This is my first report to the forum… your feedbacks are welcome

I want to share about Precision Cam shaft Which can be on the verge of future disproportionate growth. My Background is mechanical engineer and Masters in business currently working in indirect taxation in government. My Humble request to moderators and seniors if same topic is covered elsewhere you are requested to move this to the requisite thread

Company Back Ground :

The Company was incorporated as ‘Precision Camshafts Private Limited’ on June 8, 1992 under the Companies Act, 1956 (“Companies Act 1956”), with the Registrar of Companies, Maharashtra at Mumbai. Pursuant to conversion of the Company into a public limited company, the name was changed to ‘Precision Camshafts Limited’ and a fresh certificate of incorporation consequent upon change of name on conversion to public limited company was issued by the Registrar of Companies, Maharashtra at Mumbai on August 1, 1997. Pursuant to a resolution of the board of directors of the Company dated January 10, 2001, the registered office of the Company was shifted from 51, Sarvodaya Housing Society, Hotgi Road, Solapur, 413 003, Maharashtra, India to E 102/103, MIDC, Akkalkot Road, Solapur 413 006, Maharashtra, India with effect from January 10, 2001 and the relevant filings were made by the Company with Registrar of Companies, Maharashtra at Pune

It was listed in the exchange on 08-Feb-2016 it’s Location is at : E 102/103, M I D C, Akkalkot Road, Solapur - 413006, Maharashtra, India and virtual address is at http://www.pclindia.in/

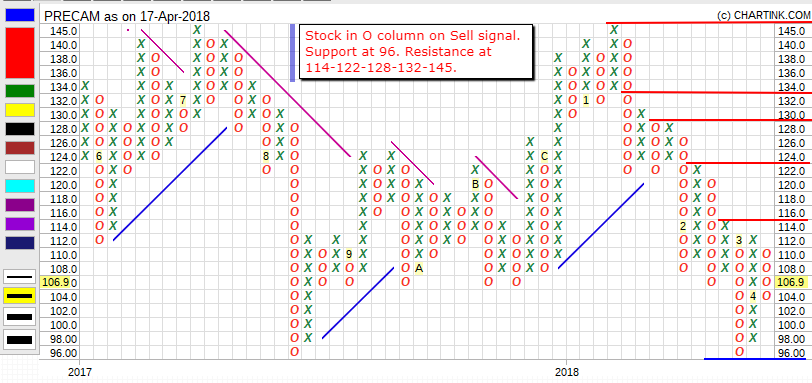

Fundamental

Industry Type : Engineering / Auto Ancillary Face Value:10 , CMP :110 , P/E ; 22

Manufacturing Facilities:

PCL has set up four manufacturing units at Solapur, Maharashtra out of which two units are 100% Export Oriented Units (EOU).

Weakness/Threats :

• Customer and product concentration Historically, PCL has been dependent on a single product, i.e. camshaft and limited number of customers for significant portion of its turnover. GM (as a group) and Ford Motors (as a group) are PCL’s primary customers, which together accounted for around ~69% of total income in FY16 across various geographies. PCL thus faces the risk of fluctuations in production levels of its key OEM customers.

• Susceptibility of profitability to exchange rate fluctuations PCL derives significant portion of its revenues (~75% and ~79% during FY16 and FY15 respectively) from exports, and its profitability is thus exposed to fluctuations in foreign exchange rates.

• Susceptibility to quality standards: PCL products are subject to strict quality requirements and any failure to comply with quality standards may lead to cancellation of existing and future orders

• Susceptibility of profitability to fluctuations in raw material prices PCL’s major raw materials include resin coated sand, melting steel (M.S) scrap and pig iron. PCL primarily procures them from domestic markets from reputed manufactures. The volatility in commodity prices can significantly affect PCL’s raw material costs and in turn, profitability. Inability to compensate for or pass on increased costs to customers, such price increases could have a material adverse impact on PCL’s financial profile. PCL does not have do not have long term agreements from its suppliers However company is sourcing these from multiple vendors

• Cyclical nature of auto industry The auto components industry is ancillary to the automobile industry. Demand swings in any of the auto segments have an impact on the auto ancillary demand. The demand scenario is impacted by general economic or industry conditions, including seasonal trends in the automobile manufacturing sector, volatile fuel prices, rising employee expenses and challenges in maintaining amicable labour relations as well as evolving regulatory requirements, government initiatives, trade agreements and other factors

• Labour problems: in past in 2013-14 company has faced problems from labour unions but now PCL have hired third part unskilled workers from the contractors

Rationale of investment / Strengths

PCL’s established track record of manufacturing of camshafts, long-standing relationship with globally reputed client base, wide and diversified geographic presence and PCL’s strategic and technology tie-ups with world’s leading camshafts manufacturers and ongoing capital expenditure (capex) without much reliance on debt.

Long track record and experienced top management PCL has a long track record of about 25 years in manufacturing of critical engine components and has established strong business relationships with global OEMs. The promoter, Mr Yatin Shah (Managing Director (MD), a first-generation entrepreneur, has a vast experience in the field of engineering and has grown the organization over the years into one of the leading manufacturers of camshafts in India. The promoters of the company are assisted by a qualified and experienced management team which has been associated with PCL for more than 15 years.

