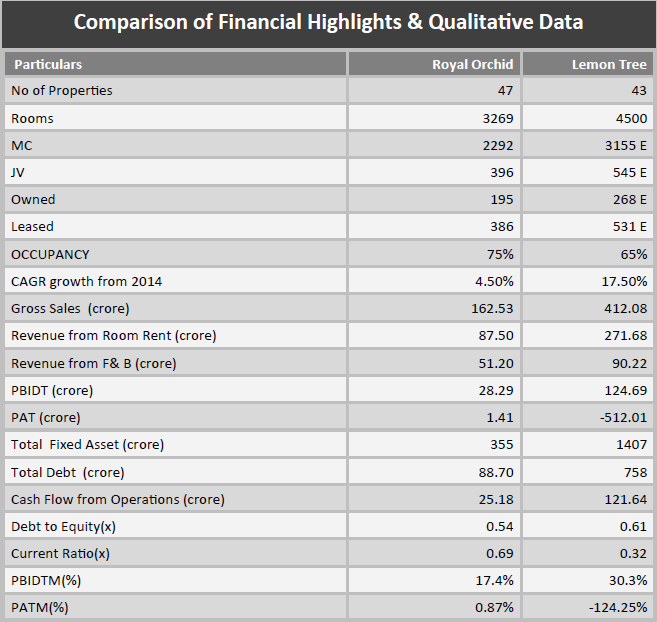

Royal orchid is just under half the size but the difference in Market Capitalization with Lemon Tree Hotels is huge!

Disc : Invested in Royal Orchid

Royal orchid is just under half the size but the difference in Market Capitalization with Lemon Tree Hotels is huge!

Disc : Invested in Royal Orchid

Industry Overview

Tourism in India accounts for 9.6 per cent of the GDP and is the 3rd largest foreign exchange earner for the country. It is expected to grow at 16% CAGR to reach INR 2,800 thousand crores in 2022.There are multiple growth drivers in the tourism and thereby in the hotels industry. The government has allowed 100 per cent FDI under the automatic route in the tourism and hospitality sector, including tourism construction projects such as development of hotels, resorts and recreational facilities.

International hotel brands are targeting India. Carlson group is aiming to increase the number of its hotels in India to 170 by 2020. Hospitality majors are entering into tie ups to penetrate deeper into the market, such as Taj & Shangri-La entered into a strategic alliance to improve their reach & market share by launching loyalty program aimed at integrating reward program customers of both hotels. Berggruen Hotels is planning to add around 20 properties under its midmarket segment ‘Keys Hotels’ brand across India by 2018. Hilton plans to add 18 hotels pan India by 2021, along with 15 operational hotels under its brands namely Hampton, Hilton Garden Inn, Conrad, Hilton Hotels & Resorts & DoubleTree by Hilton. Marriott International plans to open 30 new luxury hotels. As of November 2017, the company operated 93 hotels in India.

In June 2016, the Indian government approved 150 countries under the Visa on Arrival scheme to attract additional foreign tourists. During Jan-Sept 2017, a total of 10.67 lakh tourist arrived on e-tourist Visa as compared to 6.75 lakh during the months of Jan-Sept 2016, registering a growth of 71.0%. Foreign tourist arrivals (FTAs) in India increased 15.5% to 71.20 lakhs compared to 61.63 lakh in the same period.

Medical tourism is another major area of growth. The country is witnessing 22-25% growth in medical tourism. Indian government has also released a fresh category of visa – the medical visa or M visa, to encourage medical tourism in India. Indian medical tourism is expected to reach USD8 billion by 2020.

Domestic expenditure on tourism has grown significantly. Indians are travelling much more frequently for both business and leisure and has been aided by much better connectivity of Tier-II cities by the low-cost airlines. Meetings, Incentives, Conferences and Exhibitions (MICE) segment is another key growth segment.

Company Overview

Royal Orchid Hotels Ltd (ROHL) is a 31-year-old company which owns and operates hotels in India. It is promoted by Mr Chander Baljee, who is a IIM Ahmedabad alumnus with over 40 years of experience in the hotel industry. Key brands include Royal Orchid (five-star), Royal Orchid Central (four-star), Regenta Hotels (four-star), Royal Orchid Suites (service apartments) and Regenta Inn (budget hotel). It currently operates 47 hotels across India with plans of reaching 50 in FY18.

ROHL operates in 33 cities with a 1.4 lakh loyalty members. Management is planning to grow more by management contracts which is an asset light business model. It requires no upfront capex and can break even at operating level within 1 year.

