https://www.steelmint.com/billet-prices-indian

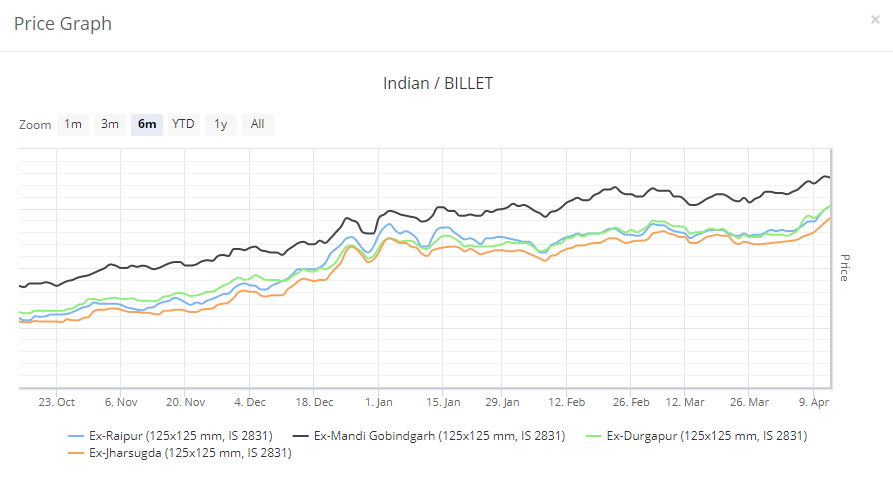

Above are the price graphs of steel billets in different parts of India

There is rise in Indian Steel Billet prices recently due to e-Way bills due to restriction on movement of unaccounted materials. Shown in the above charts from steelmint

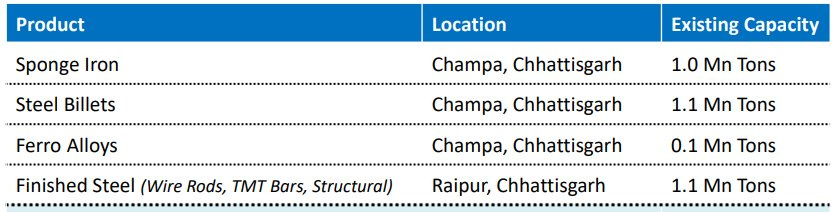

Below is Prakash product profile

It is apparent that Steel Prices are on a increasing trend are at all time high. This augurs well for Prakash Industries.

I am expecting announcement regarding Commissioning of Iron Ore Mines very soon. Although the company had been assuring its commissioning since 2010 (as per various old brokerage reports). But lets see, if it is announced it will be a big positive (long awaited) for the company.

Thanks Maven for sharing the Price Graph.

The following news shows that there is a clear cyclical uptrend in Steel Industry and more particularly in Indian Steel Industry. The way top corporate steel giants are showing their interest it is very much evident that the uptrend industry in Indian steel is going to stay for a longer period of time( minimum 2 to 3 years)…

Liberty House Offers Over Rs 26,000 Crore For Bhushan Power And Steel

The following are the reason for revival in steel Industry:

It is really ironical that India is increasing its steel capacity and China is cutting down…

Dear @VALUE2017,

Many thanks for sharing the articles. As you rightly mentioned steel is in an up cycle. There’s abundant information to testify to that effect.

Is it likely that the upcycle is already priced in?

The stock has risen by more than 500% in the past 22 months.

Dear Shreys do not go by percentage increase in the stock price from its past levels because one can then probably argue that the stock price was at 347 on 01/01/2008 and around 230 in March 2010 and that the stock price has not increased during the last 8 to 10 years. The main idea of value investing is that whether I am getting a value at this price and if the answer is yes go ahead and buy and it it is no then wait for the correction.

While arriving at value, apart from present valuation you will also have to necessarily factor future growth prospects.

Conclusion of above my above two posts: The Indian Steel companies have clearly understood that at the current rate of growth of India, there will be a growth of 7 to 8% in steel demand i.e around 7 to 8 MT. In the near future the demand is going to outpace supply and hence all steel companies are either on a expansion mode or buying out stressed assets to cater to the rising steel demand.

India is the second largest steel producer in the world and the supply is just enough or short of demand. The second largest Steel producer i.e China is on a production cut on a large scale (the production cut by China is more then the total production capacity of India). Also the Chinese are no more interested in producing cheap and low quality Steels mainly due to alarming pollution levels.

So we are having a rising demand scenario with domestic supply shortage and also the threat of import of cheap steel from China is not visible in near future. All this things place Indian Steel Industry in a very sweet spot and this the reason why there is so much of interest in stressed assets and capacity expansion by Steel companies

