Radico Khaitan concal summary:

-

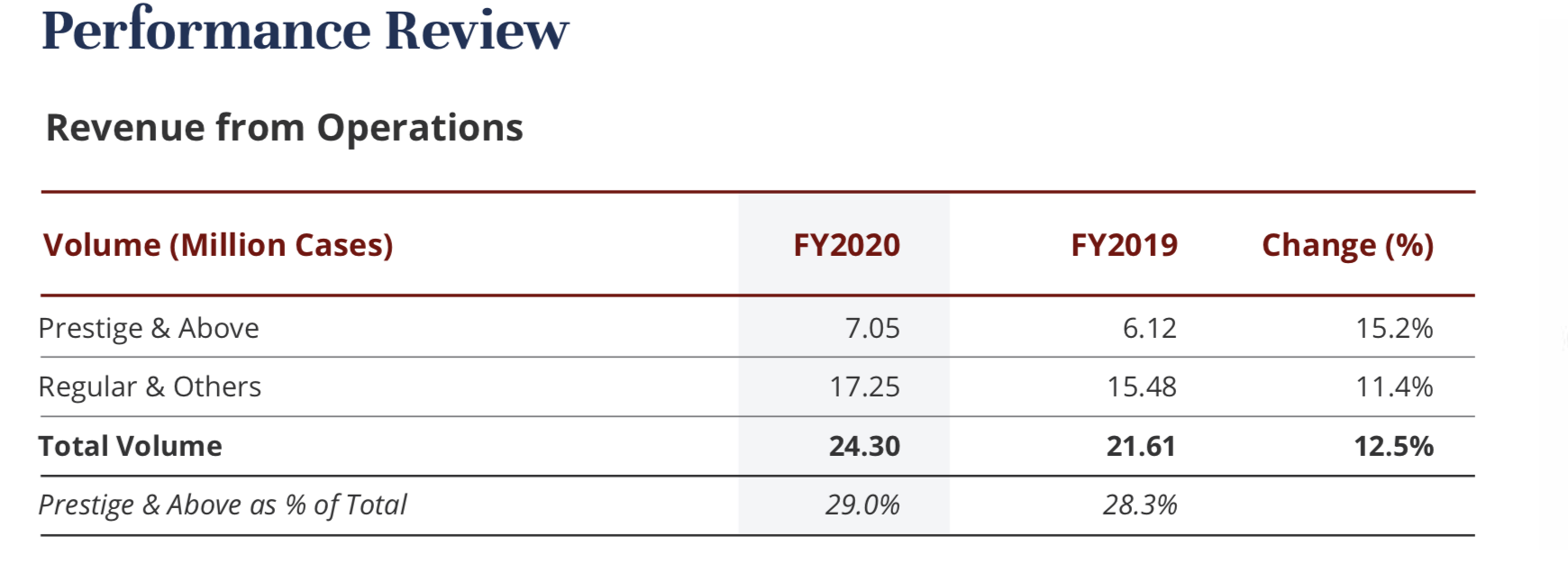

Outgrown industry volume growth, industry grown 0.5% vs radico grown 12.5% due to good brand portfolio

-

ENA price reduced 2% qoq but increased 19% yoy put pressure on 200bps gross margin impact. But improved monsoon, drastic reduction in crude price,good crop this price may come down going forward

