Could this news impact Poly Med ?

Hi Raj,

Nothing can be said until the details come out. For example, if the products under such a regulation are stents, implants etc, there will be no effect on polymed.

IMO, the product portfolio of polymed should not be impacted.

1 Like

Forgetting the minutae, if this is to incentivise local manufacturers, it could only help Polymedicure expand in India.

In fact, Polymedicure stands a chance to launch new products also.

Poly Medicure Ltd has informed BSE that CRISIL has reviewed the Credit

rating of the Company and has Re-affirmed, the ratings on the bank

facilities of the Company as under :

-

Long-Term Rating : CRISIL A+/ Stable (Re-affirmed)

-

Short Term Rating : CRISIL A1 (Re-affirmed).

http://www.crisil.com/Ratings/RatingList/RatingDocs/Poly_Medicure_Limited_July_03_2015_RR.html

CRISIL believes that the Poly Med group’s business risk profile will remain strong over the medium term, supported by its established market position in the medical devices industry, increasing production capacities, and continuous focus on upgrade and automation of machinery, and on new product development, leading to sustained healthy

profitability. The outlook may be revised to ‘Positive’ if the group significantly diversifies its product profile leading to lower dependence on intravenous (IV) cannula and related products, thereby registering substantial growth, while sustaining its healthy operating profitability and capital structure. Conversely, the outlook may be revised to ‘Negative’ if the group’s net cash accruals are low because of a decline in its profitability on account of significant fluctuations in forex rates or increase in raw material prices, or if its capital structure weakens, most likely because of large debt-funded capital expenditure or higher working capital requirements.

1 Like

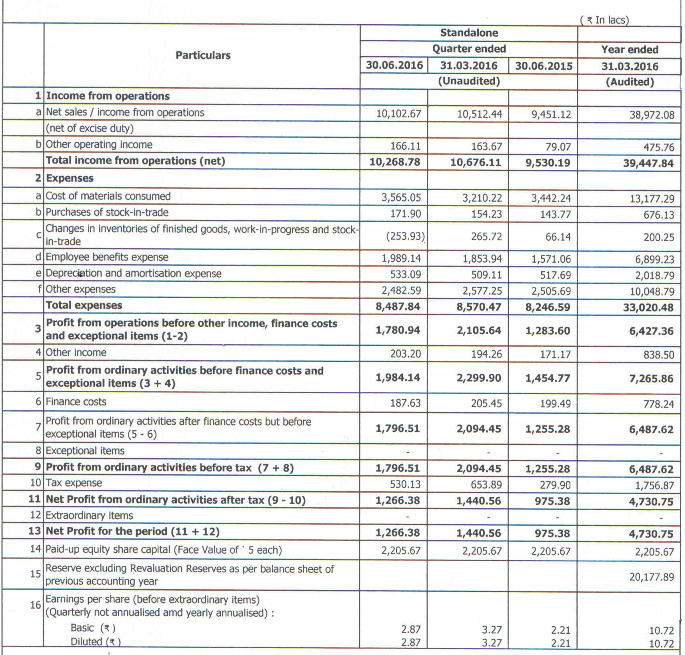

Results out

Sales up 16% to 94.5cr.

Profits flat at 9.75cr on account of 24% increase in cost of raw materials (34.4cr vs 27.5cr) and other expenses(25cr vs 20.4cr).

Sales flat for the last four qtrs. Profit flat for the last 8 qtrs. If we go by past pattern, they have to show growth in Sep 15 qtr. I think competition is telling on the margins.

However, there is a long ramp for Poly Medicure to grow at 20-25% CAGR. Medical disposable business is an evergreen huge business (unless, there is suddenly a replacement of IV Cannuale with some other tech.) And FY18-19, Poly Med can start selling Safety IV Cannuale anywhere in the world (Braun’s patent expires). Safety IV cannuale is 3-4 times more expensive than IV Cannuale. Think about the impact on revenues and margins.

Has he considered Braun’s Indian strategy to counter Polymedicure? When there is no price difference, guys will prefer Braun over Polymed.

Poly Medicure Ltd has informed BSE that the Company has received “GOLD” Patent Award for financial year 2014-15 on September 23, 2015 in recognition of commendable contribution in Medical Devices from Pharmaceuticals Export Promotion Council of India (Set up by Ministry of Commerce & Industry, Govt. of India).

