Came across these comments on Quartz from a competitor Aro Granites on the Alpha Invesco blog. Might be sour grapes; but needs consideration.

https://www.alphainvesco.com/blog/tag/aro-granites/

5 Likes

Pokarna looks like full of uncertainities: 1:Increasing Debt, 2: Chinese competition, 3: US slowdown, 4: Ikea factor i.e. success/ failure in India.

Disclosure: Invested.

People who are commenting here influenced by Aro Granite,will be requested to go through Caerserstone Annual Report on market size a bit

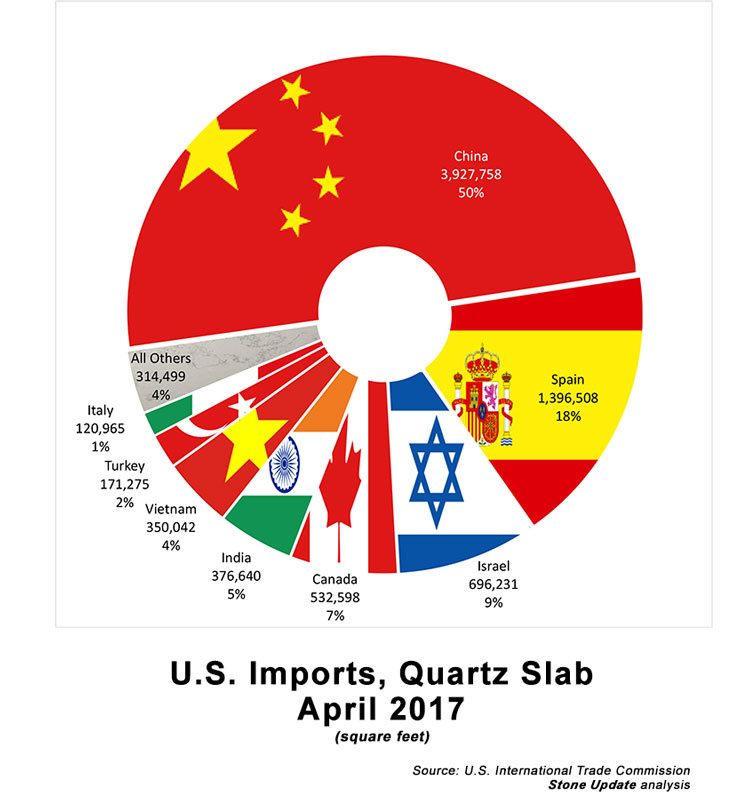

U.S. Surface Imports April 2017: No Stopping Quartz?

For April 2017, U.S. imports of dimensional hard surfaces seem to be more of the same … as in more recovery for granite, and more of a stupendous growth curve for quartz slab.

Imports of “worked” (cut, one side polished) granite in April cut its losses to only -1.5% compared to the same time last year. Yes, it’s still behind. but the deficit is lower and shipments show some uptick from previous months, especially with Brazil.

Quartz slab, meanwhile, continues its skyrocket pace, with an April-to-April growth rate of 30.6%. China supplied half of the shipments to U.S. ports-of-entry – which isn’t surprising, given its doubling (and then some) of exports to the United States for this April.

Other stone sectors stay on pace, save for a lessening of growth in worked marble. Travertine still faces challenges as Turkey lags behind its 2016 pace; the catch-all Other Stone category, meanwhile, continues to grow with a large upturn in shipments from Brazil.

Stone Update continues with its experiment with doughnut charts featuring national flags. We hope that you continue to enjoy the new look; for the editor, who’s on a low-carb diet, these are the only doughnuts he gets all month.

5 Likes

Hi guys, did you find any update about the quarterly results and AGM of the company ? August is about to end but the company has not notified anything. Isn’t this surprising ?

Thanks

Kanv

Maybe they are transitioning to IND-AS and sought the relaxation for reporting q1 by September 15. Just my guess since I saw a similar case with another company.

https://www.google.co.in/url?sa=t&source=web&rct=j&url=https://www.nseindia.com/content/equities/SEBI_Circular_05072016.pdf&ved=0ahUKEwi865W16-TVAhVKp48KHQdlC6QQFggwMAE&usg=AFQjCNGvOHjniZvb7dF-VhaUCH4-yYYc3Q

Yes, why there is no news on Q1 results?

Red flag?

Thanks.

Please find below. Q1 earnings on September 18. http://www.bseindia.com/corporates/anndet_new.aspx?newsid=d635d48a-8e49-4ebf-927a-b79284f62dcc

This is a notice for AGM and not for Q1FY18 results

1 Like

As per Annual report of Pokarna(16-17) , Ashish Kochalia as on 31st Mar was still holding the stock .I met Ashish Kochalia last month ,he confirmed that he still holds the stock .

