starting at 47 minutes of the call, CEO Mr. Sanghi beautifully explains the prospects and potential of FCB in India.

- https://rationalsideofpendulum.wordpress.com/2018/02/14/fibre-cement-board-changing-fortunes-of-sluggish-roofing-businesses/

My guesstimate is that FCB revenue contribution for most players would be 10-15%. With increasing awareness, it is growing at faster rate than roofing business. It will take some time for FCB to catch-up with roofing numbers and only then the market perception would change.

Overall, Sahyadri has posted strong set of numbers for FY18. If one excludes Windmill numbers, Sahyadri’s FY18 numbers look excellent!! Management has mentioned in FY18 annual report that enough spare capacity is available and most probably no need for any CAPEX in next 2-3 years.

Would encourage and request others to share their scuttle-but findings on FCB adoption and acceptance among construction players. All views/comments are invited.

Disc: invested and hence biased.

4 Likes

Thanks for your detailed response.

Rgds, Ranjan

1 Like

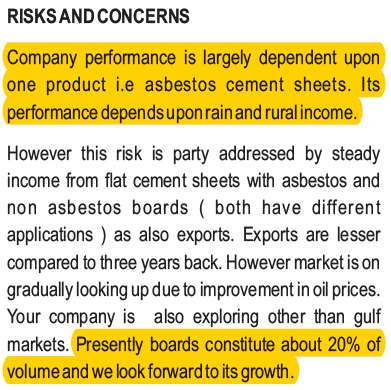

@rupaniamit, Sahyadri is posting higher margins is due to their sales is 95% FCB, which has severe Occupational health issues due to the asbestos chrysotile. Any ban on the fiber will take toll on SIL.That is the reason market is not rewarding with higher valuation. As the fiber is imported due to INR drop, I doubt the margins will continue down the line. Chrysotile makes up around 50% of the cost of material.

I don’t deny asbestos overhang on valuation. I have clearly stated above about it. Also agree with margins coming under pressure with INR depreciation.

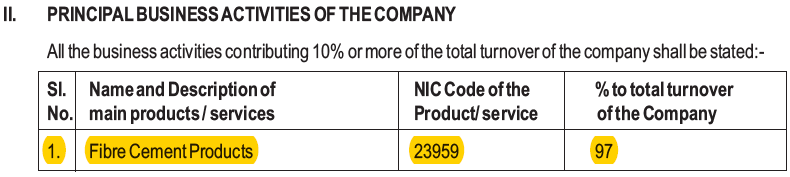

It’s 97% of sales in Fibre Cement “Products” which includes asbestos + non-asbestos products. Presently 20% of their volume is in boards which is non-asbestos business. Below is the screenshot:

Have you looked into possible value migration that can happen to boards in construction world?

1 Like

Asbestos substitute materials

What I heard many advanced economies already made the transition, but we are still compromising safety for cost.

Link to Q2FY19 result: https://www.bseindia.com/xml-data/corpfiling/AttachLive/aaee529b-9b5b-42fa-b0ed-9d02e916f09c.pdf

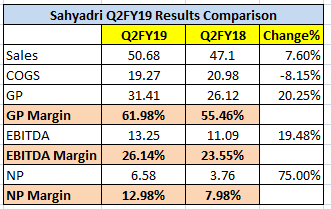

Improvement in margins is surprising. Borrowings down to 44cr from 96cr in first six months of FY19. Lower debt gives some comfort in the business. Company available at P/E of 6-7 and EY of 17-18%. Growth in sales would have been a good trigger. But still with such improved operational performance it will be interesting to see how long such valuations will continue.

Disc: invested

1 Like

Sahayadri has a higher Depreciation to sales at 8 to 9% of sales compared to industry average of 3-4%, Could someone who is following it closely throw some light.Thank you

Higher Other Expenses of 16.02cr compared to 13.08 YoY and Higher Exceptional Gain of 1.94cr this quarter. Lower EBITDA and gross margin.