sometime back i read on a blog (dont remember which1), when top executives resign - first sell ur position and then ask Qs on reason of resignation

Disc - researching, not invst

looks promising but plenty of -ve, high risk script

sometime back i read on a blog (dont remember which1), when top executives resign - first sell ur position and then ask Qs on reason of resignation

Disc - researching, not invst

looks promising but plenty of -ve, high risk script

Hi,

CEO is just another employee in a company, with more authorities and responsibilities. CEOs come and go, I think an investor needs to track how the promoter (the owner) is growing the business.

Dilution of Equity - Promoter might infuse funds. This can be a positive.

As I see it from the actions of the promoter, he is in favour with the current regime in Bengal. He diversified just before the elections to mitigate risks of regime change.

Also giving loan to the company at zero rates and then converting that to equity, this is a far smarter way to convert than via QIP or rights issue, especially if you know that sales are going to zoom in future.

It may very well be that the money he is infusing in the company is of politicians of the current dispensation.

When I asked the IR, where will the promoter bring money from??? He said, he has certain ancestral land which he will sell and infuse the funds in the company. Now, post demonetization, when we look at the latest investor presentation released by the company; we see a lot of investments planned - in logistics, in packaging and in distillery. What i am thinking now is - Is this an impact of demonetization ??

Where did demonetization come in this picture?

As for land - number 1 way for politicians to launder money.

Ya I know that…was just wondering why has company suddenly announced such aggressive growth…and that too in today’s world where focus on core process and outsource every other activity is the trend…the company is doing exactly opposite…

when bladder is full (with money from politicians … guessing) … people urinate

that differentiates between great capital allocators like piramal / ajith issac n mediocre allocators

Isn’t this much dilution hurts the shareholder’s returns?

What are these FCCBs? Are they fully convertible to equity? If not, what’s the % of equity part?

Interesting discussion. Tempted by growth…controlled by several red flags. Some similarities with opto circuits - high debt, frequent bonus announcements…Hope it will not end up like opto circuits.

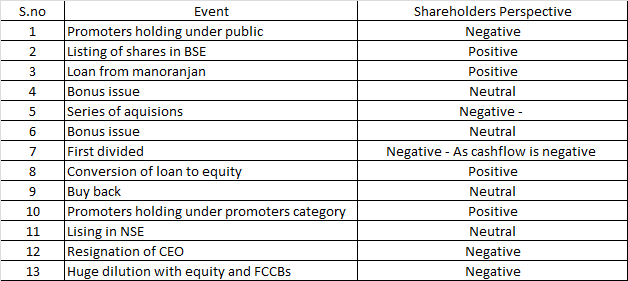

How to interpret the ideology of promoters from the sequence of events…

These are the sequence of events as I remember. I will edit if any corrections suggested by members

Dics: Holding from lower levels

Hi Abhishek,

Couple of questions regarding the recent Board meeting at PS.

These are some of my concerns, already invested in PS.Your views will be appreciated though I admit my research and knowledge is nowhere close to yours.

Last but not the least, we have a small group of serious PS investors,where we discuss the ins and outs of PS, a few members even visited the factory in Calcutta and met Roy, and are in touch with the management, it would be great to have you in our group, if you choose to be a part of it.

First of all, glad to hear that you guys have met the mgmt and seen the factory…would definitely like to be added to the group…

1). PS has finalised this in their board meeting…so now probably the EGM should take place where they will take the shareholders approval…they are going to do it through postal ballot… IR said

2). Yes…that is what he is going to do…so to the extent of Mr. Roys contribution to PP will not bring cash to the company…it will only impact the debt equity…it will become low to that extent…promoters holding will go up to that extent…

3).Yes not only fccb, but pp also…they will be shorty announcing that too…

4).IR said, they are not going to issue fccbs right now…they are just taking the approvals so that they can issue them and raise funds whenever they want…so debt equity is not going to explode…

5).same answer…

6).same answer…

7).totally agreed…fccb are good options to raise funds but can skrew the century old businesses at time of crisis…the IR said that they would be very cautious on their debt equity going further…

They said their main focus for next year (fy18) is to generate positive OCF…they are quite confident on that…that should happen with less inventory days needed…and hence less working capital requirement…

First off, disappointed with the disappointment…

Yeah, got that on approval.

