I think the rally in crude prices may have a negative impact on the margins. Welcome views of other members.

Disclosure: Invested

Regards

SJ

I think the rally in crude prices may have a negative impact on the margins. Welcome views of other members.

Disclosure: Invested

Regards

SJ

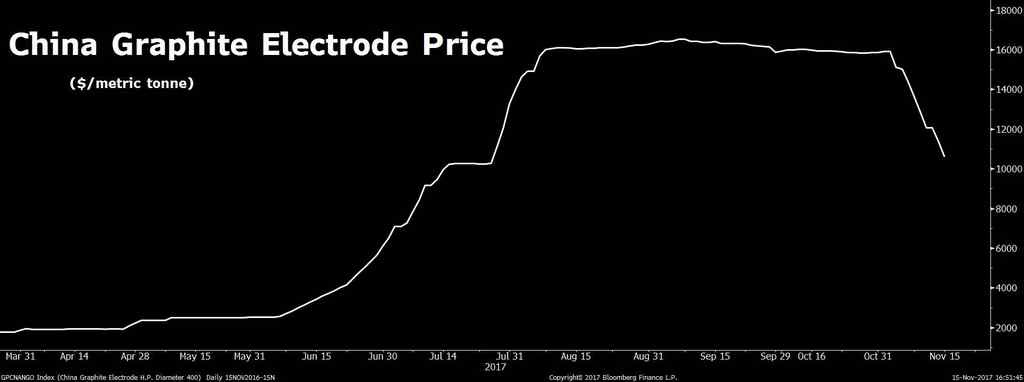

cpc prices have not fallen at all in the past one week…only electrode prices have fallen 6 per yesterday. no reason to panic I think.

How do you track CPC prices? Thanks in advance.

My view, No reason for any panic.

Out of 3 demand drivers below

i) Aluminum smelters

ii) Lithium Ion batteries for EV (Graphite anode requires CPC as raw material)

iii) EAF Manufacturing of steel (HEG and Graphite run into crazy valuations because of this)

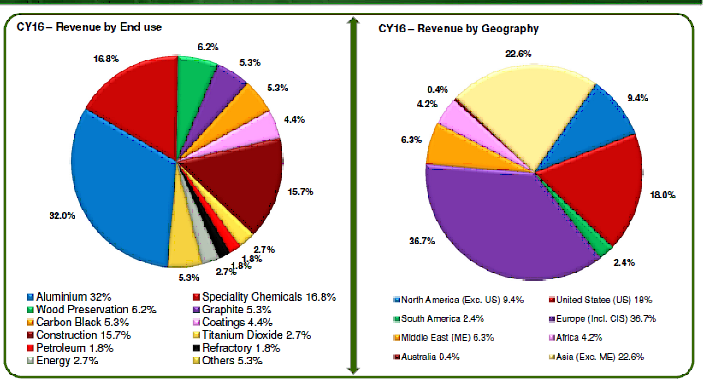

As of now,only Aluminum smelters is contributing to RAIN revenue and that is unchanged.If lithuim ION starts contributing that will add fuel to fire but I am not sure on what is the possibility. May be any SMEs can answer.

i am of the view, Increased graphite production in china may increase demand for CTP and CPC. Any contra views?

All in all , dont see any reason for panic. Existing demand for rain products is intact and future demand may vary based china dynamics which may increase/decrease demand for Rain products.

Yes - Mr. SP Tulsian’s. Here is the full video with negative comments.

It would be great if Mr.Tulsian can help us understand what is the share of graphite in RAIN industries revenue.

I figured out it was Mr Tulsian. But didn’t want to give it undue importance.

He gave negative comments about Graphite India too, but it’s trading in green today.

I think it’s the absence of institutional buying in Rain. And retail investors are in a stampede to get out.