withdrawn…

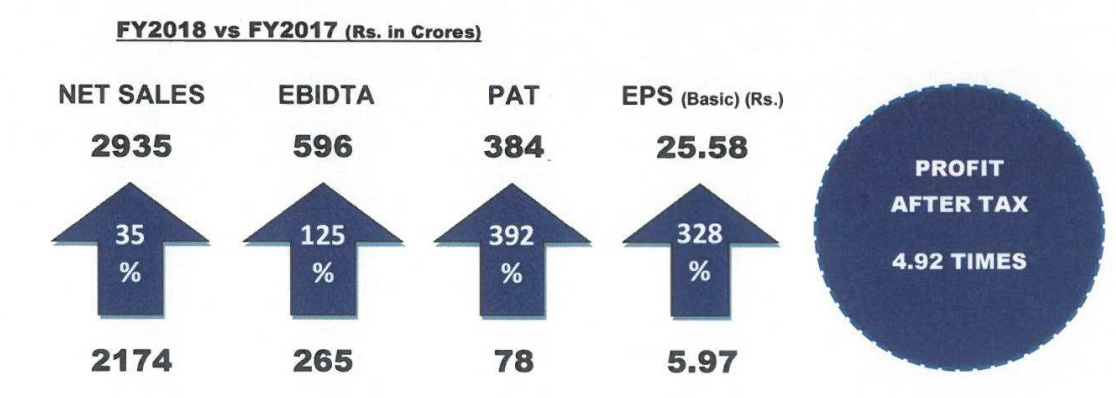

Pretty good performance. Sales up 45% and PAT up 347%. Yearly EPS now at Rs.25.58 which means that at Rs.216, it is trading at a P/E of around 8!

Year at a glance.

P/E of 8 could indicate that earnings have peaked out…

Disc: Holding

Hi @aammiitt2 @VALUE2017 @phreakv6

From the cyclical nature of the industry what I have understood from the commodity thread in VP is that we need to exit when the they are at peak earnings, but going by the thread it looks like there is still or rather more steam left, can you help me which of the understanding is correct, excuse me for my novice question.

my point is regarding the pe…Low pe is not a good measure in commodities…Look at price realisation and margins…As long as the price is stable for steel the stock would go up…Backward integration is favourable for prakash as it keeps them insulated from price increase in iron ore…investors who are disappointed by no dividend announcement should note that they have not been distributing dividends since 2014…This is the time to trim down the debt and add more capacity incrementally using internal accurals…

I am holding it for now…

No buy/sell recomm.

Though overall Q4 results are spectacular, Power segment contribution is more in terms of EBIDTA, when compared to steel segment. Again steel segment EBIDTA is less on Q-O-Q basis even though billet prices have firmed up during the last Qtr (Q4). Perhaps this might be below market expectation and short term punters have booked profits.

Discl: P I forms 7% of my PF and intend to hold as long as Steel cycle is in uptrend

Prakash QoQ margins of steel is gone down.

In last quarter it has done 652 crores of sales and NP of 28.39 crores NPM: 4.3%

In this quarter it has done 836 crores of sales and NP of 22.22 crores NPM: 2.6%

This is despite the rise of end product prices which is not understandable. Hence prices have cooled down as RoA is low for steel.

Bulk of the profit is from Power segment.

Management has guided for 40% revenue growth and some improvement in margins.

Billets price have risen recently, but rebars have been rising in last quarter.

Nothing announced on the start of mine which was expected by April 2018

In my opinion the inter sentimental reporting between Steel Segment and Power Segment are being done to take care of the Tax outgo and do not have actual impact on the performance of the company. The EBIDTA margin for the current quarter is 23% which is very good and also a significant improvement as compared to previous quarters.

The stock took a beating due to the misinterpretation of qualifying remarks made by the Auditors regarding the adjustment of MAT credit.

ya…the power & steel nos clearly looks adjusted as Rs 148 cr profit on Rs 173 cr revenue on power looks quite stretched…

need to watch stock price movement for the next few days to get a feel of where it’s headed…

surprisingly, couldn’t find any analysis of the results anywhere on internet…

not sure if something’s again cooking in this firm with tainted history…

discl: invested

In my opinion the results have met my expectation by all standards and I give a thumbs up for the following reason.

The cash flow from operations during the FY 2017-18 was a healthy 552 Cr.

The company has done a capital expenditure of around Rs 450 Cr and at the same time has also reduced total debt to the tune of Rs 112 Cr.

The long term borrowing has been reduced and in spite of 35 % increase in sales the Short term working capital borrowing has reduced by more then 40%.

Around 450 Cr of Capital Work in progress has been commissioned and will add to the top line in the current FY.

Along with this around 690 Cr of CPIW will be commissioned in the current Financial year and will add to the topline and bottom line performance of the company.

Analysing further and will update in this forum.

Disclosure : Invested and forms major part of my investment and hence heavily biased on positive side.

Now with regard to the qualifying remarks of Auditors on MAT credit.

The company is having MAT credit in the form of "OTHER NON CURRENT ASSETS " in the Asset side of Balance sheet. The outstanding MAT credit as on 31/03/2017 was 240.86 Cr. Now MAT credit is Minimum Alternate Tax which is a form of surplus Tax paid by the company and this surplus tax paid has be appropriated with in a period of 10 years. As the company was not able to utilise the same total tax credit of around Rs 76.72 Cr have expired during the current financial year. The company has however utilised MAT credit to the tune of 82.72 Cr in the current financial year.

Now the MAT credit which has not been utilised needs to be written off which is very much obvious. Since the MAT credit writing off is not a part of operations it is not required to be routed through the Profit and Loss Statement and has been directly written off from Balance Sheet from the retained earnings. The writing off is very much as per accounting norms , however I think it is very much prudent on the part of the Auditors to mention the same as qualifying remarks because the investors otherwise would not have noticed the reduction in retained earnings.

The qualifying remarks are not new and the same can also be found out in previous years Annual Report. I had already clarified this thing in my previous posts(in this forum) also.

I request other members to post contrarian views so that we can have both pros and cons of the company