hello All, I am new to Rights issue and got the basic idea about what it is all about.

Investors who have 23 shares in their demat account on the record date can subscribe to the rights issue and get 1 share (if allocated) at a price of 2380.

My question now is

When a right issue is fixed at 2380 and the CMP is close 2800 will there be a correction in price or will the price shoot up.

I do not have any shares of PEL and would like to invest, I cannot buy 23 shares at this point in time. So before buying the shares (1 or 2) I would like to know when to buy them.

Io make a start buy1 at cmp and wait if price falls buy more.Even if u hold i share u will receive rights issue form with zero entitlement.If u apply for 1 share u will get it.

I have few questions:

a) I have 25 shares of PEL but in two demat accounts(10+15). Am I eligible for the rights issue?

b) My demat accounts are ICICI and Zerodha. Are these brokerages providing the facility to apply for Rights issue or there is no restriction as such.

c) Let say, I am eligible for X shares via right’s issue. What happens if I apply for 2 or 3 more shares in rights issue than I am eligible for ?

Will try to answer your questions

a) I guess you need to have 23 shares in one account to be eligible for rights issue. It will be based on DPiD/Customer ID combination.

b) All online brokerages should provide facility to apply for rights issue online. I could apply Infosys rights issue some time back from ICICI. So they provide this facility for sure. Not aware about Zerodha.

c) You can apply for more shares. Whether you get additional shares or not is a function of % of over/under subscription to the rights issue.

Right issue price was disclosed few months back and market was aware of the tentative ratio (from rights issue size and rights issue price, one can arrive at this rough number). The stock price would be based on how effectively and quickly company use the right issue money.

Nandini is daughter of Ajay and Swati Piramal and is director of Piramal Enterprises. This interview helps us to understand Piramal’s value system and their vision.

Piramal Enterprise

Highlights of Q3 and Nine Month results

Financials

Q3 Performance

o Revenue up by 22% to 2858 Cr

o EBITDA up by 21 % to 490 Cr

Nine Month Performance

o Revenue up by 26 % to 7648 Cr

o EBITDA up by 25 % to 1176 Cr

Loan book grows by 68 % to 38000 Cr and 23000 Cr rupees loan also approved but it will be disbursed in this quarter

From past 6 year revenue has grown at a CAGR of 29 % and Net profit 41 %

Company is giving 45 % annualised return from past 5 years comparing to nifty 14 %

Piramal enterprise is now among Top 5 Company to give highest return and growing consistently at revenue and net profit.

Loan book grows at 95 % CAGR from last 5 years.

Pharma Segment is growing at 14 % CAGR from last 7 years.

Company is going to raise funds of 7000 Cr

o 5000 Cr from Convertible Debenture which will be used for Financial Services Segment

o 2000 Cr from right issue at 2380 per share in which 90 % underwriting will be guaranteed by promoter. It will be utilised in Pharma segment.

Company is continuously giving ROE of 21 % , Gross NPA is 0.4 %

Strong pipeline of loan book is there worth 23000 Cr already approved by maintaining healthy asset quality.

68 % growth in Q3 with multiple products and value added product.

Loan Mix has also been changed

o In 2015, 85 % of loans are from real estate

o In 2017, 24 % is from real estate, 47 % from construction finance, and 17% from Indian Corporate finance loan.

Company is maintaining 25 % ROE from last 10 quarters this quarter it is 21 % because of infusing 2300 Cr in Financial service segment.

Company also got approval of reverse merger of Piramal Capital and Piramal Finance in Piramal Housing Finance.

CARE Rating also up from “AA Stable ” to “AA Positive”

In Q3 pharma segment revenue has grown by 6 % to 923 Cr it is low because Q3 is last quarter for all global pharma client so they do not keep stock in last quarter. It will be normal from next quarter.

In 2011 Company got 29 USFDA approval and also passed 91 other regular audit

In Q3 Company cleared 4 regular audit and 35 customer audit .

Company will focus on Gastro segment in pharma.

Q&A

Kindly give some brief on company’s reverse merger?

o Company wants to operate entire loan book on one single platform which will include loan of Real estate, Corporate Lending, Construction finance so this step of reverse merger is taken.

So after Merger, Company’s net worth will reach 10,500 Cr?

o Yes

On other income side how much have company earned from shriram investment?

o Around 1000 Cr is earned from shriram investment .

Give outlook on Domestic Pharma growth ?

o In Domestic pharma, company is still in investment & growing stage in top line. 90 % of total revenue comes from exports in Pharma segment.

