It would be interesting to see how Ajay Primal works to develop PEL Financial Services in the near term. Given PEL and subsequently PEL Financial Services would hold a large amount of IDFC and IDFC Bank, PEL Financial Services to merge into the IDFC and IDFC respectively is definitely possible. Unlikely RBI would give PEL a licence to become a bank but given he has been given a verbal nod for the Sriram/IDFC merger speaks volumes of his stature. He folding up the PEL financial services part into IDFC/IDFC Bank looks like a forgone conclusion. PEL Financial Services working on the entire value chain of Real Estate Financing and SME/MSME structure financing would bring in good fit to the IDFC/IDFC Bank platform which is still absent.

Further update on gains by Piramal’s investments in Shriram. As per the article, Piramal made mark-to-market gains of Rs 2,787 crore on investments in two listed entities of the Shriram group

I believe merging of PEL finance with IDFC entity will not happen. PEL finance will be listed separately and they might acquire other NBFCs later. Later option is better for PEL and its shareholders

after going through Piramal interview with Eco times one more angle seems obvious …many top mgt personnel leaving as some with aspirations to suceed didnt get the coveted offices …creating some vacuum and strain on PEL resources to handle it …IDFC under Lall would be easily be able to do it

That is , if it strictly a financial investment …if not then we would know some years down the line

plus it helps them experience and understand a bank at close quarters at another’s expense before taking the plunge or merging which ever way

The benefit of low cost of funds for banks is overrated. CASA deposits may be low cost, but generating them requires heavy investments in retail branch network, technology, staff costs etc. Banks also suffer from CRR / SLR restrictions and in general, a lack of operational flexibility and heavier compliance burden compared to NBFCs. IMHO, NBFC (borrow wholesale, lend retail) is a better business model than banks in today’s environment.

“In the long run, if ever there is a black swan event, you do need a fall back and that’s where a bank will help”, Ajay Piramal said in the ET interview. What Black Swan is he referring to? Does he fear a mass default at Shriram Group’s retail assets (for whatever reason) – which can be bailed out by regulators if the assets are on a bank balance sheet rather than an NBFC? Someone help me on this.

Terms such as IDFC getting “access to Shriram’s retail asset base” or customer network etc. are vague. They will not necessarily translate into more business for IDFC Bank. Why should borrowers of Shriram Group’s consumer loans (or truckers!) open CASA accounts with IDFC Bank when their salary comes into some other bank? CASA accounts are day to day operational accounts, and customer’s choice here is driven by very different considerations than whatever brought them to Shriram for loans.

Banking requires a very different mindset – banking is transaction oriented, action oriented. Banking requires a personal touch. NBFC and Infra financing are very different, you cannot change the way you work overnight. Even culturally I suspect IDFC to be very different from the Shriram Group – a merger is not just an arithmetical addition of two Balance Sheets.

I tend to agree with Anil Singhvi on this - IDFC shouldn’t have become a bank in the first place. And now, this doesn’t look very convincing either.

Disclosure: No exposure to any of the companies mentioned - IDFC, Shriram or Piramal Ent.

Piramal Enterprises Limited’s Annual Report wins Gold at LACP’s(League of American Communication Professionals) 2016 Vision Awards Annual Report Competition. PEL’s FY2015-16 Annual Report earned 98 out of 100 points. The awards benchmarks and recognises best practices in international financial reporting.

Another feather in the cap of Piramal Enterprises.Please see the news item below -

As per data from Screener, Piramal’s ROE at consolidated level is just 9%. Is it not very low? Do they have any target level that they want to achieve ROE in future?

Piramal Enterprises is also concentrating on improving the ROE of the company. At present ROE is 25 per cent.

