While the draft letter of offer for the rights issue can be found on the SEBI website, the same cannot be said for the final letter of offer. But for the Tata Steel it is found updated. Not sure why such a discrepancy exists.

I think the final letter will be filled with the date of issue opens and date of when this issues closes…i think it will be done after today…in the draft letter also the date of issue and closes are blank…so we can assume that final letter holds all this details i think

Considering the rights come without paying the STT, which creates some taxation hassles later on, at what price does it make sense to forgo the rights and buy it market price? My gut feel says it is around 2400.

I didnt understand…you mean to say we are better off buying from the market at 2400 levels? already it is at 2500 i think we can get to 2380 levels in coming days given the fact there is a global rout and heavy sell off…Dow doesnt fall the most in a history…there is something to it telling us the markets are ready to correct more maybe even 20%…

Hi @deevee - On the purchase on PEL since you had purchased at a high price, what is the approach (or best approach) to take, average it out as it falls or book a lose and again purchase once a bottom is formed

This question is not particular to PEL but asked more of how to approach.

Market can always behave in an irrational manner. We have to decide what is appropriate for us. So there is no rule to say the price cannot go below 2380, just because the support exists.

If I remember correctly, Godrej Consumer Products came out with the rights issue in 2008 at Rs.123 and the market price was quoting below that. So the promoters had to underwrite the issue. But we can say that is in 2008.

As I see, Piramal has timed it to his advantage because promoters are underwriting the rights issue in a company which is considered mostly as holding company and hence has a natural discount to its intrinsic value. The value will be unlocked only after the de-merger. Until then investors who would like to own Piramal for its Finanacial Services may be put off by its Phrama division. The same applies vice versa as well.

Piramal has been stagnant for like 8-9 months now. Is it consolidating after a huge rise in Mar-April, or is market waiting for all the recent acquisition (pharma products & DRG) to bear fruit?

Anyways, I did some back of the envelope calculations:

Book value per share for FY '18 = 23500/20 = 1175.

Stock available at 2550 implying 2.2 times book

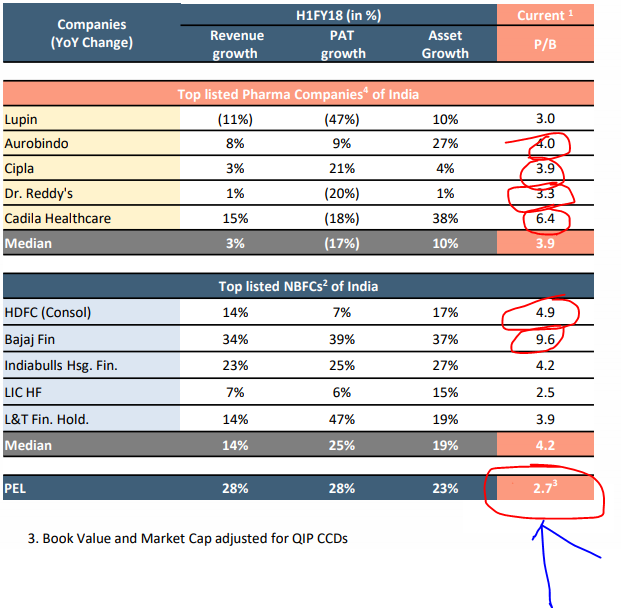

Other OTC pharma companies (GSK, Merck, Sanofi etc) trade at 5-10 times book. PEL’s Finance could also command a 3.6-4x considering its growth potential and high ROEs. I won’t give it a holding company discount because I like both their Finance & Pharma businesses, and, demerger toh hona hi hai.

A company with promising businesses, very strong governance all the more so important in India (the 50k crore Vakrangee comes to mind ), a mind-boggling track record of superior performance, available at 2.2 times book.

@deevee@sgjaclyn@suru27@sajijohn

Experienced VPers please point out the flaws in my reasoning as it seems in my excitement (especially today during market carnage) I would surely have overlooked some serious facts.

Piramal Enterprises has entered into a JV agreement with Bain Capital Mauritius Bain Capital Mauritius will buy 50% stake in India Resurgence AMB, a wholly-owned subsidiary of co After the transaction, India Resurgence AMB will cease to be a subsidiary of the company. @proficient2014

Hi, Anything we can think why it is not getting the due attention even though it is one of the best performing in terms of revenue roe etc.? why the DLL holdings is very low? why the most analysts doesn’t have a coverage? is it because for any analyst to predict the growth…he has to have idea in financial services…pharma DRG OTC analytics? which is very tough to have ?

Hi sir,

BVPS of 1175 was arrived at taking into account CCDs and Rights both. The ppt doesnt include that I suppose. And price during latest results(Jan 30) was hovering at 2800. Yesterday it was availbale for a bargain below 2500

Further, whats your opinion of DRG? Is it a significant drag on ROC?

Can we apply for Rights share thru our bank website(thru which we usually apply for IPOs)? Or is going to the designated bank branch with the application form and cheque the only way? I don’t reside at my registered address, so can’t get the form. Any alternatives? please suggest.

because I like both their Finance & Pharma businesses,

because I like both their Finance & Pharma businesses,  and, demerger toh hona hi hai.

and, demerger toh hona hi hai. ), a mind-boggling track record of superior performance, available at 2.2 times book.

), a mind-boggling track record of superior performance, available at 2.2 times book.