Not able to post the link for Pokarna annual report of this year -read the full annual report today -very nice read -shows how strategically the company is looking “future backwards” on opportunity /size of prize -expanding quartz capacity by 130% with IKEA as partner for domestic demand -more importantly have truly identified Quartz thru technology as "true differentiator "

His holding is close to 7.5 % as on 30th June2017

1 Like

In the AR, I am astounded by Quartz overall market. Execution will be key. Also how IKEA picks up in domestic market in H2 2017-18, that is more important

They also seems to be the distributors for Raymonds. Owns about 6 stores ( Hyderabad & 1 in Mumbai) for their own branded apparels -Stanza .

I think they have decided to divest their loss making apparels business. .

Am a late joiner to this thread. This is certainly one of the highest quality threads on VP - thanks and congrats to all those who joined this party early.

A handful of queries for the seniors on this thread:

-

Has anybody got an opinion of Shantilal Daga who audits the company? What is his reputation in the Hyd CA market - a google search says he is on some big national level committees of ICAI? What is the reputation of other companies he signs off on such as Srinivasa Hactheries, etc?

-

Concerned like several of you above that the 130% capacity expansion for Rs 325 cr will suck out all cash flows for the immediate future. Luckily management has provided a wealth of disclosure in the FY17AR

(a) The expansion is apparently funded Rs 75 cr by internal accruals and Rs 250 cr debt. Is anybody aware where the expansion will be? As in physical location - is land etc already tied up and paid for? Capital WIP in FY17AR is less than Rs 3 cr - does this mean expansion is so far only on drawing board with no money spent yet? Is debt tied up already - with the CDR history, will it be difficult to raise debt, given that Debt/EBITDA will be greater than 3?

(b) What exactly will the Rs 325 cr be spent on (sorry for such a basic question) - what sort of machinery will be purchased and from what sort of vendors (all from Breton or do they only sell technology)?

© Even after reading the ARs, analyst transcripts, and this thread; I cant get a fix on capacity utilisation. WIll revenues (for quartz) be stagnant until the capacity expansion is complete (assuming they are maxed out already on existing capacities)? How long does such an expansion usually take?

In case anybody already has all these answers, please do share. Am hoping these will help me build the conviction to add to the position on what appears to be a very reasonably priced stock with good growth prospects.

Disclosure: Been holding a small position (as % of PF) for eighteen months. Never had the conviction to add to it.

The answers to some of your questions can be found in the Conference Calls held by the company in previous quarters. I’ll list what I have:

[quote=“arsh13, post:403, topic:1863”]

Capital WIP in FY17AR is less than Rs 3 cr - does this mean expansion is so far only on drawing board with no money spent yet? Is debt tied up already - with the CDR history, will it be difficult to raise debt, given that Debt/EBITDA will be greater than 3?

[/quote] The debt will come on the balance sheet from Q1FY18. They’ve had the debt sanction for a while now. Not sure what the debt will cost, we’ll probably get that answer soon.

[quote=“arsh13, post:403, topic:1863”]

(b) What exactly will the Rs 325 cr be spent on (sorry for such a basic question) - what sort of machinery will be purchased and from what sort of vendors (all from Breton or do they only sell technology)?

[/quote] The machinery is all from Breton. That itself costs around Rs 300 Crores.

The company has intentionally not revealed much about capacity utilisation in their con-calls. They say they don’t want their competitors to know. Their FY11 Annual Report says that they can make 8,89,500 sq. meters of Quartz Surface. But I think they’ve already reached the peak capacity utilisation. Revenues are likely to stay stagnant unless one sees increase in realisations (which can happen as Pokarna seems to be getting better prices). Their new line should be operational by June 2018 and should operate at 60% capacity in FY19, generating Rs 100 Crores of revenue. From FY20 one will see 100% utilisation, of course assuming that the demand doesn’t die. Addition to top line of Rs 250 Crores and EBITDA of Rs 100 Crores.

If all goes according to plan then Cash from Operations in FY20 will be Rs 200 Crores. Whether things will go as per plan or not is anybody’s guess. My big concerns are collapse of US Housing Market sales, INR appreciation, P/E contraction if a bear market hits us by FY20.

Disc: Invested and looking to add more

3 Likes

@jprasun it is a good summarization. Just one point, in case USA Housing market collapse, not only Pokarna , the whole world will take a beating. You remember 2008.

For me more important , whethere Pokarna is able to show top line growth. As per AR2016-17, Pokarna is very clear that they want Growth with Profitability. Means they will sell provided they have good returns. That is a good practice. But market will regard cos that have earning visibility and decent growth too

Both points taken @nil_71

I am still relatively new to investing. And thus lacking experience & ability, return of capital becomes much more important than return on capital and the choice some times ends up being between a bank FD and equity, and not between one company and another. With Pokarna the USA housing market collapse becomes even more significant because that is their primary client base and so far their main claim to fame. I also own Ujjivan, and I’m considerably less worried about the impact of USA Housing market collapse on Ujjivan.

With the additional debt of Rs 250 Crores being taken, their total debt will be close to Rs 450 crores. That may tie up their hands a bit. But I’m optimistic and as mentioned in my previous post expect double CFO couple of years down the line.

1 Like