Got it, on increase in stake and converting loan to Equity.

Yeah, learnt about CP for FCCB and PA floor price. But also realized that, the importance given to CP, in case of FCCB is just pure baloney! I, as an investor, will keep a hawk’s eye on what PS is planning to do with the funds raised, is it for aggressive growth plans as chalked out in Investors Presentation?(That’s a healthy sign) OR is it in anyways used to pay off / reduce existing Debt,( Borrow from Peter to pay Paul), that will be a red flag for me.

Got that too. If FCCB is Liability to the books, its also infusing funds, to fuel growth, and when used wisely, who knows, Roy can reduce Debt off the profits itself.And also if at all, the CMP of PS in near future hits the CP, and the bonds are converted to Equity, Debt(FCCB issued) will also get reduced by that amount and of course number of shares will increase same way. Time will only tell.

and 6. Not an issue any more…

FCCB, hope when ever issued, it is hedged (considered as a smart move against currency fluctuation). Again wait and watch situation.

Lets see how Roy walks the talk. The Investors’ Presentation is pretty aggressive.

And finally, many thanks!

Deepali

I had talked to IR and they had mentioned that more details of the conversion price will come out in a few weeks.

You mentioned that you have met Monoranjan Roy and have also seen the factory. I had a few questions on the same:

Thanks.

Hi Rajeev

Sorry for a delayed response.

Now, there’s a big hullabaloo even in our PS Investors’ group, over the

Conversion Price of FCCB. But my personal take is(since I’m an "investor"

in PS and not a “trader turned investor”), it’s of NO importance,

whatsoever what CP, is because the bond holders are no idiots to give loan

to Roy if they don’t find the deal attractive. For us,

Investors/shareholders ,only thing of prime importance should be what are

Roy’s intentions/plans to do with the proceeds of FCCB money, and also if

he is actually adherering to his plans. Which is a positive for me. Or is

he simply taking a loan to clear off his previous debts or cover up some

stupid expenses. That’s a big red flag for me. Also it will be considered a

positive if the FCCB are hedged, PS can hedge their payments to bond

holders using currency swaps or currency forward contracts.

To cut to the chase I wouldn’t speculate over the CP.

Secondly, not to speculate over FCCB conversion to Equity leading to

dilution, because if conversion occurs, then debt will also get reduced by

that much.

I have not met Roy, but my group members have, more than once and are

prolly planning again shortly.

But, of what I heard from them about Roy, is that he is a frugal, pragmatic

person, a workaholic and passionate for business guy. Even his office

doesn’t look that impressive, (saw from the pictures taken by my group

members),which I take to be positive.(not squandering money on unnecessary

things), like Peter Lynch says,“

The extravagance of any corporate office is directly proportional to

management’s reluctance to reward shareholders”. Also he has a thorough

knowledge of the business, the ins and outs and has a vision to have a

2700crs revenue by 2019(as per latest Investors Presentation). Roy has bet

his own bottom dollars in PS by giving a 60 Crs interest free loan to the

company. That speaks aplenty.

Hope the above reply was helpful.

Deepali

BTW, the price for allotting Preferential Share warrants is fixed at 73.

Deepali

Thanks Deepali. It is good to know about some of the details that you have mentioned about Monoranjan Roy. Actions speak louder than words and it is good to hear that he is making the money count by not spending it frivolously on office decor and so on. Look forward to hearing your answer on the 2nd question.

Regarding preferential share I had heard that it will be 75 but I have not seen any official communication from the co on the same. What is the source for preferential share price of 73?

Rajeev, you can go through Company’s website OR read this article on Roy,

-managing-director-pincon/

Regarding PA, I got the email from the Company for e-voting, I am pasting

the part, which shows the price as 73. You can do the math, by dividing 42

crores with 57 lac shares …

Deepali

Thanks Deepali. Very helpful.