The Company has also received ''First Position" Export Award for financial year 2013-14 and 2014-15 on September 25, 2015 in the category of Plastic Medical Disposables from The Plastic Export Promotion Council (Sponsored by the Department of Commerce, Govt. of India).

glad i exited this one. dug deeper after investing and the political links made me uncomfortable. too many lucky exits in my portfolio to make me uncomfortable - Poly, TRF, TIL, Vulcan.

memo to myself: 1. even small holdings for “watching” the stock can be dangerous. 2. must stick to the gems I hold

This is an old report, but the reason I have put it here is that the company Allegeny Finance was raided by the ED day before in connection with Robert Vadra.

Also, the fact that there are some companies which are clearly related to the promoters but not listed as promoters or acting in concert must be seen as a serious corporate governance issue.

3 Likes

I hope you have read my posts about the Company despite people arguing with me I was not convinced. I hope these guys exited at the right price. Only good companies, we can be passive as Fischer says but not with these kind of companies where we need to re visit our conviction often.

Unfortunately, couldn’t find any reasons why the stock has touched upper circuit today! Any pointers here?

It is trading at 52 week low without any change in fundamentals and sustainable business model … As new to investing especially valuation part Can’t understand whether it is wait or buy or screaming buy at this time . Any vp member would like to guide me on that ??

@DEEPAK_AGARWAL Although the long term story still holds, the company is unable to grow its sales and profits in last few Qs and the price is just reflecting that. Also, there are other better opportunities now in the market.

Interesting piece of blog questioning management’s integrity.

4 Likes

@Donald @ayushmit Your views about the concerns pointed by @goyal_neelesh will be helpful and a learning experience for us

Regards

Mallikarjun

1 Like

Hi Mallikarjun,

I have high regards for the business quality of Polymed - I think there wouldn’t be much debate that the business quality is high here…its a knowledge based business (there is intellectual property and innovation involved in terms of product and designs) and this company has done an extra-ordinary job of starting the business from scratch and becoming the biggest producer from India in a period of 15 years. Now coming to management quality - again I have high respect for Baids…they have worked hard to bring the business to this level and I feel they have been honest to minority shareholders. Had that not been the case, one wouldn’t have seen such healthy margins and wealth creation.

Regarding the specific negatives - I don’t have sufficient details to comment or make sure comments but my feel is that these are not material negatives to be deal breakers.1 - Transactions with Vitromed - the company has been mentioning about this in the annual reports since last 2-3 years and has taken shareholder approvals. I think the job work is for the safety cannula for which they want to protect their IP. 2. Starting of organic juices company - I don’t think the company would be big enough to be concerned. But yes, one should be aware of these things and try to seek answers. Another good thing would be to check the financials of these companies.

Regards,

Ayush

6 Likes

Poly Medicure to invest ₹60 cr in new facility in Haryana

http://www.thehindubusinessline.com/companies/poly-medicure-to-invest-60-cr-in-new-facility-in-haryana/article8807875.ece

1 Like

Steady results from Ply Med - 30% growth in PAT.

