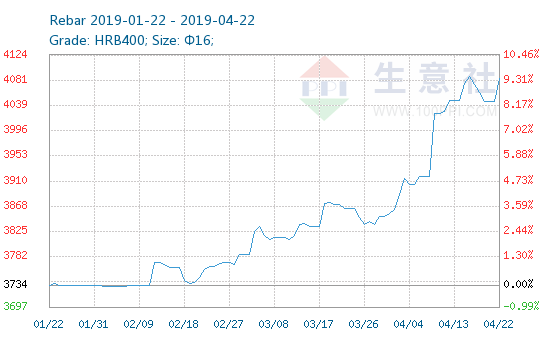

Rebar prices are moving up recently as shown in graph (source: SunSirs).

More Importantly, PLEDGING has gone down considerably

Pledging as % of Promoter’s holding:

June 2018 - 77.29%

Sep 2018 - 62.63%

Dec 2018 - 64.62%

Mar 2019 - 52.65%

Now, Prakash will trade Ex pipe division tomorrow. Prakash pipes value unlocking is possible (opposite is equally true given the history of stocks like Omkar, sintex, etc.)

As per the steel prices and demand, good results are expected. I think people are pricing in Peak of profit cycle. This, I believe, is good thing as a bad scenario is already priced in.

I believe that it is waiting for a bull run in market, then only it’ll run. If sentiments change, it can show good runup. This makes it a good stock to look at from 2-3 years perspective. The risk that I see that can tank the stock is if numbers are fake. If anyone sees other negatives that makes stock expensive at current valuation, views are invited.

Prakash Pipes shares may be allotted much earlier and credited to demat with temporary ISIN but listing of same will take about 45-60 days in normal course.

Based on your rich experience in markets, what would you suggest on working around these spinoff’s. Should we hold the parent and child companies/ sell ? There have some spinoffs happening in Prakash, Man inds etc

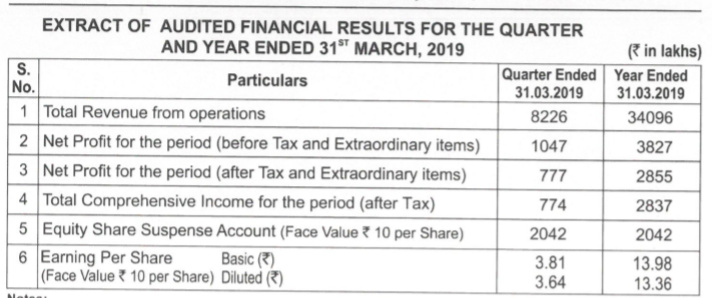

Starting the journey with a Dividend! The first filing of Prakash Pipes post demerger is out. The results are announced and dividend is pending now. This is certainly a nice way by promoters to communicate that they are ready to share the profits with shareholders. Fingers crossed for the new journey!

Is the yearly EPS around 13 for PPL? With this sort of EPS what sort of valuation we can expect the listing at given the valuation of similar other companies.

board to consider dividend along with q4 results. A big positive for this company and a welcome change from the regular practice of not giving dividends.

PIL has declared a very good results and dividend.

But if some seniors could kindly explain the rationale of the exceptional expense and it being debited from the general reserve it will be highly helpful

Though the nos look good on face of reported earnings but big write offs from reserve create lots of question mark on the promoter and balance sheet etc. Based on what I could understand - the write off is of a power project started several years ago but stopped due to unfavorable policy/changes. This used to be shown as CWIP on balance sheet for last few years and finally it has been written off. So this is a non-cash charge.

Similar thing has happened in the reported nos of JSPL also.

Have they shelved out power Project ?? But we can still find substantial amount of CWIP in the books.

One benefit of write off can be that they can save tax on this, my interpretation : write off is a non cash expense, but with Income Tax @ 30% the company will be saving cash out flow of around Rs 120 Cr.

In there results they have announced that they have received all the approvals

The Company’s captive Iron Ore Mine in Odisha has now largely received all statutory approvals and the Company is making all out efforts to operationalize the same very soon.

This has been heard for long time and I hope they get it done otherwise a good chance will be missed by promoter.