Is this spooking the PEL today?

Seems like you are right. The market seems to have been spooked by the surge in yields of Lodha group. Other RE paper too may see similar surges.

What amount funded to Lodhas, any idea?

Total exposure to Lodha Grp is Rs 4300 (as mentioned in the concall)

Lodha dollar bond sees sell off…PEL as large exposure to Lodha

https://t.co/cws7IMtGji

The loans are towards specific projects rather than to the holding company.

Piramal is known to force RE companies to liquidate unsold properties even at a discount to manage cash flow.

Disclosure: holding

Credit report on Archean Chemicals -

Archean Chemical-R-30082018.pdf (283.4 KB)

Looks like Archean chemicals has delayed debt payment in past and it is surviving by refinancing debt!! The products of the company are in commodity and has many headwinds ! It is risky bet by PEL though they will earn higher interest rate!

Well, I have noticed quite a bit of desperation on the part of Lodha to liquidate its unsold inventories. They are running good offers but don’t think they can go beyond a point to sell stocks. They badly need IPO to succeed and that too before elections to deleverage its balance sheet. It feels like something is not right and some or other issues are being brought deliberately to delay it. Who in sane mind takes USD loan @12%.

Check out @myvaluepicks’s Tweet: https://twitter.com/myvaluepicks/status/1067737078283231232?s=09

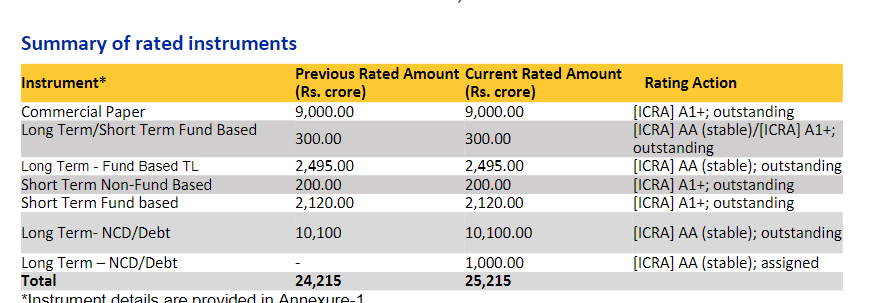

Issue of Rs. 2125 Cr privately placed NCD @9.5% for one year and 500 Cr @9.75% for 2 years.

They recently raised a ton of capital. Any idea if these are CP rollovers or new cap raise ?

This is a fresh NCD … and it is secured (CP would be unsecured) … So don’t think it is a rollover.

The Credit rating agency is comfortable with the liquidity position and is expecting a reduction in debt as the company monetises some of its investments as well as Financial services receivables come in … THis rating is given on 26th Nov and I think Lodha issue surfaced on 27th Nov … we have to wait for the next tranche to understand the impact of Lodha issue as assessed by the Credit Rating agency who may have more access to info than press or public …

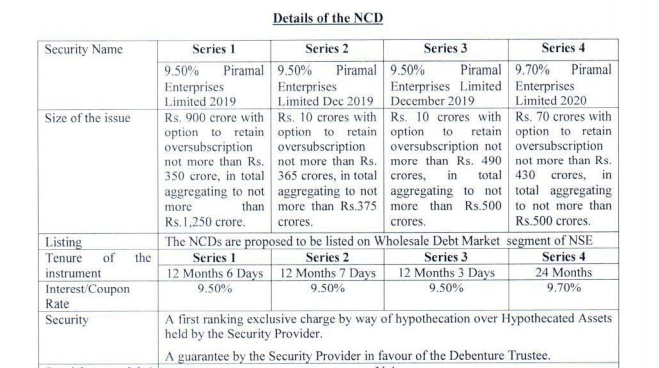

The NCDs for not for 2 years but one year plus a few days for most of the issue, only one series is for 24 months for 70 crores with an option to retain 430 crores.

A snapshot below

May be pertinent to note that this is not raised by the housing finance entity of Piramal, but the parent. Next, the rates are about 9.5% quite high compared to 360 day CP rates of a comparable firm like HDFC that traded at 8.6% (11 months). And CPs are unsecured, Piramal Enterprises has the highest rating there, whereas these debentures have been raised with a lower rating promising a security (first ranking exclusive charge) as well.

(from NSE website)

So raising funds at a higher rate with much higher security is, to me, indicative of some strains in funding. Seems like a quick bridge finance even if at higher rate with the hope they can refinance it a year down the line at lower rates.

I am also concerned by the similar rise in yield for Edelweiss. There is no denying that perceived risk has gone up for all RE financiers. However, there are two factors that need to be kept in mind. For the short term, these NBFCs have raised floating loan rates so they can afford to take higher yielding liabilities. Second, if they remain optimistic about their RE business over the longer term, it is time they support them with adequate funding at whatever rates they get to keep them going. There is price difference of 8-12% between under construction and finished inventory due to GST. The first priority is to get them to finish the construction before they could hope to recover dues.

The NCDs were raised by Piramal Enterprises Ltd. while the real estate business is housed only in Piramal Capital and Housing Finance Ltd. Unless we assume the PEL is funding the latter there is really nothing to suggest this is for real estate funding.

Why Piramal is raising too much money? are they facing repayment from existing borrowers?

avg rate is 9.5%…was it not high?

Just curious…Raising long term debt when interest rates are supposed to be downtrending…

Must be mouthwatering opportunity to invest…

Edelweiss , Manappuram etc raised at around 10.5 . So relatively its less