4 Likes

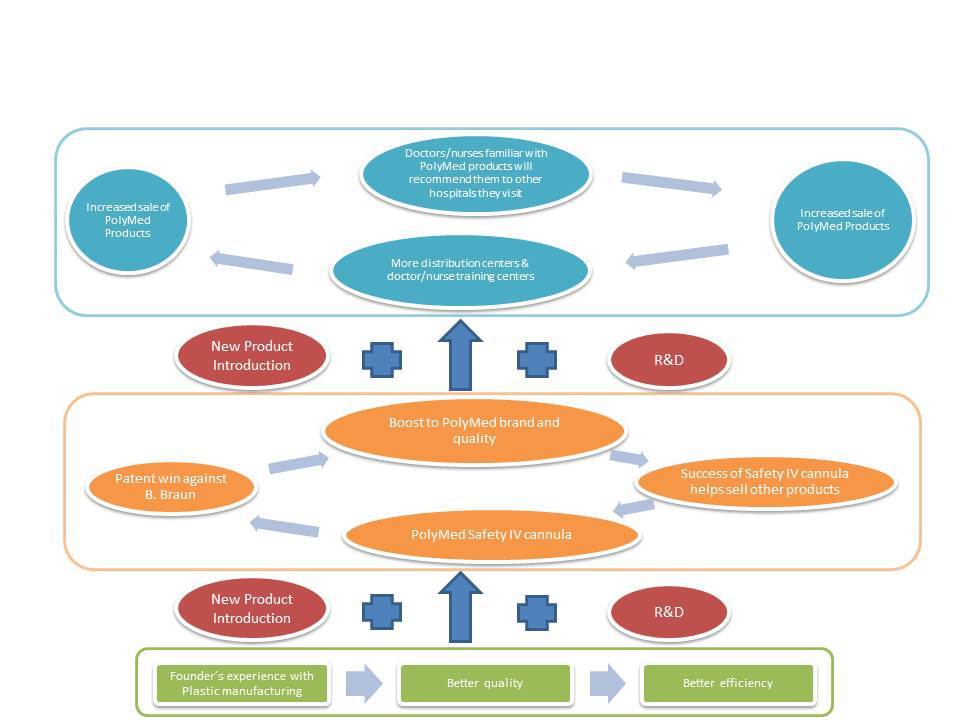

Inspired by the self-reinforcing business model thread discussion by @Donald Sir, I have tried to put PolyMed story in a simplified way. May be its too simplistic. I would appreciate if you can provide constructive suggestions to plug the holes in my understanding.

Phase 1: The founder had extensive experience with plastic manufacturing and hence decided to venture into the medical devices. Past experience with plastic manufacturing helped them to achieve better quality and better efficiency. Manufacturing is the core strength.

Phase 2: Safety IV Cannula is the main product with the company having IP. Successfully defending the IP against B. Braun (competitor) strengthened the image of the company in terms of quality and innovation. This in turn helps the company sell their other products. And as more and more customers use their products, it reinforces the quality/innovation of PolyMed which in turn helps them sell more products. So safety IV cannula is like a central product that is helping the company drive sales of their other products. The IP win against B. Braun has had a significant impact in establishing PolyMed’s quality and innovation.

Phase 3: Recently PolyMed’s focus has been to capture and strengthen its position in the domestic market and to this end they have been aggressively increasing their distirbution, sales and marketing network. PolyMed has been conducting seminars to train doctors/nurses on the use of their products. Once the doctors and nurses are trained to use PolyMed products and if they like them, the same doctors and nurses will demand/prefer PolyMed products when they go to other hospitals/medical facilities. So this in a way can be a self-reinforcing model.

Next Triggers:

1.New green field project at IMT Faridabad in Haryana (Rs. 60 Cr. investment) & introducing DEHP-free and PVC-free products to its range as these are considered environment-friendly and free of carcinogens.

2.FY18-19, Poly Med can start selling Safety IV Cannula anywhere in the world (B. Braun’s patent expires). Safety IV cannula is 3-4 times more expensive than IV Cannula. Think about the impact on revenues and margins.

3.Constant introduction of new products to plug the gaps.

Best Regards,

Lav

14 Likes

NOTES FROM AR2016

-

Revenue was 402.86 cr vs 381.9 cr in FY15

-

Net profit was 47.30 cr vs 61.01 cr (including 19.57 cr of exceptional items) in FY15

-

EPS was 10.72 vs 13.83 in FY15

-

PML is starting a new R&D center with an investment of 12.5cr which is to be operational by Q3 2016

-

New green field project at IMT Faridabad which is to be operational by Q3 2017 on an investment of 60cr

-

PML to focus on new market opportunities in Oncology, Nephrology & Respiratory Care segments

-

Product expansion is in process for Infusion therapy and Blood Management

-

PML is planning to launch 8-10 new products in FY17

-

PML is now exporting products to 95 countries

-

PML is now present in 3000 key hospitals in India and plans to expand to 5000 hospitals in next 2 years

-

Expanded the sales and marketing team with 80 new team members

-

The Indian medical device market is the top 20 in the world and 4th in Asia after Japan, China & South Korea

-

The medical devide sector was valued at USD 6.3 in 2013 and is expected to grow to USD25-30 by 2025

-

PML is the leading exporter of infusion therapy, blood management, gastroenterology, surgery and wound drainage,

anesthesia and urology products -

Over 65% of revenues come from exports

-

PML has 144 product and process patents globally; filed for additional 394 patents in India and worlwide

10 Likes