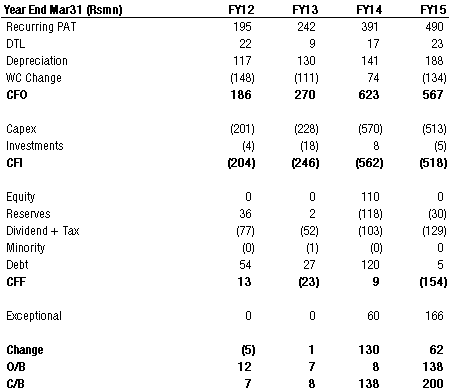

Please see attached cash flow statement below. Company spends as much on capex as it generates in terms of cash flows from operations. Yes I have excluded exceptional items 9crs and 19crs net of tax for FY14 and FY15. Debt/ Equity is very manageable at 0.31x and net debt to equity is 0.21x. Yes stock is not cheap.

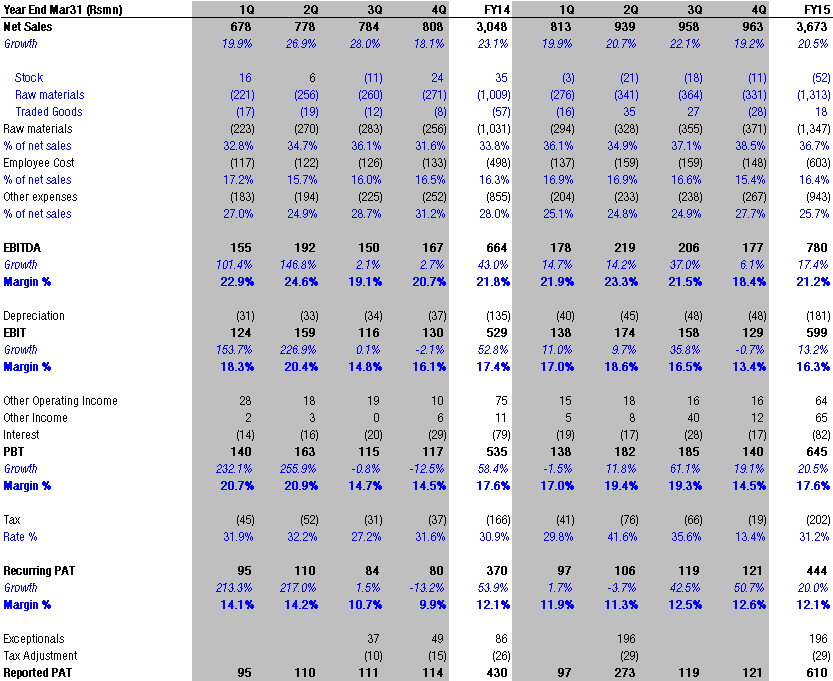

4Q results

-----19% YoY sales growth

----- 6% YoY EBITDA growth

-----19% YoY PBT growth on lower interest cost

-----51% Recurring PAT growth on lower effective tax rate.

FY15 consolidated EPS Rs13.3 up 20% YoY

RoE - 29% and pre tax RoCE - 27%

Please go to Page no 85 of AR 14 Always look at a business from a consolidated angle and yu again work hard to get the right numbers dont depend on publications like capital market as quality is compromised.

CF from operating activities Rs 65.54 cr

less exceptional item Rs 9.91 cr

Rs 55.63 cr Capex Rs 58.52 cr It is the same scene for FY 15 with around 19 cr as exceptional item but I can do this exercise correctly only when the AR 15 is out. But , going by the numbers it looks negative for me to be confirmed by AR.

A great business pays for Capex itself . Yu should be aware who said this. They are raising Rs 200 crs and it can be a debt or equity dilution. Both are bad from equity investors point of view . I am not saying there is something serious but we need to be cautious. We are getting into a stage where the earning capacity of the business is questioned and it is always a risk to fund the capex by debt or equity dilution.

again in such a situation it does not deserve the present forward p/e of 43 times for Mar 16

We are making a generic point about the desirability of free cash flow (a characteristic of mature business) without taking into consideration the specifics of a quality emerging moat growth business like Poly Medicure.

Poly Medicure is a quality emerging moat business in VP Portfolio, but by no means a mature business. At the same time there is enough evidence/track record of predictability (less variables being in medical devices) and sustainability of its prospects (very difficult fro another emerging player to match its cost efficiency and IP).