-

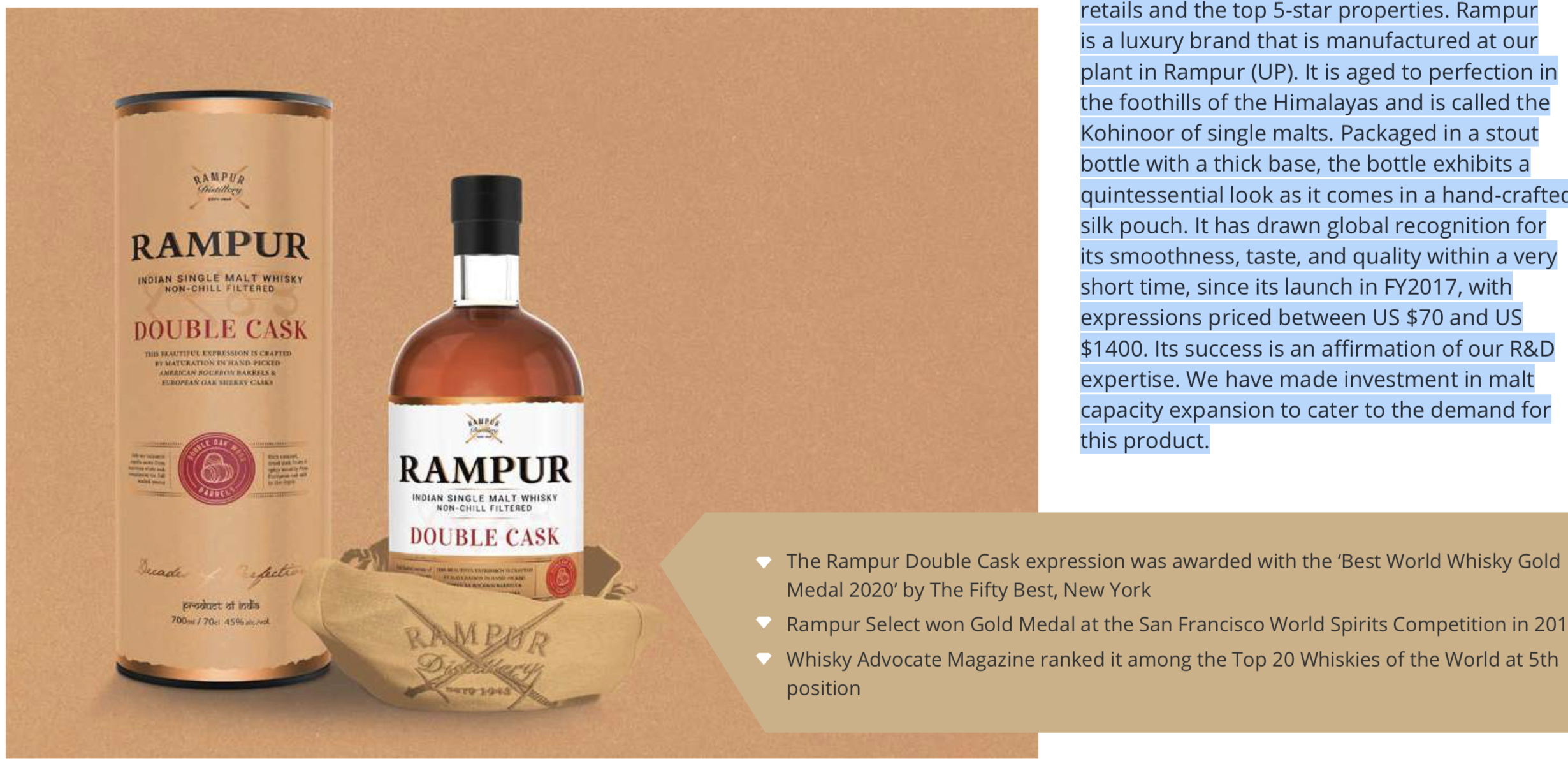

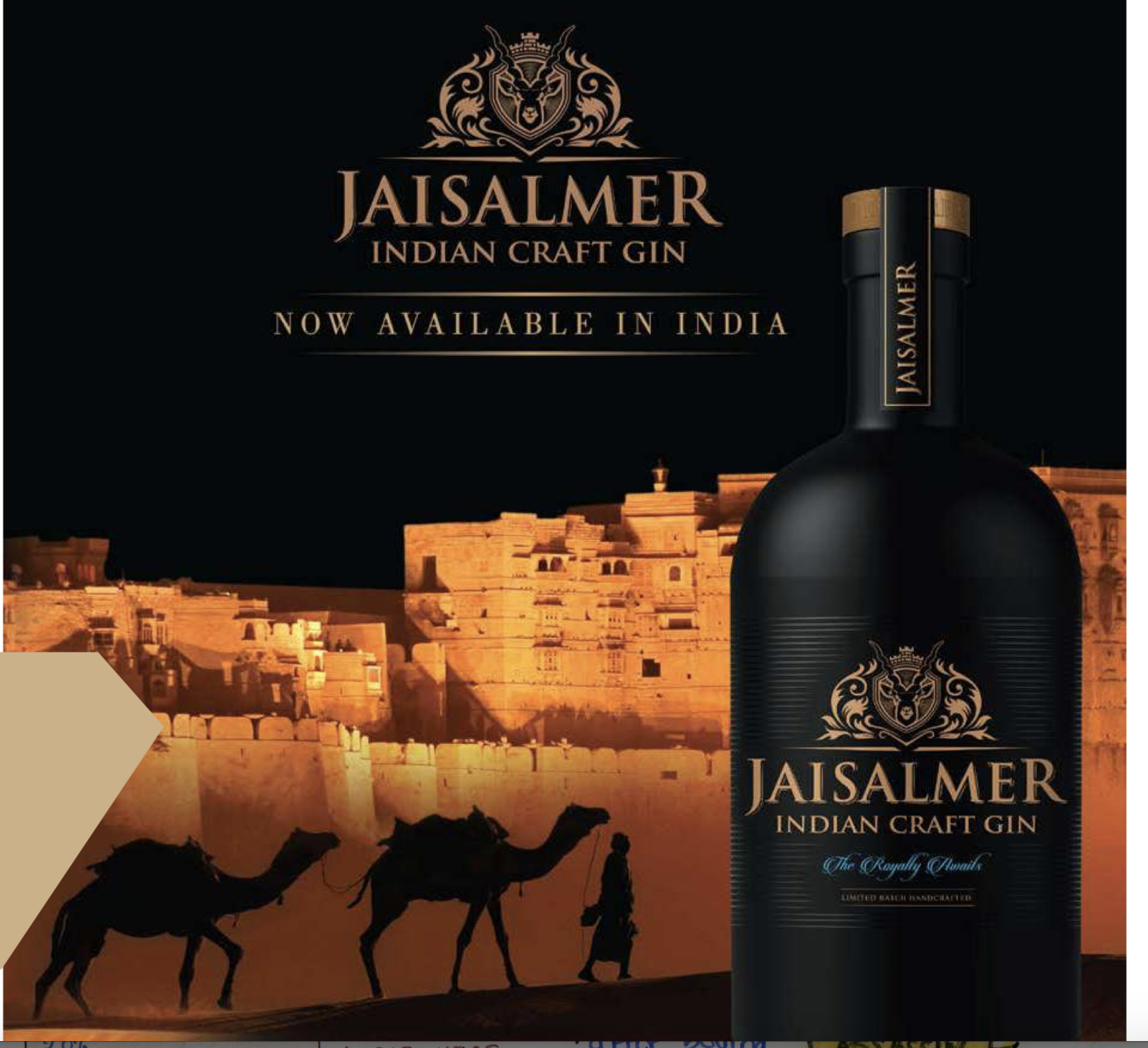

2 of premium brand crossed million cases this year

-

8 pm family volume crosses 10 million cases

-

Near term outlook remain uncertain but medium and long term trend intact

-

Finance cost reduction of 10.2% ,March year end debt of 382cr increase in debt due to increase in working capital

-

Year end receivables 300cr , due to timing delay in receiving receivables from corporation on the day of March 31. But company received major part of receivables within 45 days from the corporation. Received 100cr of receivables so they repaid the debt . Debt as of today reduced to 300 cr from 382cr

-

Other expenses due to cow cess imposed on UP

-

Alcohol delivery directly to home:

Delivering alcohol directly to home is good structural change, it gave one another distribution channel and so help to increase consumption. And this help people with hesistant and particularly women for alternate mode to consume alcohol -

Increase excise duty is 100% pass on to consumer and

MRP is adjusted accordingly so no pnl impact.

11.wherever 80-90% stores are open and states with excise duty increase of only 10-15% came back to normal -

States where 70% excise duty industry volume reduced by half,

-

States where 10-15% excise duty increase mgmt not seen any down trading happening but states where 70% excise duty increase seen lot of down trading. If this excise duty will not normalise in near future the material from neighbouring state will flow to this region will result in less revenue to state.

