I was going through this link and found out that Granite, marble and other stone’s import data by us was given in MT but for Quartz it was in Sq Feet. Can some one tell me the reason for this. Also if some one can help to convert the Sq Feet data to MT.

The next real trigger would be if the company can continue is this 20-25 % topline and 30 % EPS growth. Given their reluctance to talk about cap util, and their focus on jumbo slabs which can give higher realizations, its a difficult one to judge.

Does anyone know if they run all shifts or only one at their plant ? can they sweat their assets further ? if yes, this has a lot more runway.

@varadharajanr In one of the interview management said that they could export only 200 cr worth of quartz and even after such meteoric rise of quartz export from India their rise wasn’t there. So I am assuming that they must be running at the maximum capacity before this capex. However instead of EPS growth I wuld be interested to see their Cash Flows and capital allocation. Even if you assume 0 growth for next year and profitibility same as December quarter, Pokarna becomes a blind buy.

200cr sales figure was for FY16. They have increased operations to 7 days a week along with increase in no. of shifts. Realisation will improve on bigger sized slabs. So I think full capacity utilisation will come faster than expected. It seems that they might announce another quartz line sooner than expected. Any announcement of major debt reduction will be a trigger in the medium term.

1 Like

Sumit FY16 is still going on and if you see the increase in YOY sales figures from Stone update they just don’t add up. There is no increase in Q-o-Q sales from last 3 quarters so I think they are already running at full capacity. However, I am not sure how much their realization will increase with the increase in slab size. Secondly, if they are going to add another plant then I don’t see any reduction in debt infact it will go up but I would be interested to see the Capital Allocation, primarily to see how much money are they allocating to their Granite and apparel business. If the increase in WC of apparel business is high, say more than 10cr, then I will blindly sell the stock because that would confirm my suspicion of Siphoning off of money through that business.

I have burnt my hands badly because of Promoter issues in Tree House and Eros and I don’t want that.

Your call to buy and sell but I think if they delay investments someone else will fill the gap in case the demand is there.Don’t think a rising brand will risk that. A new Bretton line will cost $30-50m which is 3-5 yrs worth of profit in my opinion. Easy to fund but absolute reduction in debt level will be postponed for few yrs.

As I said Sumit, I don’t have a problem if they invest their money in Quartz division, I have a problem if they increase their WC in stanza or their apparel business. And I think with the margins they are making from Quartz presently, it won’t be more than 3 yrs to cover the cost. My bet is on the product and a leap of faith that management is not crooked and not diverting the money. My all queries would get settled after their Annual Report comes out or the Audited Balance sheet for FY16

I recently enquired a sales manager in HomeTown furniture and kitchen cabinets and countertops in a mall in Bangalore. He was selling Quartz tops from Caesarstone . When I enquired he said they are selling this company as it is imported and they are not selling Pokarna. May be Pokarna should start concentrating on domestic sales also. I wonder Is their Capex utilization being completely used for exports and not able to produce more quantities to supply domestic market in addition to exports.

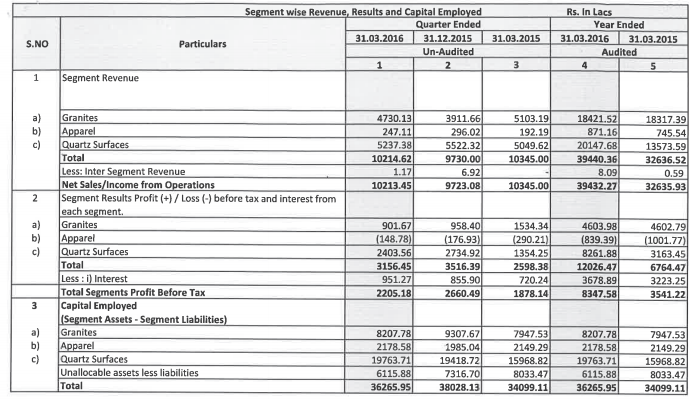

Great set of numbers. Would have been greater with higher sales growth. Dividend of Rs 10. Exceptional item of payment for CDR restructuring.

1 Like

Good result… The growth rate will be lower going forward in the quartz segment due to base effect… A 15-20% growth will be more than satisfactory…Another factor we need to consider is the increasing supply from competition. There is little differentiation in the products which could lead to price wars. Will be interesting to see how Pokarna deals with it this FY.

Exit from CDR is a great feat…The company now trades at EV/EBITDA of 6.4 still at a discount to Caeserstone which is at 11.5

2 Likes

Thanks for the update!! What’s the EPS for this year? Consolidated shows 82.5 and for FY 15 its 50.58. Whereas both moneycontrol & screener are showing 95.8. Has it gone down?

EPS excluding exceptional item is 110…screener is showing TTM eps iam guessing…

Meanwhile…

1 Like

Thanks, that’s a disappointing number I guess

Headline EPS of 110. Look at eps before exceptional items. Calculated adjusted EPS would have been close to 97. Company had made provisions already and these are non-cash items.

Disc: Invested

Thanks, for the input.

Invested at 1,144

Wonderful set of numbers! As management indicated, their EBIDTA has improved. They are doing Capex in quartz division as visible in the balance sheet. Will add more if it falls tomorrow,

Disc, Invested

Hi Sumit,

How are you doing this calculation. Mgmt reported EPS excluding exceptional is 110 Rs. How did you get to 97?

Also I thought the mix change was interesting - commoditized granite slowing, branded quartz growing

See my calculation below

9M EPS = 110.84-37.21 = 73.63

Q4 adjusted PAT = Clean EBT* (1-T) —> 22.0518 *(1-0.33) = 14.77 cr

Q4 adjusted EPS = 14.77/0.62 = 23.83

FY adjuted EPS = 73.63+ 23.83 = 97.4/share

assumption that they remain @33% tax rate. Hope this helps.

Few questions that need to be asked to the management

Low sales growth ?

Work in process capex is for quartz?

Why costs higher in Granite division?

Management in their interview said that they will do approx 200 Cr in quartz this year (because of capacity constraint) and Capex is to increase the production and Slab size of the quartz stone as it fetches more price in the market. I watched that interview somewhere in Moneycontrol.com

For Low Sales Growth question:

From Q4 presentation by the company -_1. “Heightened competition and currency headwinds impacted granite business’ momentum during the year.” _

2. "Lower utilization levels coupled with higher operating costs resulting in muted performance. "