It is also true that current valuations are running ahead of actual business performance. But that it is true in this market, for any business with high quality & good growth prospects. In this thread or elsewhere I have read about Poly Medicure that there is a disproportionate future awaiting Poly Medicure - if it has to grow to next level, it has to get a strategic JV into US MArket, bag very large OEM assured offtake contracts, or get acquired by someone who finds in it a strategic fit.

The point is this business is still in its early stages of growth. It will need all the cash it generates and more to fund its growth requirements. Free Cash Flow is not the holy grail in growth stages of an emerging company - Pat Dorsey makes this very very clear in his book - 5 rules for successful investors.

As long as D/E is small, a judicious mix of debt is always preferable for a business that is able to invest that capital at reasonably higher rates than its cost of capital. Poly Medicure is certainly able to do that.

Yes one should be cautious of high valuations - which means DO NOT BUY at these levels, as there is no margin of safety. For those invested from earlier levels, the decision to stay invested depends on the conviction one has in the Management and the predictability/sutainability of its business performance.

Disc: Invested since VP Portfolio Recco with >10% holding.

4 Likes

This is the business I understand from AR

India’s medical device market is currently the fourth largest market in Asia with 700 medical device makers, and ranks among the top 20 in the world.

The industry is very fragmented with more than 65% of Indian manufacturers falling in the SME category.

The market is still highly import dependent with 77% of the market consisting of imports.

High quality, high tech products are sought after, particularly by facilities run by corporate groups such as Apollo Hospitals, Fortis Healthcare, Max etc. An estimated 95% of all new hospital beds created in recent

years have been in the private sector and future increased demand for medical devices and supplies is ikely tocontinue to come mainly from private sector hospitals and medical centers.

US Safety Syringes Co., LLC, USA: 75% owned by PolyMedicure, did not have any business activity and

accordingly Poly Medicure has provided a provision for diminution in value of investment of this company

during the current year.

It is nice to say so many things like explosive markets,etc but we dont have a data to support this. Pl answer my questions

1.The pricing power/arbitrage will diminish in the coming years. Major part of their sales is exports which is mainly done by arbitrage/cost difference. This market is not comparable to a software industry.

2. Is there enough market for all the players and where Polymedicure can grow disproportionately. Compare Infosys in early stages. There the market size was huge to accommodate and grow.

3.It is low margin business and how long the present margin can be maintained. Infosys margin was very high in initial stages.

4. Check with any hospital guy like Apollo and he will tell you there is no negotiation for a company like Polymedicure. They have supply at the prices quoted by Hospitals.

5. Where is the moat in their products? Compare this to AIA Engineering which is still perceived by the markets as a commodity player.

6. US Markets - yet to penetrate. Subsidiary is a failure. If somebody is doing well in the US markets , it is a sustainable business.

These are my views and I may be wrong but confidence and conviction is not there which is a must for an investor.

2 Likes

You have done some work on the company - which is a good sign.

-

However from your comments, it looks like you don’t know enough about the business. All the questions that you are raising are old hat - sorry to point out that you haven’t taken the trouble to go through this thread carefully. That is the first thing I recommend you do. Start from the first page of this thread - enough pointers for every question you have raised

-

Why there is nobody who is able to compete with Polymedicure will become very clear when you study the numbers of its closest competitors - especially on the margins front.Have you taken the trouble to do that

The best part about a forum like VP is you can cut short the investigation into any existing business by going striaght to the heart of the matter - study the strucured content on the Company like the Poly Medicure stock Story, and Poly Medicure Management Q&As - if I am not mistaken there are interviews almost every year for past 3 years with Management - that gives yiu great insights into most of the common questions raised by anyone, including yours.

Most people form the opinions very early - based on generic patterns - which is not bad - it gives you some sort of an hypothesis to start with. BUt when you get into the specific context of the business in question, its industry, the competitive positioning of the company, you may find enough data - to even reverse your hypothesis which was short on facts.

Get the fact sheet right on the business. Then get a feel for the Management. That’s very important. Poly Medicure is featured in VP Management Q&A Insights presentation - not for nothing right? Mr Market has not been giving it premium valuations just on whims - High Valuations can’t sustain over whims and fancies over 3-5 year periods. Go over the history of the inclusion of Poly Medicure in VP Portfolio in 2012, categorising it as an A+ Category business.