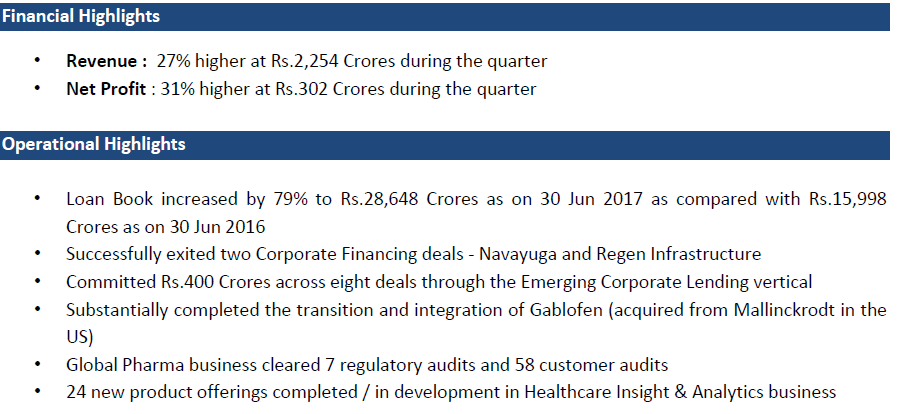

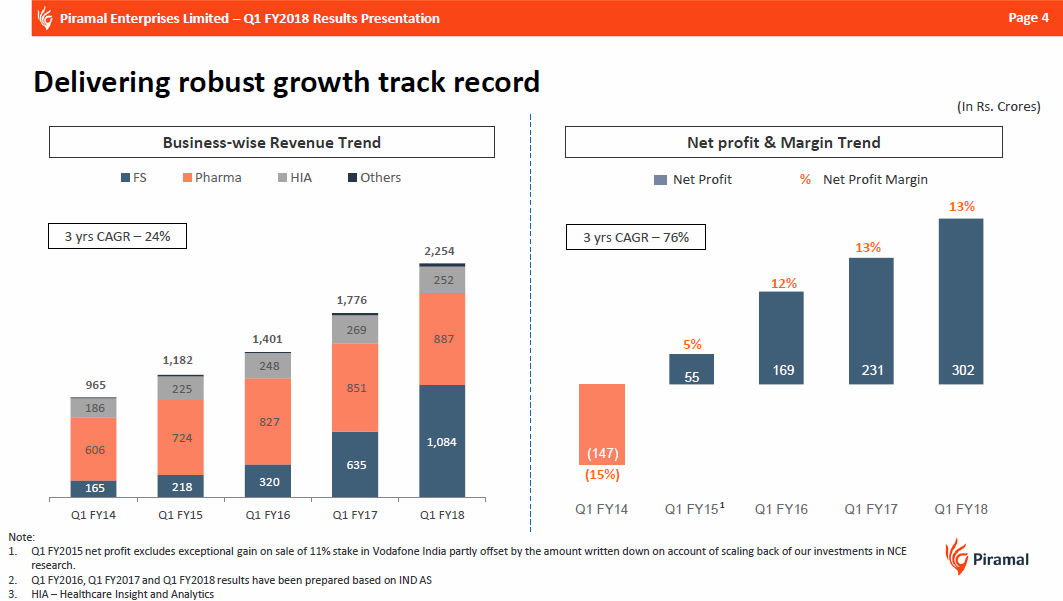

At the AGM today, Ajay Piramal indicated that PE is growing its loan book aggressively. Total Loan Book grew by 79% to Rs.28,648 Crores as on Jun 2017 Crores Vs. Rs.15,998 Crores as on 30 Jun 2016 (company presentation made to the exchanges).

PE’s finance business is looking to diversify into other areas in order to reduce concentration on the real estate sector. Emerging Corporate Lending is the new vertical that began ops in the June quarter.

Piramal Bain JV has received license for Asset Reconstruction Company. This JV will handle the group’s stressed assets business.

Housing Finance Corporation licence is expected in August, according to Ajay Piramal.

According to him companies like Piramal Enterprises will gain much following the introduction of RERA. Replying to a query by a shareholder he says only 10-15 per cent of the developers will remain in business and others without bandwidth will have to leave the business. Piramal Enterprises hopes to lend to the big developers.

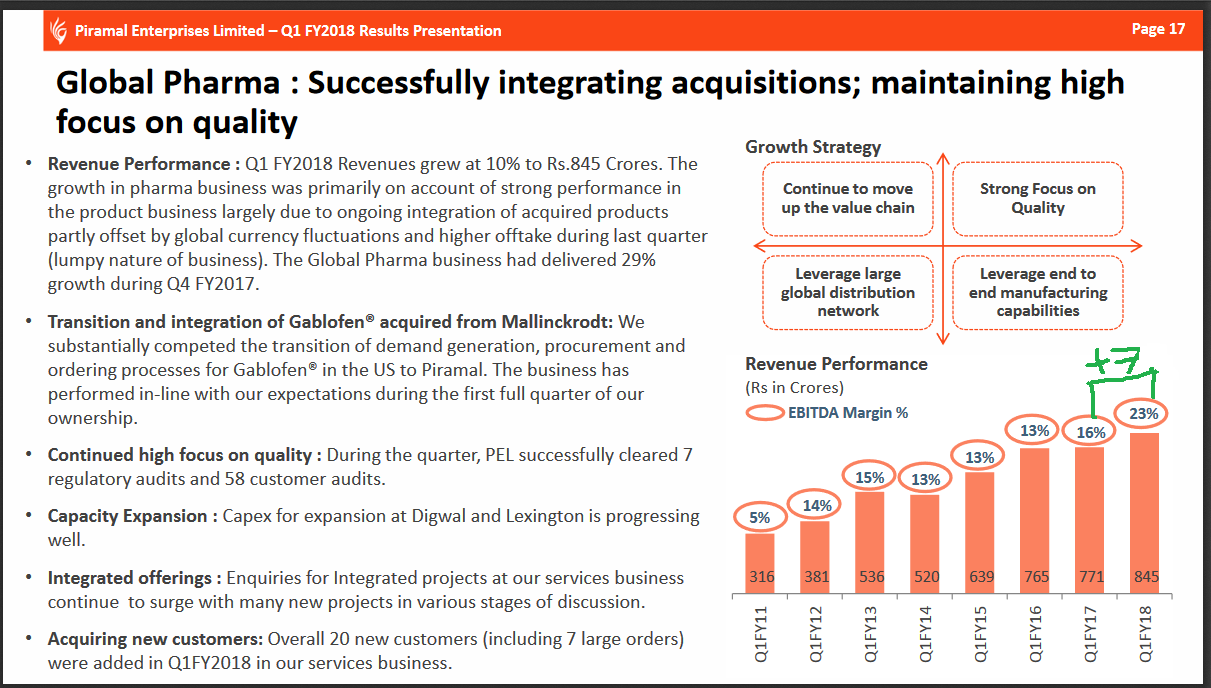

Replying to another shareholder, Piramal said the government’s move to enforce generic marketing of medicines would be a big negative for the company and consumers in general. People would not be able to differentiate between manufacturers who maintain quality and those who do not, he said.