-

All 32 units of company get operationalized .and not seeing any issue to ramping up the production once the consumption become normal

-

Northern market has higher edt for premium brand compared to southern market

-

Annual realisation for premium product will be maintained at 1400 to 1450

17.AP contribute to 7% revenue so no material impact on ap excise duty raise

18.on closing of bars and restaurants:

In india only 3-4% only alcohol consumed there. Majority of alcohol consumption happened in house . So social distancing and closure of bar won’t affect much -

Receivables outlook:

As state financial under strain going forward , majority of state revenue depends on petrol and alcohol. So in order to increase revenue states increasing distribution routes to increase consumption . So they have to pay supplier properly in order to support this revenue to flow in . Otherwise this will affect states most . So going fwd mgmt not seeing any pbm with receivables -

Selling premium brand in mall is step in right direction , it will help to increase consumption and mgmt waiting for implementation

-

Telegana gave 8-10% price hike in this year. Tamilnadu gave 96 rupees per case price hike. Kerala too will increase price

22.new premium brand in whiskey going to lunch in next couple of month which is up scale of 8pm black variety. Company focusing on vodka and brandy upscale products too -

Gross margin of 48.5 to 49% and ebitda margin of 15% is guided

-

A&p spend around 7% last year it may come down this year

Regards,

Sathish