Something form above should strike you right - that your hypothesis could be half-baked and short on facts? How can you have conviction when you are lazy on doing the homework on the business - there is a wealth of information & analysis of very high order available on the company - and pointed out several times in this thread itself.

Valuations is a different game - and you may not be comfortable to buy or hold at these, perfectly Okay! But please start on the homework. Some of your strongly held opinions may change about the quality and sustainability of the business.

6 Likes

Polymed has to compete with imported products within India and abroad they need to compete with B Braun , BD, Baxter, J&J outside India. B Braun is having the same EBITDA margin for the last five years. So is the case with Polymed. If we go by your argument that it is a disproportionate business why EBITDA margins have not improved. A stability in EBITDA margin shows a mature business not a growing business or dis proportionate business.

I could find all the names like Braun,BD,Baxter in FDA site but not Polymed. this is somewhat perplexing. Do you have a document which says they got USFDA approval for all its four facilities. I could get some newspaper reports in this thread. Not even a filing with BSE/NSE

US is the largest market for medical devices which Polymed is not able to penetrate.

Highlights

- BCC Research estimates the global market for medical device technologies as $390.3 billion in 2012. This indication has reached $411.8 billion in 2013 and is expected to reach $538.7 billion in 2018, registering a compound annual growth (CAGR) of 5.5% over the next five years.

- North America as a segment will grow from $187.6 billion in 2013 to nearly $225.4 billion by 2018 at a 3.7% CAGR for the period 2013-2018.( No presence at all)

Asia is the largest segment of the global market for medical device technologies and it has reached $7.1 billion in 2013 and is expected to reach $10.8 billion by 2018, increasing at a CAGR of 8.5% from 2013 through 2018. ( Braun is already present in Vietnam, etc) India so much fragmented where price plays an important than quality and it is doctors\hospital driven)

A future growth for Polymed comes from maintaining the present European share( doubtful), penetrating US (no concrete plans yet) and Asia (we all know about India, no presence except a small one in China)

I dont give much credence Management Reports as full details will not come out for various reasons and always biased except for some mature companies.

I also suggest you read the Management Report given by B Braun to understand the business more fully and the hurdles in the business.

I will be happy if you come with a convincing data instead of browbeating me. Produce some convincing data instead of verbose.

5 Likes

Thanks for more objective data cited, now.

Sorry, I still have to punch holes in facts cited:

- In Value terms IV Cannula (45%), Safety IV Cannula (6-7%), Blood Bags (10-12%) are the main product segments. Safety IV Cannualae segments hare is unlikely to grow more than 10% share in the near future

Counting the international biggies as major competition is true only for 6-7% of Poly Medicure current business

-

There is no presence as yet by Poly Medicure in US Market. The strategy is not be a direct supply but pursue OEM relationships to crack that market - perhaps the entrenched players hold on the distribution set-up is a stranglehold and as of now Poly Medicure doesn’t have a wide basket of safety products (only those can sell in US market) that makes it interesting for top distributors to consider it.

-

The disproportionate future cited - is from an expectation of something that has to happen - in its cracking the Developed markets bid - it is in a exciting position already as one of the Top 5 in its category after the International biggies.

So its is an attractive acquisition target itself; It can form a JV with a large OEM - that had sealed one in 2013 but fell through at the last minute as the JV partner got acquired; or sign multi-year assured offtake contract with some of the top distribution arms.

Don’t get me wrong - my intention was to nudge you to get deeper into the specifics of Poly Medicure business - rather than judge on the surface purely from the numbers - which many smart investors like you are prone to do (with generic comments minus product segment specifics, my impression was certainly that)

I am glad after the hard barbs, discussion is now veering to hard specifics of the business - and not numbers-based superficial opinion-bazi only, as some seniors like Donald like to call it.

Lets discuss more on why or why not Poly Medicure

a) Has a long runaway in front of it

b) Is the business very predictable

c) How sustainable is the business - do we see anyone cming and dislodging the business from its perch

d) How likely is something disproportionate to happen in medium to long term in this business

3 Likes

This is what I have been missing on value picker for sometime. A charged up discussion on stocks. Thank god we are doing it again which provides wisdom and direction to everyone.

Stock is expensive. There is very little in terms of latest updates in the public domain. No result co calls and no interviews.

One FII Matthews has constantly been increasing their holdings in the stock at 500 levels. Did you notice that?