Long association with leading global and domestic OEMs with wide geographic reach PCL has developed strong long-term relationships of more than a decade with large OEMs, both within domestic and international markets. Total client base exceeds 40 leading OEMs, and includes reputed names such as General Motors, Tata Motors Limited, Ford Motors, Hyundai, Maruti Suzuki India Limited, Chevrolet Sales India Private Limited, Mahindra& Mahindra Limited, New Holland Fiat India Private Limited, etc. PCL is the preferred supplier of camshafts to General Motors Company Inc. (GM) and Ford Motor Company worldwide. PCL exports camshafts to various global OEMs covering Europe, UK, China, Brazil, Russia and North America. PCL has been constantly expanding its geographic presence and has been increasing the market share at a global level. Exports form a major portion of the total sales and accounted for ~75% of the total sales in FY16. PCL has tie ups with various international marketing agencies. In order to strengthen the business operations in Asia, the Company has promoted two joint ventures in China.

Highly advanced manufacturing facilities, technical collaborations with overseas players PCL has developed strong quality systems and its facilities are certified with ISO TS 16949:2009, ISO 14001:2009 and ISO18001:2007. PCL has also entered into an exclusive agreement with EMAG, a German machining and tooling process company, for transfer of certain know-how and technology for manufacturing assembled camshafts. The technical collaboration with the European and Chinese players has enabled PCL implement advanced machinery which aids in lowering the cost per piece.

Improvement in capital structure and debt coverage indicators, improvement in profitability and strong liquidity position During FY16, the capital structure of the company improved with overall gearing of 0.33x as on March 31, 2016, as compared with 0.83x as on March 31, 2015. Total Debt to GCA (TDGCA) ratio improved to 1.87x during FY16 while Interest coverage remained high at 15.69x during FY16. PCL’s liquidity position improved on the back of proceeds received from the IPO. Current ratio as on March 31, 2016, improved to 2.49x as compared with 1.21x as on March 31, 2015. PCL had a free cash balance of Rs.312.46 crore as on March 31, 2016 (Rs.88.93 crore as on March 31, 2015). Since the capex in near future will be funded using the IPO proceeds, internal accruals will be available for managing the working capital. Furthermore, on January 13, 2017, Rs.62 crore of preference shares held by PCL in CTPL have been fully redeemed, improving PCL’s liquidity profile significantly. During 9MFY17 (unaudited) (refers to the period April 1 to December 31), PCL’s revenue remained flat with TOI of Rs.345.57 crore as compared with TOI of Rs.344.45 crore during 9MFY16. Its PBILDT margin declined to 23.64% for 9MFY17 as compared with 26.29% during 9MFY16 mainly due to higher employee cost. The company reported Profit After Tax (PAT) of Rs.45.24 crore during 9MFY17 as compared with PAT of Rs.48.21 crore during 9MFY16

High Barrier to Entry : Only 5 to 6 major player in the market Business is Oligopolistic in nature however ThyseenKupp who is European pioneer in this field is struggling in Latin American market

Revised Credit rating on dated 24/04/2017 company got revised credit rating from CARE Long-term Bank Facilities : Revised from CARE A- [Single A Minus } to CARE A; Stable [Single A; Outlook: Stable] and Long-term/ Shortterm Bank Facilities : Revised from CARE A-/ CARE A2 [Single A Minus/A Two to CARE A; Stable / CARE A1 [Single A; Outlook: Stable/ A One

Detailed rating report : http://www.careratings.com/upload/CompanyFiles/PR/Precision%20Camshafts%20Limited-04-24-2017.pdf

Recent Order: PCL has won a global contract from Ford for the delivery of 8 million camshafts over the life of the program, which is expected to commence supplies from 2018-19

Margin of Safety: IPO price – CMP i.e 180 – 110 =70 which comes out to be (70/180) *100= 38%

Shifting focus from low value product to high value product: Cam shaft casting profit 15- 18 % whereas machined cam shaft offer 30-35% profit which is elaborated by R&D innovation, Capacity Expansion and acquisition, technology collaboration

PCL, which is a leader (40% stack in global market )in chilled cast iron camshafts, is taking steps to climb the technology curve. In 2014 y, it introduced ‘Ductile Iron Induction Hardened’ camshafts (aims from 20% share in global market ) to its portfolio. It has also struck a technical alliance with EMAG of Germany deal was signed in the month of June 2014 beweeen Yatin Shah, CMD, Precision Camshafts, and Dr Andreas Mootz, MD, EMAG Automation, which will help it enter the assembled camshaft market. The pact includes the development of a low-cost version of the technology. PCL will hold a global patent for it for the next five years i.e till 2019 (ref : http://www.autocarpro.in/news-national/precision-camshafts-inks-tech-pact-emag-ag-aims-stop-global-shop-5861)

PCL recently entered into two joint ventures, both with Ningbo Shenglong Powertrain Company Limited (―NSPCL‖), being Ningbo Shenglong PCL Camshafts Company Limited (―NSPCCL‖) for machining of camshafts and PCL Shenglong (Huzhou) Specialized Casting Company Limited (“PSSCCL‖) for setting up a foundry in China

To increase its capacity at the Solapur plant, the company has added a machine shop with proposed capacity of 2 million units annually with a total capex of Rs 230 crore. The capacity addition will be in phases over FY18 subject to the order received from customers. The company says this new capacity addition will expand its product offerings for existing customers as well as target new customers. PCL is also setting up a plant in Brazil for machining of camshafts to General Motors. The GM order includes 6 million units over the life of the programme

Recent acquisition of MEMCO Engineering: The company is Nashik-based precision machining it is a supplier to German component maker Bosch. It is 32 year old company with equipped with a range of CNC turning, VMCs, Deep hole drill machines, Multi-Spindle Automatic lathe, along with other Second operation conventional machines

Copy of original IPO : http://www.sebi.gov.in/sebi_data/attachdocs/1426145620337.pdf

Discl: Currently invested about 5% of my portfolio so views maybe biased do you own research before investing. Inviting reviews and guidance from forum and seniors .Contradicting or questioning is highly appreciated and looking forward for a discussion …