@varadharajanr who is this competitor? what’s the name of this company? thx

It must be Spica India if I am not wrong.

2Q results out. 14% YoY sales growth, 8% EBITDA growth and 23% PAT growth. 1HFY16 PAT growth at 34% YoY.

1 Like

Decent set of numbers… PAT growth came in higher because of higher contribution from other income. Is this other income related to fx ?

Any clue about Today’s closure of 20% upper circuit? Only justification for such rise could be from Vietnam capacity expansion/ announcement of new client addition comparable to Hanes in my opinion.

Discl: Invested and have purchased in last 6 months

1 Like

Today one of the private equity fund has recommended this stock. So this stock was zoomed to 20% circuit. This is my assumption.

Disc: not invested.

which pvt equity fund? or stock advisory service?

StockAxis recommended this yesterday

this advisory service has such big impact?think Vietnam plant has commissioned or current qtr perf is good

The company has started looking for executives for their vietnam plant: (LinkedIn screenshot)

Job requirements posted in Oct & Nov.

3 Likes

How is Premco placed technically n fundamentally ? What cud bethe impact of crude n commodity softening on it?

The Vietnam plant got commissioned on 15 Jan 2016.

Hi @Vivek_6954,

I don’t see any CA regarding commissioning of the vietnam plant. How did you get to know this?

I also read the commissioning of Vietnam plant news in moneycontrol messenger, where few people saying about this. Hope that news is correct. This is the original news last year : http://www.indian-commodity.com/corporate/premco-global-to-set-up-plant-in-vietnam.aspx

The all news will be disclosed soon. The result will be on 3rd Feb.

Let’s hope for 4.2-4.5 Cr PAT this time. Current valuation 18 pe looks fine for long term investment.

Disc : Invested 4-5% of folio

I am exploring Textile sectors, not invested as yet.

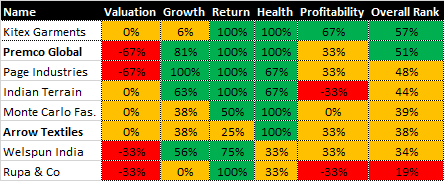

FA wise Premco is excellent. May be costly, but other peers are relatively cheap, but with their share of weakness in fundamentals.

May be Quality wise Premco is strong. Value wise Indian Terrain is attractive.

I think that we should not generalize the textile company’s same as pharma or fmcg company’s. (In pharma/fmcg, most of the company’s business model is same)

Here each company has different business model.

Like Arrow Textile, Premco are in B2B space but Premco targeting export customers where tailwind is very high and earning is in USD where Arrow targeting indian base company.So Premco’s valuation always be in higher side.

Page, Indian, Monte Carlo is in B2C business where Monte Carlo has seasonal business while Page has very strong track record vs Indian has poor track record in past. So valuation difference will be high.

Where welspun, Verdhman fall into typical textile business where equity capital & debt is very high. So all RoE, RoCE is poor compare to Page/Kit and hence it’s not make attractive opportunity for investor prospect.

Desc : Invested in Page, Kit, Premco

1 Like

Your textile business understanding seems good, and it matches with fundamentals & valuations. But the issue is 2 investors will have different opinion looking at the matrix. One who is already invested & other who is looking to invest.For an new entrant Its a typical case of paying up for quality or look for value.

Marginal decline in profit and sales for Premco. No update on Vietnam plant. Not so great result and may see temporary set back in prices in short term.

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=b0b40000-7fb5-49e1-a533-2f943961871a

The number looks ok. We can’t expect 30-40% sales and profit growth in each Qtr. Sometime business is in transition phase and Qtrly number muted.

The current valuation is 16 pe seems ok for long-term investor to buy at some lower level. Nifty Current P/E is 18 vs Premco you get in 15-16 pe so risk seems less.

Find enclosed link for Hanes Capacity in Vietnam

As per this article, Hanes has 400 million in Central Vietnam (Two factories) and Third one with 67 million pieces giving total capacity of 467 million.

Assuming, third unit being fully for undergarments and old capacities 50% being for activewear (not using Elastic), total capacity in Vietnam for innerwear would be 200 million in Central Vietnam and New capacity of 67 million piece in North Vietnam, giving total capacity of around 250 million.

Assuming one innetwear requiring 1 mts of elastic and 1 Mts elastic realisation costing around Rs 6-7 (10 cent at exchange rate of 67 INR/USD), total requirement of Elastic from Vietnam could be Rs 175 Cr (250 million* RS 7) or USD 26 million.

Very crude number crunching based on some subjective assumptions and may go completely wrong. But still give at least some guestimate of potential market for Premco Global Vietnam operation. Any thoughts:

Discl: Holding since last 12 months and added in last three months

2 Likes

Nice number crunching, Dhiraj!

Given that the Hanes new facility has started, shouldn’t the timeline have been same for Premco? It seems they are running behind. As per the latest note in the Dec quarter result they have invested about 3.95 Cr in the subsidiary till now and haven’t announced on commissioning of the same.

Regards,

Ayush

Disc: Invested