What is your outlook on Real estate?

o Company has done a JV with Bain & raised fund to finance in real estate sector.

How company will be planning on in Mumbai region real estate ?

o Entire real estate industry is consolidating so it is not bad. Customer wants quality now. Finance is not only done in refinance but a lot of new launch comes & company had supported them a lot.

o Developers are also changing focus to affordable housing and company is focussed on financing more to self-employee segment because 50 % of people in India are self-employed. Company is focusing on tier 3 & 4 cities only

o Company helps developer by providing end to end solution. Company can even buy a land for developer and finance for construction.

o There is De-growth in loan book of structural finance because it has high risk.

What will be company regional strategy?

o Focus on real estate whole business will be there. Company has recently started functions in Surat and Kolkata also. Company study the region first and then enter in it.

o Housing finance is game of low NPA and company got stabilised in Mumbai region. Company now focuses on Delhi , Noida , Gurgaon.

o Company study and take time to get on decision if company like the region then they enter in it.

What about Corporate lending business?

o In Corporate lending company only give loans to suppliers that need expansion to cater their demand.

Is there any interest accrued model?

o No, in Real Estate Company get payment of interest every month so there is no interest accrued.

How company diversify risk in its loan book from past 2 years?

o Company gets benefit of diversifying by Risk adjusted return that Rating agency let them to do. Interest cost of company has also gone down by only announcing of merger.

o Company gets rating of individual product from rating company and work with them very closely to always improve the Rating. Higher the rating lower is the interest rate so it drives cost of borrowing down.

From which segment loan comes majorly in real estate , self employee or salaried ?

o Currently 75-80 % loan demand comes from salaried people with average ticket size of 40-50 lakh.

Is leverage level comfortable for company?

o Leverage level is always maintained between 4-4.5 % and company works very close with ICRA so company never cross this leverage level.

What is the company’s yield rate segment wise?

o In structural finance it is 15-16 %, Construction finance it is 13-14.5 %, corporate finance it is 14-15 % and other 12.5-14 %.

What are the new sector company look to finance under corporate finance ?

o Major focus will be on renewable and solar sector.

Why company has 2 % provision?

o It is not actual provision. Company is very conservative so it is done in advance.

When will company separate its business company wise (demerger hint)?

o In Mid of 2018 it will be done.

As tomm feb 1st is the record date for rights issue…do we see price of the share adjusting rather than correcting? tata steel record date is also feb 1st i think it has corrected a lot today…but i guess both the right issues are somewhat different…any please throw some light on this

Also why market is not valuing the consistent performance it has delivered over the last many years?

stocks which are not worth at all are raising a lot in this bull market

I have a doubt here, with respect to “right issue and share price”. Say if a retail investor has bought 20 shares around 2800 level. And if the the right issue is happening at 2380 and if the stock price is adjusted to the same(2380), which is a 15% fall for the retail investor isn’t it ? Is it ok to book a mere loss and enter after the right issue ? Requesting for more clarity and understanding.

PS: I searched previous responses, there was no conclusive response which I can grab.

Stock price would hardly reduce by 1% or so going by straight forward calculation of 23 to 1 adjustment. Market could react taking into prevailing sentiment (not necessarily related to rights issue)

My math would be as follows:

Lets assume CMP is 2700 (for easier calculation)

23 shares * 2700 = 62100

1 share @ 2380

Total = 62100+2380 = 64480/24 = 2686 after the rights issue

Senior boarders correct me if the approach is wrong.

Calculation of Right is done theoretically. Yes @pandi.rao this is correct.

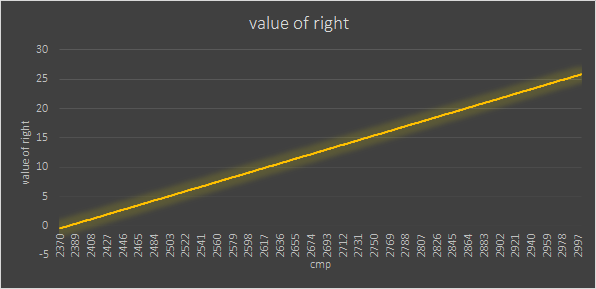

Market value of 23 shares today = 23 x 2743 = 63089

Value of one rights share = 2380

Total value = 63089+ 2380=65469

Total shares = 24 Expected adjusted price per share = 65469/24 = 2728

Value of Right = 2743 - 2728 = 15

Obviously these are just textbook methods. If you notice this is a linear function vs CMP. Something like below.