Please find answers to the above questions raised -

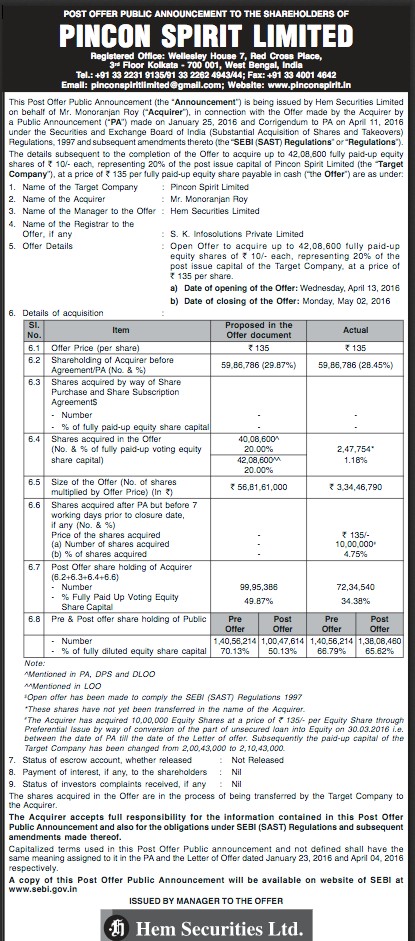

1). Mr. Roy has not started Pincon from scratch. He has acquired it some years back. He acquired 30% stake without making open offer. There is a SEBI guideline on this. Since he had not made the open offer as per SEBI guidelines, he cannot be classified as a promoter. Now, he has done the open offer. the new shareholding pattern should reflect him as a promoter.

2). Even I had this issue and I have raised this question to the IR team. They should come back in a day or two.

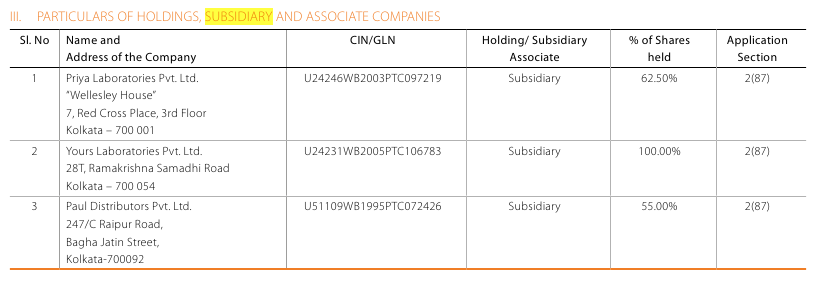

3). There are only 3 subsidiaries - Paul, Yours and Priya. They are bottling and distribution business. The finance companies you are talking about are group companies and not subsidiary co.

Please check and do correct me if I am wrong on the third point.

FMCG segment which is edible oil is also grew from 182cr to 281cr, growth of 54%. Has any other company in edible oil segment grew at such a pace? Why would pincon FMCG segment grew at such a scorching pace?

Hi @Sowmay

I believe this is due to expectations of positive results on Monday…(Just a guess)

People expecting good results from Pincon on account of elections…

and while GM Breweries has not given good result…if Pincon gives good results its going to get valued fairly in coming times…

Consistent performance does give confidence…

Things to watch out for…

Revenues from Orbitol…

And any increase in margins (gross or net or both) would be super positive

Thanks for sharing Abhishek, really appreciate your depth of research.

I had some qns if you could help with your thoughts

Why did mgmt get into the Oil refining & marketing business? Isnt the distribution very different from alcahol? Just trying to understand the synergy of the 2 businesses?

Why did company borrow from 60 cr promoters instead of from banks? Do teh banks see some issue and not lend? Will the promoter converting remaining debt 50 cr to equity keep diluting shareholders?

The branded (manufacturing business) generates an OPM of 8-8.5%. Isnt that the best case margins for them? how wil margins improve to 14-15% in 4-5 years?

Your thoughts on OCF, Capex and FCF next 3 years?

Thanks vm!

Discl: Invested and trying to ascertain adding in recent corrction

Looking at the risks section, I had the following questions:

Based on base rates, what is the probability management will be able to hit the projections for e.g. 60% market share, improved margins, 3000Cr turnover by 2020 etc.

What is the bear case for not investing?

Have you looked at scenario analysis whereby specific actions taken by say a GM/ Radico etc. will materially impact the Pincon business model?

1). All these projections are given by management - either in AR or in media interviews. This is also reflected in the performance of the company over years (check screener.in). OPM has been consistently increasing over years. In last interview, Mr. Arup Thakur told that they are expecting OPM to soon get into double digits and we can see the evidence of that - “Pincon hikes prices”. He also said Pincon is now almost in a monopoly in WB in country liquor segment. 3000cr by 2020 is given in their AR.

2). Please refer the risk part in my presentation.

3). Globus spirit is coming with distillery in WB. IFB agro is already there in WB. But, Pincon is doing far better than them.

Disc - Please understand and keep this in mind that this sector is very risky to be in. The mortality rate of the business is very important. You cannot enjoy sound sleep with this stock. Prof Bakshi calls such stock having a temporary moat. Pincon does enjoy political support. Please do not get amazed with the growth part alone. The risk is much more in this counter. Prof Bakshi keeps saying this - understand how the business is earning money!! Is the way of earning correct on moral grounds? When you pick stocks like pincon, you immediately start thinking about the shifting trend among youngsters, social status, etc. and you think positive, but you never think about rapes happening daily, domestic violence, etc which is caused by liquor !! Even if the stock becomes a multibagger for you and you get out at the correct time, and then it comes back to where it was; remember your research was wrong. So, I am just trying to experiment here and learn. This stock no more forms part of my core portfolio. Do your own due diligence.

1). I have no idea why they tried to diversify. But, yes they somewhere in the AR wrote that they are trying to leverage the position of their Pincon brand by diversifying.

2). Promoter has a 31% stake in the company. He wants to raise it by substantial % (it seems). This is the reason he has been doing this. It is unethical. But, yes it is comforting me. He sees a huge potential in his liquor business.

3). They currently earn 8-8.5% margins in branded business. They plan to get virtual monopoly (50-60% market share) in next 2 years time. Check the margins of GM breweries and other peers. They are much higher than 14%. But they have their distilleries too, when Pincon doesnt have its own. So, Pincon can easily make 13-14% over next 2-3 years. Arup Thakur recently told they are expecting margins in double digits.

4). No clue about cash flows. For next year, I expect the cash flows to be still negative. Can predict beyond that.

According to Q4FY16 results FMCG segment i.e edible oil is grew from 182cr to 281cr, growth of 54%. Can we verify this growth from some other source. Why would edible oil segment grow at such a pace?

1). Yes this is a big issue. Very few companies in this business make profits. We need to check this out.

2). Unethical in a sense that he could have done a rights issue - giving chance of further investing to each and every shareholder. This is just a point. Not a red flag for not investing. But its good he has infused his capital to bring the capital structure at optimum levels.