Is this applicable for retail investors ?

No. Internal employees and directors of the company should not trade the stock for the next one month

Why would the management do that.?

Is the volatility in price movement a concern for management ?

And moreover why the Management is releasing notices on shares frequently

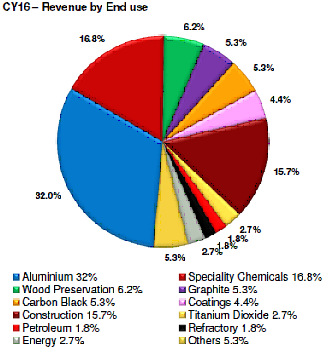

They came up with a clarification earlier that revenues from graphite is just 5 %

1 Like

I think people will argue either ways .

It’s a common practice to send out a notice so that the employees familiar with the results don’t trade based o. Inside information. Nothing wrongnin it.

The fundamentals are intact so don’t bother on y the recent fall . It’s a general correction and Rain is no different to general sentiment . Look at Graphite it has posted humongous profit almost 18 times ( yes 18 times and not 18%) yoy and still ended in red. Operator proposes investor disposes.

2 Likes

Why is Rain consistently going down. Anything wrong with the company - or is it just technical correction.

A 20% tariff rate introduction by Govt. on export of graphite electrodes explains the plight of HEG and Graphite India.

http://events.steelmintgroup.com/indian-govt-introduces-20-tariff-rate-graphite-electrode-exports/

Rain having a small percentage of revenue from the segment should not be severely affected. It downfall seems purely sentiments driven as the three stocks mentioned have moved almost in tandem in near past.

2 Likes

Thanks . As per my understanding, Rain produces “Carbon Products including Calcined Petroleum Coke (“CPC”) and Coal Tar Pitch a(“CTP”),” used primarily in Aluminium Industry. Graphite, as produced by HEG and Graphite India, is used primarily in Steel Industry. It appears that the export duty by GOI is on Graphite used for Steel and not CPC used in Aluminium. If so - GOI action may not affect Rain.

1 Like

Rain has approx. 5% exposure to Graphite industry.

2 Likes

Thanks for sharing. With just 5% exposure to Graphite, there appears to be no threat to Rain at all. This price dip appears to offer great opportunity to add more.

Disc: invested from Rs 150 to 450!

Check out @acosgrove003’s Tweet: https://twitter.com/acosgrove003/status/959629241431281664?s=08

Expect CTP prices up by 20% in 2018

And CpC prices by 40%.

Good time to look at considering the recent fall.

4 Likes

Very interesting interview - highly positive for stock market in general, and Rain in particular.

https://aluminiuminsider.com/indian-aluminium-firms-banking-clusters

Capex by Nalco and vedanta should further increase demand of CP coke. Good for Rain and Goa carbon.

How do you perceive the Q4 result of Rain Industries? If anyone has attended the con call could you please summarize the highlights and gist of management outlook for the next FY?

I looked at the results and the profit has tripled comparatively speaking QoQ and Yoy basis, but the share price started falling post results.

Disclosure: Invested at price of 380/- and a neophyte to stock market.

Results for Rain looks good, which was not in the reckoning of a good performing company last year.

Out of the company’s 3 business segments, Carbon products has witnessed tremendous growth in 2017, with an increase of 115% on a full year basis and also by 168% on a y-o-y basis.

At the same time, the growth on a q-o-q basis is only 3.1% for Dec 2017. Does it imply the growth is slowing or is it not appropriate to compare q-o-q for such businesses? Need to see next quarter results to understand the trend better.

The chemicals business saw a good growth on both measures but on a yearly basis, it is down by 60.8%. Maybe the company has not focused on the chemicals business in the first 9 months of the year, but is giving its due importance starting last quarter? very possible.

The cement business is still comparatively smaller and has not witnessed any growth.

If the company is able to deliver a reasonable full year growth of 20% for the current calendar year, then the stock could move towards Rs. 650-750 by Dec 2018.

2 Likes

Not sure of the con call, didnt see any notice to that effect.

Here is a link to media release. The CY17 consolidated appears great compared to last year.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/d148f9cf-b9d7-4c13-9ff3-e82ffc11ac8b.pdf

The highlighted statement could explain the focus (or lack of it) on chemical business

Discl: Invested from much lower levels than prevailing market.

Rain Industries Management Conf Call :

-

CPC VOLUMES : CPC Volumes has been lower due to Slight Delays in Shipments And one of the Client having a “Force Majeure” - meaning Unexpected Unwanted Event or Issue, but have seen full shipping, into the 1st Qtr, and CPC is Witnessing Sustained Demand, leading to Improved CPC Performance in the Current Qtr.