Disclosure: invested

the only data yu have given above is outdated ie dated 27-11-2012 . Do yu know what are the percentages now. Your assumption that 6-7% competition is flawed . Just do your home work. List out the products as given in the AR of Polymed and compare with the products of B Braun, Baxter, BD. Also, management answer as given in 27-1-2012

- Margins will improve - not improved

- Cashflows will improve significantly

- In 2-3 years we should be in a happy cash surplus situation.

If it is so, why are they raising Rs 200 crs and why FCF is negative for the last 2 years. You have a management which is not able to have a visibility of 2-3 years. Compare this with a management like Infosys. I am not blaming the management but the business, a highly competitive one. Also, have you heard of a company called Ahlcon Parenetrals which got delisted from BSE. B Braun’s strategy is very clear here. Please also do some investigation on who is J K Sancheti Oswal.

So many things as retail investors we may not know and we will be last ones to know. My strategy is always playing safe and rely on hard data as every business assumption of mine can go wrong as I am not an insider to know exactly what is happening.

It is better to buy a fantastic/fair/established business at a fair price then betting on a company with assumptions which may go wrong. I am glad to be loser even I am proved wrong.

In this case, we cannot get any data as to sales and growth unless you are an insider. I hope you come back with a data which establishes your last 4 points.

There is no MOS at this price and time also.

Thanks and regards

2 Likes

where it has increased. it is 4.5%. Dont go by FII holdings unless they are highly reputed. In case of trouble, they will be first to sell as they have long hands

Hi @sethufan

I agree with your point, that MOS is low at current levels. However, it is extremely important to identify and categorize businesses in their respective quality slots, so as whenever you get favorable entry point you lap up the opportunity with both hands.

You are doing the right thing by wearing a skeptic’s hat. That is necessary for developing conviction. I got interested in Poly Med first time from Kiran’s (@dkirand) blog. Link

I will leave you with Kiran’s ending note,

However, there is a long ramp for Poly Medicure to grow at 20-25% CAGR. Medical disposable business is an evergreen huge business (unless, there is suddenly a replacement of IV Cannuale with some other tech.) And FY18-19, Poly Med can start selling Safety IV Cannuale anywhere in the world (Braun’s patent expires). Safety IV cannuale is 3-4 times more expensive than IV Cannuale. Think about the impact on revenues and margins.

1 Like

@Prdnt_investor

This Kirans note should be before Braun’s acquisition in India. Polymedicure advantage/arbitrage goes away when Braun manufactures these in India. Pl think. And Poly medicure does not have any FDA approvals to its credit unlike Braun and this is the most worrying part. Which one is better Braun from India or Poly from India. I think we need to dig deeper to find answers. We dont have data in this case unlike KITEX. We dont know to whom OEMs they are selling, how much in Europe and how much in USA. 80% of the sales from exports. That means they sell less in India. Exports we dont have data and we assume they are able to sell because of cost advantage which goes away when the product competes with Braun India.

Unlike Pharma the market may not be huge here for so many generic players. We need to find the answers.

2 Likes

Corporate Presentation by company

http://www.polymedicure.com/wp-content/uploads/2015/06/CorporatePresentation.pdf

It gives %age wise revenues from each segment

@sethufan FII holding has increased from 4.94 to 7.15 last quarter. Price was broadly in range of 500 +/- 25. So we can assume the FII increses 2.2% at about 500 (http://www.bseindia.com/stock-share-price/poly-medicure-ltd/polymed/531768/) . Though I agree with you, we should not pay much attention to this data.

Company has defended itself well in Europe. For USA, out of 4 manufacturing plants in India , 1 is audited by USFDA. I think competitors will put spirited fight in US market and it may not be wise for PolyMed to spend money on legal issues. I will wait for further clarity on 200 Cr. spend. Hope they will spend some in brand building.

Point to be analyzed “New regulatory regime Drug and Cosmetic Amendment Bill 2015:Largely unregulated industryOnce the amendment is enacted, manufacturing of standard quality products will become mandatory and the Company believes it is uniquely positioned to quickly corner a significant market share from unregulated players”

Also on Braun manufacturing in India, will they reduce cost ? esp. in euro markets. Otherwise cost advantage stays…

3 Likes

@kittystocks

Braun and BD are the largest players in Infusion Therapy with deep pockets. They are already having a good presence in India. In fact, Braun is having 3 set-ups in India. When 100% FDI is allowed, what is the need for a JV partner who is not going to add any value. This point in the presentation I dont understand. Braun just bought out AHL and they did not form a JV.