GST for hotels with room rates between INR 2501-7500 has been reduced from 21% to 18% which is expected to provide a boost by increasing overall affordability.

Currently, the company manages 3269 rooms and is operating at a utilization of 76% in Q2FY18. It expects to add 300 rooms this year and another 1000 rooms in FY19.

The company signed a pact with UK’s Bespoke Hotels recently. Under the agreement, Royal Orchid will now offer its guests hundreds of hotel options across multiple global markets and Bespoke will promote the Indian hospitality firm to its guests.

ROHL has two land parcels that it may dispose off – one in Tanzania and another in Mumbai. If it can do so, it may reduce its debt significantly.

What is Changing?

The hotel industry is slowly turning around after many years of sluggish or negative growth. New supply has been low, and demand is inching up. This is causing significant uptick in occupancy rates across the industry. Given that new properties take between 2-3 years to come up, the next phase will see hardening of ARR (average room rates). Hotels with a good brand name with pan India presence and in the affordable luxury segment (3-5 star) would be in great demand.

Risks

Lack of revival in domestic growth can hinder growth. Increase in supply through formal or informal channels (like Airbnb, oyo rooms etc) can keep a lid on ARRs. Any geopolitical incident can severely impact foreign tourist inflow. Large and foreign brands coming into India can provide stiff competition.

Financials

Screener Link: Royal Orchid Hotels Ltd financial results and price chart - Screener

The company seems to be in the initial stages of an industry turnaround. It was loss-making between 2012 and 2016 at both PBT and PAT levels. Debt has been reducing over the years and management is focused on reducing it further. In 2017, it has made a turnaround and posted a profit. With better times for the industry, fortunes for the company seems to be looking up.

DISCLOSURE: INVESTED from lower levels. This post is for discussion purposes only. Please do your own due diligence or consult an approved investment advisor before investing in any stocks.

I also have a small position in Royal Orchid hotels (< 3% of pf) from lower hotels.

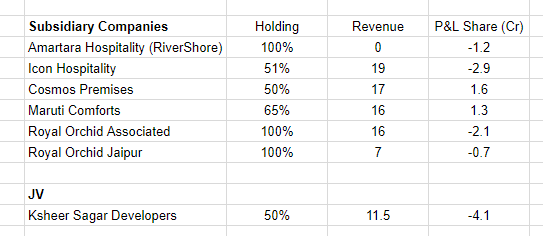

What has kept me from increasing the stake in the company are consolidated numbers as previously pointed by @Mridul & @Nolan. Following is the split up for FY17 →

The most worrying is the last one - Ksheer Sagar Developers where loss is 4Cr & it is not exactly into hospitality business. I have no clarity over what is happening in this JV.

Following are conslidated numbers provided by management in Q2 conf call →

Q2FY18 - Consol. Numbers

Q1FY18 - Consol. Numbers

Even here, they do not talk about Ksheer Sagar Developers individually.

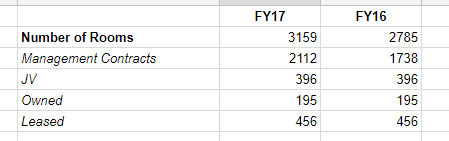

Following is the split of rooms across different categories →

Disc - Invested, not a buy or sell recommendation.

There are some unanswered questions regarding subsidiaries here though my bet is on the valuation vis a vis peers.

SEBI has cleared Lemon Tree IPO for about 20 cr shares. It is expected that IPO may be priced around Rs. 57-63. Total issue size may be around Rs.1200 crores for 25% equity thus valuing the company around 4800 cr.

Now, just compare the numbers of Lemon Tree with Royal Orchid whose market cap is just around 500 cr on 3 parameters.

No. of hotels - Lemon Tree ~40 / Royal Orchid ~47

Cities - Lemon Tree ~24 / Royal Orchid ~32

No of keys - Lemon Tree ~4300 / Royal Orchid ~3300

Lemon Tree is still a loss making company (though losses are shrinking steeply during last 3 years) whereas Royal Orchid is profit making company with excellent track record of dividends.

In Management Contract, revenue is not accounted for; only the mgmt fee is accounted which is usually 3% of sales or ~8% of Gross Profit. This is being booked in a separate wholly owned Subsidiary - Royal Orchid Associated Pvt Ltd. Contract hotels numbering more than 32 and revenue from those hotels are not included in the books. That`s why topline looks somewhat subdued. Auditors objected to it and now with effect from April 1 '2017 they are recording revenue on net basis (like Byke). Hence there is a steep downfall in their topline.