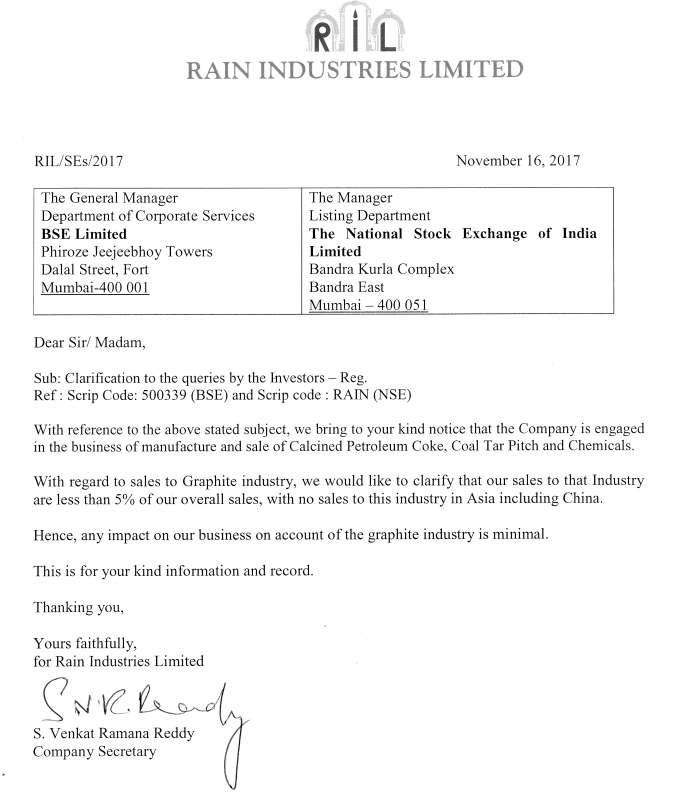

as per rain industries promoter it is less than 5%

SP Tulsian has given unresearched views on Rain Industries. As soon as/if rain hits my buying range I will be adding more. I believe 200-240 will give me some decent value. Personally I think now that there has been a major correction, we will see some instituitional buying taking place. Dare I say, SP Tulsian himself may end up accumulating stock. This is why retail investors struggle in the market. Investing is a difficult project to execute. Real money, real serious. I think macros are in place for Rain and they will scale new highs over the next two quarters. They are also going to restructure debt at a lower rate which would mean that reduction in intrest payment will flow straight to the bottom line.

In my opinion 200-240 would be oversold position.

Rain industries has issued a circular and it has negligible impact because of Graphite prices. I think Tulsian wants to accumulate stock and went ahead and issued a statement on the channel, so that retail investors can tender and can bring it down …

Here is the circular from the company

http://www.bseindia.com/xml-data/corpfiling/AttachLive/8b8268f6-646a-4469-8d9c-fac672d4f853.pdf

The stock is fundamentally very good.

If this was not enough , Summarizing the financials

In the last 5 Quarters , Sep quarter HAD

Highest PBT At Rs 419.57 cr which has Grown at 111.02 %

Highest Net Sales Quarterly at Rs 3,050.81 cr

Highest PAT Quarterly - At Rs 253.41 cr ,Grown at 74.6 %

Highest PBDIT - at Rs 673.83 cr.

Highest Operating Profit to Interest - at 4.61 times

HIGHEST ROCE for last 5 half yearly period at 13.42%

LOWEST D/E in the last 3 years at 2.04

OPM highest in last 5 quarters at 22.09

and offcourse HIGHEST EPS in a quarter at 7.3 rs

just spoke to the investors relations of the company… absolutely no reason to panic according to him…he said there has been no change in the business conditions since the last quarter concall…he didnt want to give specific numbers but things are status quo…they being a converter have steady margins and in a tight market, the margins could inch up to the levels seen in the previous quarter…

@all: just for understanding - If graphite electrode prices are going down, isn’t it natural that prices of key raw materials of electrode i.e. Coal Tar Pitch and CPC (core businesses of Rain) will also go down globally . It should hardly matter whether Rain supplies to Asia or Europe or Americas because at the end these are global commodities and effects will be seen across geographies…

As such, below is the kind of steep decline graphite electrode prices have seen in the last 2 weeks. Want to understand as to why key raw material prices globally will remain unaffected.

Looking for more perspectives/rationales.

Disclosure: Not invested. Monitoring and trying to understand.

Graphite is just 5% of Business and as such price of end product cannot determine the price of raw materials. It’s like price of laddo determines the price of sugar which to me is not correct.

Graphite electrode is used for Steel making via EAF and their main raw material is needle coke…whereas Rain CPC / CTP main usage is in aluminium industry so that needs to be tracked rather than graphite

Never been a fan of TV experts. Especially the ones who are most confident (without refering to anyone in particular). One big reason for giving a rash overconfident call on a stock is that these people are never made accountable for the calls they miss. IMHO, disclosures of holdings are just not enough. TV Channels should maintain thorough stats of hit and miss averages of all so called experts featured on their shows, and it should be revealed to the viewers whenever stock/market calls are made by respective experts. This is just like the batting averages of the cricketers which are to be used for selecting a winning team combination. I bet a large number of them would find it hard to maintain both the average and the TV jobs. Market/Stocks work on countless variables simultaneously. It is near impossible to factor in all independent variables to determine the precise trend of future stock price. This gets exemplified in the case of Rain Ind too where just about a week back Motilal Oswal gave a buy call and Mr. Tulsian gave a sell call. I personally dislike those calls which do not present a balanced view on the stock. For all my money if experts, who are confident on their calls, know so precisely which way the stock is moving, then with due respect they would be billionaires already and they won’t need to feature on petty TV shows. It leads me to believe that they need a forum to swing larger public opinion on their side to run their/their clients’ trades on the positive side. Rain Ind has run up fast and a correction is not bad at these levels. The commentary has been positive overall on future business prospects. Graphite prices may have come under pressure in last week, but without properly analyzing its impact on Rain’s porfolio, it would be rash to take a strong bearish call within days of the amazing operational performance shown by the Company.

Disc: Invested. Views are personal.

I agree…analysts just simplify variables which affect a stock and give

out rash sell calls…in their last concall, the CEO of Rain management had

said he had been to China and nobody there seems to have an idea about the

closure of CPC factories due to pollution, then how come a TV analyst

sitting gives such informed calls…

their latest call indicates lot of tailwinds

Correction is good for a stock. But there’s some level of manipulation going on here.