How to determine the market size where 69% of sales come from infusion therapy. That is the problem. Is that market big enough to accommodate all. Why company is not disclosing the name of the manufacturing facility which is approved by FDA. Compare the patents Braun is having Vs Polymed.

I think Polymed is more like a CRAMS supplier to some MNC. What are their direct sales. Why they were not successful in USA.

It is a very competitive space and driven by hospitals and doctors and unless we get a clear picture of the above questions, it is better to play safe.( Buy at a price with MOS)

1 Like

Any update on this company? Stock has been extremely weak for a long time no in the abscence of any news

I just looked up the B Braun India website. Posting some points

The products of B. Braun were available to India con sumers for more than two decades though channel partners. The Company came into existence in 1994 as a joint venture between B. Braun and a local India company.

The company established a factory in Ponda, Goa for manufacturing Medical Disposables in 1996 and then it re-located to Chennai in the year 2007, which manufactures IV Sets and Sutures, Right Heart Catheters along with other blue chip products. Since 2001, all the products available in the international markets were introduced in the Indian Market which led to a marked increase in its range and turnover.

The future of B. Braun in India holds a lot of promise mainly due to its double digit growth plans, improvements in healthcare facilities in the country.

Details about the 2 plants

-

Chengalpet Plant (Tamilnadu)

The state of the art Production facility near Chennai in Tamilnadu was established by B. Braun Medical India Pvt. Ltd. in 2007. Today, it manufactures over 2000 different types of Surgical Sutures. With an output of over 20 Million units of Sutures per year, it provides employment to over 200 people. It is operationally integrated with the B.Braun Center of Excellence (CoE) for Sutures in Spain.

As a part of the Aesculap Division, it contributes significantly to the global supply of B.Braun Surgical Sutures. Close integration with Best Practices at CoE and Standards based on US and European Pharmacopoeias ensure best possible Product Safety & Quality.

-

Hyderabad

B .Braun Medical (I) Pvt Ltd (BBMIN) has successfully acquired a controlling stake in Oyster Medisafe Limited (Oyster Medisafe). This strengthens B. Braun India as the customer’s first choice for Safety Infusion Therapy.

Oyster brand carries a wide range of medical devices including syringes & needles, types of I.V. Infusion & transfusion sets, crape bandages & other infusion, transfusion & urine collection accessories. These products are well accepted in the market as Oyster Medisafe has sales and distribution channel operative across the country selling and distributing its products.

Moreover, Oyster Medisafe’s manufacturing plant has a state-of-art infrastructure as well production quality systems in place. The facility meets with various standards (GMP & USFDA) and also has ISO 9001:2000, EN ISO: 13485 and CE certification accreditations.

5 Likes

Hi All ,

This is my first post on valuepickr. I have been silent reader on forum . After going through some of post in this thread , i went on to do further research and first thing I did is to check on management integrity as prescribed by master value investors . Yes, this management has delivered phenomenal returns however numbers may not speak about integrity of management is what I eventually found out .

I stumbled upon an interview by Himanshu Baid MD, Polymedicure on youtube . I further did a look up for him on Google news to find out recent headlines made by him .

To my surprise , I stumbled upon this Indian express article " Three firms that bought land from Vadra have records riddled with holes" . Some excerpts from article are as follows :

These three firms are all linked to Faridabad-based manufacturer of medical disposables Poly Medicure Ltd which is linked to the family of Congress leader and former Rajasthan Finance Minister, the late Chandan Mal Baid. According to records, the three companies, Allegeny Finlease, Sachchiya Enterprises and VCB Trading, own 14.1%, 3.5% and 4%, respectively, in Poly Medicure. These companies, as first reported in The Indian Express on November 27, paid three to seven times the price at which Vadra companies were buying land in the same areas at around the same time. - See more at: http://indianexpress.com/article/india/india-others/three-firms-that-bought-land-from-vadra-have-records-riddled-with-holes/1/#sthash.zW5I7pZX.dpuf

Yes, this company may have good future and has shown good numbers in past . However, I’d like to hear perspective of Senior members on the forum if they would advise investing in a company which may be mired in corruption with low management integrity .

1 Like

Hi Manish,

This issue has been discussed earlier. Read the past posts in the same thread.