Royal Orchid Hotels Management is very sound and their statutory auditors are from “Big 4” Deloitte. Therefore, they have a sound accounting system.

I understand that comparing a highly expensive company with a less expensive one doesn’t mean the second company is undervalued. Though, there is a lot going well for the hospitality industry. Commentary has improved; occupancy improving; ARRs improving. So my investment rationale is a ix of peer valuation and industry tailwinds.

Dis: I took position in ROHL ~140; averaged up couple of times in last month around 175/180.

I think this is the primary reason for the difference in revenue between the two despite being of comparable size.

I believe royal orchid will benefit from reduction of tax to 25% announced in budget as sales is less than 250 crore.

Q3 FY18 Concall Summary

- YoY occupancy has gone up from 72% to 79%; ARR has gone up from 3900 to 4200 (owned hotels)

- All accumulated losses wiped out; will be paying taxes; subsidiary which manages owned hotels has turned profitable

- At a consol level, co is now profitable; the worst is over

- Trying to reach 50 hotels by end of FY; next year target is to add 15 hotels (about 900 rooms)

- Management fees income is adding about 1 cr to the bottomline

- Managed rooms occupancy is lesser by 2% as lot of new properties has been added

- Mumbai land parcel - 2 term sheets are there; waiting for DP; also looking at outright sale

- Consol Rev -

○ 9M - 137crs (vs 121 cr)

○ Q3 - 52.51 (vs 45.51)

- Consol EBIDTA -

○ 9M - 20.29 crs (vs 12.73 cr)

○ Q3 - 11.65 (vs 9…15)

- Consol PAT -

○ 9M - 8.12 vs 0.12

○ Q3 - 8.05 (vs 4.80)

- Cashflow From Operations Q3 - 11.31 cr

- Debt - 36.68 (standalone, vs Mar 2017 - 41.53); 76.55cr (vs March 2017 - 81.08)

- Occupancy has peaked; ARR can improve by another 8-10%

- Loyalty Member addition - 9000 new members in Q3

- Regenta brand is doing very well

- Management contract business cost is usually fixed cost for sales office etc - 2.14cr, Rev 3.88cr

- Promoter holding has reduced due to personal reasons- no further plans to reduce stake

Hi Abhishek, can you please let me know if there is a way to calculate the cash flow from operations on Q basis.

As I can see the - Cashflow From Operations Q3 - 11.31 cr in the above summary.

I was under the impression that the only way it can be seen is the Annual report of the respective company.

Thanks,

Pandi

It was mentioned in the Q3 concall.

Valuation is about 8x Royal Orchid , whereas sales are about 2.5 x . Besides Royal Orchid makes money whereas Lemontree does not.

Royal Orchid Hotels is eyeing to own 80-90 properties by 2020, including 2-3 overseas, over the next three years, a top company official said.

The company currently has 49 properties in 32 cities across the country with 3,200 rooms.

We will add 15 more hotels to our portfolio to take the total to around 65 properties next year with 4,500 rooms.

Going forward, we are going to focus in states where we are not present or have few properties. We see a huge potential in Tamil Nadu, Telangana and Andhra Pradesh.

With 6500 Cr, you can buy Royal Orchid (EV 550 Cr, Sales 160+Cr) + Asian Hotels East - 2 marquee Hyatt properties (EV 400 Cr, Sales ~200 Cr) for a total of say 1000 Cr . Both already have strong positive operating cash flows and conservative expansion plans. And be left with 5500 Cr Cash

OR you could buy Lemontree ( EV - 6500 Cr, Sales 400 Cr, no operating profits, over 30% of sales from 2 properties) and be left with no cash.

With the onset of ‘strong’ upcycle (2nd part of upcycle), cyclical industries start attracting investments. Here is an ex. i came across. Good thing is that hospitality industry has longer cycles than that of metals or sugar. We still have good 2-3 yrs of upcycle left to play on.

The hospitality sector is beginning to get into a bull cycle, hopefully for the next 1-2 years, before the supply again comes onstream.

Any suggestions what should one particularly look for when selecting a a hotel stock from the multiple choices available? Thanks.

Looking at hotels is slightly difficult, because you need to analyse them on a case by case basis. Because each hotel in India is different. Some of the things to see is what types of properties are there, which cities, what is the main source of revenue, the capacity utilization (current and at peak historically), average room rates (ARR) for the city and type of hotel.