-

Shipping/Cost Rise : Company by its experience is well hedged to face freight-shipping costs rise, by employing Large Vessels, with Higher Capacity and Increasing Volumes in these Ships, which will offset Cost Pressure.

-

MARGINS : Company is Guiding for maintaining margins seen in current Q4 Going into Q1 which is positive for current qtr going ahead. Even though Raw material Prices have risen, Company has intimated clients about the increase of its finished products, and confident of passing on the higher costs.

-

CHINA DEMAND & Scenerio Post Winter : There has been actual higher than larger closures than expected especially in the Calcine Side, compared with other Smelters, and Company sees tightness in CPC in China leading to prices of CPC continuing to be firm.

-

US CPC DEMAND ON EXPANSION BY ALUMINUM MAJORS GOING AHEAD : Fresh Demand of 250,000 TO 300,000T of CPC demand as Alcoa/Century Aluminum/Mangnitude Metals etc see expansion of Capacites in the the North American Zone, VERY POSITIVE for Rain from 12-24 Months perspective.

-

BENEFITS OF REFIANCING OF DEBT ON INTEREST COSTS : Company expects savings of around $25 Million to $30 Million, which could conservatively translate into 30 cr to 35 cr conservatively each qtr, taking into account current Debt levels, again positive for EBITDA/Net Profits, going into 2018.

-

COMPANY`s PRODUCTS/PRICES : Fuel Oils/Benzene/Napthalyene/BTX-PAN Witnessing Steady Higher Prices & Demand.

-

Tax Savings : The Fall in US Tax Rates from 35% TO 21%, and also fall in Tax Rates in Belgium from 34% TO 29% has already seen write back of Tax Provisions made, and Tax Provisions will see lower trends in 2018, which should boost the net levels.

-

IT INTEGRATION : Company is in final stages to allign all its operations gloabally, on the latest SAP Models, and this will aid for prevention of Fraud/Theft etc on the Digital Fronts.

-

CEMENT OPERATIONS : Demand was mixed in the current qtr, but currently Telangana/AP Seeing improved trends, and Karnataka seeing muted offtake. Company has faced cost pressure due to Increase in Disel prices, as most of transport is by Trucks. Company is focussing on cost savings measure to lower costs, from waste recovery/cooling systems etc and hopes for a better 2018 from the Cement vertical front.

-

ADR ISSUE : Company does not want to go in for a ADR Issue to repay debt, and will use Increasing cash flows to reduce debt, especially the Euro denominated Term Loan B of 390 Million Pounds.

-

Pension Liability : The Benchmark for calculating Pension Liability is the 10 Year German Bonds, and as per new accounting gain or loss will be directly accounted in the Balance Sheet.

-

Chemical Division : Company has seen slightly lower volumes due to lowering/discountinuing low margin Chemical Traded products, & minor fire which effected a chemical Units. However New value added products are on the anvil, and Company hopes to brief Investors in the next 2 qts about developments in the Chemcial space.

-

Duties on Imports into India : Import duties on most carbon products have been raised to 10% from 2.50% from Jan, and company is passing on the same.

-

Fixed Interest Debt : Most of Company`s debt is in the form of fixed rates and hence any rise in US Interest rates should not effect the Company going ahead.

Conclusion:

Management has Given out Positive guidance for 2018, and With firm trends in CPC/CPT both from demand and finished product views and Rain Industries should make good progress in 2018.

Lower Interest costs/Lower Tax rates - Provisions should be the next positive which will be added to Net Profits.

Company need to improve its Chemical/Cement Vertical wherby a strong boost to topline/EBITDA/Net Profits can be Seen for 2018.

Repayment of Euro Notes as Cash flows Increase will be crucial for lower debt levels, leading to further lower Interest Costs.

Also, Rain industries is strongly placed to report Net Profit in the range of 1150 cr to 1200 cr for 2018, and there is scope to beat this figure as well, paving way for robust EPS of over 35 and have a good scope for strong re-rating in the coming days ahead.

14 Likes

Hi Board members,

Have a question related to Account receivable from the presentation

AR:

CY17 CY16

16873 10392

This is close to 62% Y-OY increase in the AR.

During the same period the sales has increased as follows

CY17 CY16

113919 94378

This is close to 20% Y-O-Y

How should we interpret this, as I read in some of the fundamental analysis book that the increase in the AR should be proportionate to the sales.

Can someone throw some light on this.

Thanks,

Pandi

2 Likes

Thank you so much for taking your valuable time and posting your understanding of results and summary of con call. This is my reading from your replies: All in all the growth of Rain is well poised into 2018 with the tailwinds that are helping it to catapult into accelerated growth.