My Reply on PIIND on another forum reproduced here for members’ reference :

Your concern of slow domestic segment growth is absolutely valid especially in the backdrop of sharp negative growth reported by the segment in Q1FY18 ; and you will find that I have touched upon the same in one of my post before in this thread dated May’2017. DO go through that entire post of mine which was also provided as pdf link too and you will find my point of view on this. So far, till FY17, it was not a major concern as more or less PIIND’s domestic segment has performed inline with peers. Its just a matter of product mix and geographical coverage that made difference in YoY growth of each year. However, Q1FY18 has been badly hit and that might be because of two things :

(1) GST destocking and company’s relatively strict dealer policies.

(2) Nominee Gold.

Now, first aspect is reversible and we might be able to see results soon but second aspect will pinch the company for current as well as next fiscal till some other blockbuster product emerges to take Nominee’s place. However, management maintaining 10 % growth guidance despite the setback witnessed in Q1FY18 is really an interesting thing to note. Before going any further let us first refer following two statistics :

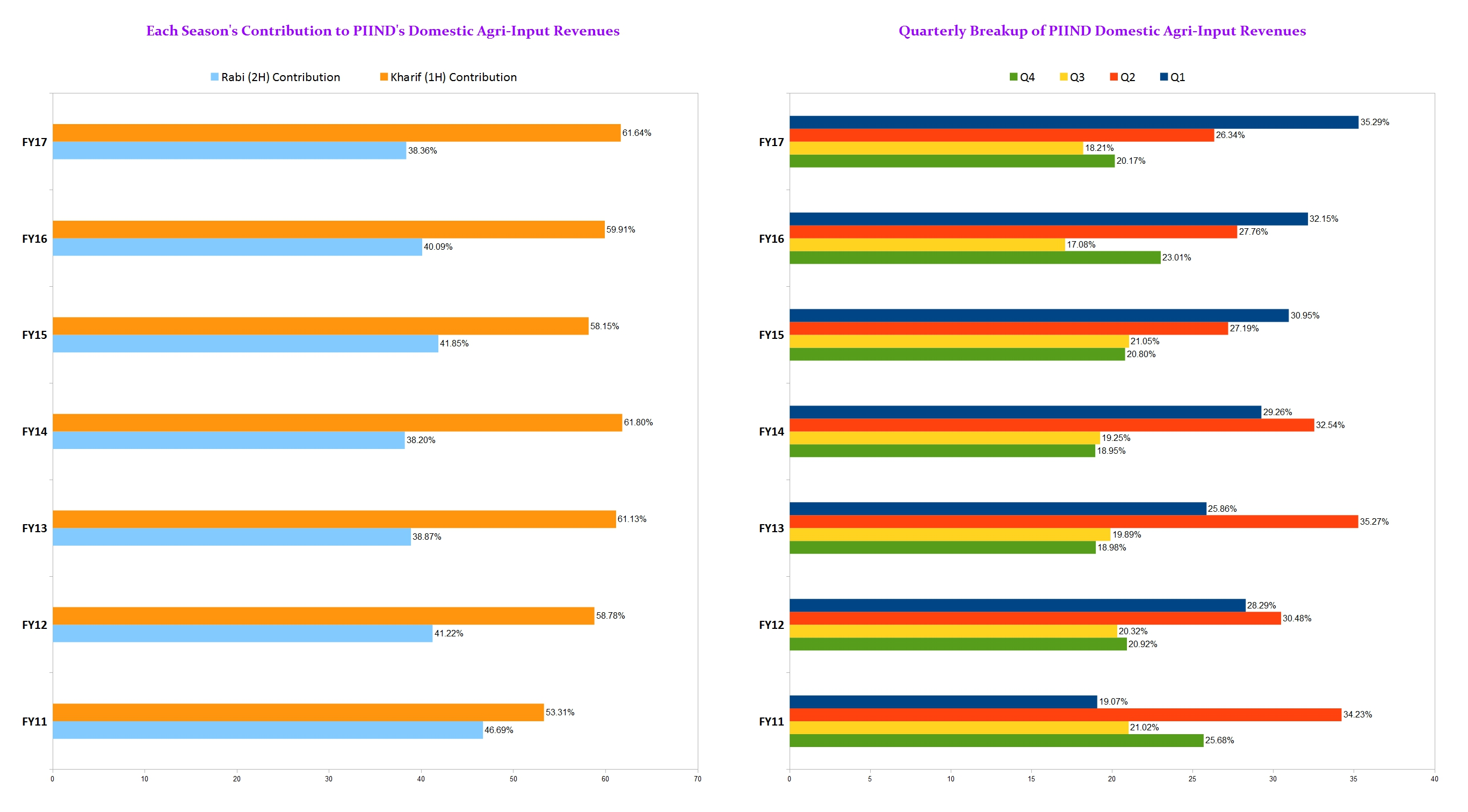

– Now, as one can see from above, it is Kharif which is the most important season for PIIND’s domestic segment and if Q2FY18 is not a blockbuster quarter, to achieve 10 % growth in domestic segment might be impossible.

– Except FY11, Q1 and Q2 of any fiscal has been almost an equal contributor to PIIND domestic revenues with Q1 being a major quarter in last three fiscals. So, a ~17 % loss of sales in Q1 itself might be difficult to recover completely. However, if the management is confident of doing this and even achieve 5 % YoY growth for domestic segment then Q2 has to be spectacular one as far as domestic segment goes.

– For CSM segment, it is actually a quite opposite situation wherein 2H is normally major contributor to revenues with Q4 being the highest contributor. Hence, management bullishness seems quite justified for CSM segment.

– It is also interesting to note that a study of quarterly trends for last seven fiscals’ PIIND CSM segment reveals that company has posted negative YoY growth only thrice, first in Q2FY15 (-14.28 %), then in Q3FY17 (-11.98 %) and last in current Q1FY18 (-11,76 %).

– Same study for domestic agri input segment reveals that company has posted negative growth only four times, first in Q2FY15 (-0.45 %), then in Q3Fy16 (-14.28 %) then in Q2FY17 (-3.39 %) and last one in current Q1FY18 (-16.90 %).

– Order-book remaining at 1 bn. USD+ despite execution is very heartening and management sounded quite confident of future in the concall.

Rgds.

Discl. - Invested in PIIND

No more talk on why PI is falling?

Lesson for me here is that if you are convinced about the story AND company is on track, held it for the period you have in mind when you entered the stock, irrespective of the price movements. Best IF you can add when Mr.Market gives you a chance. And second lesson is not to increase allocation to a single stock or sector that you lose your sleep over it !

Disc: Invested

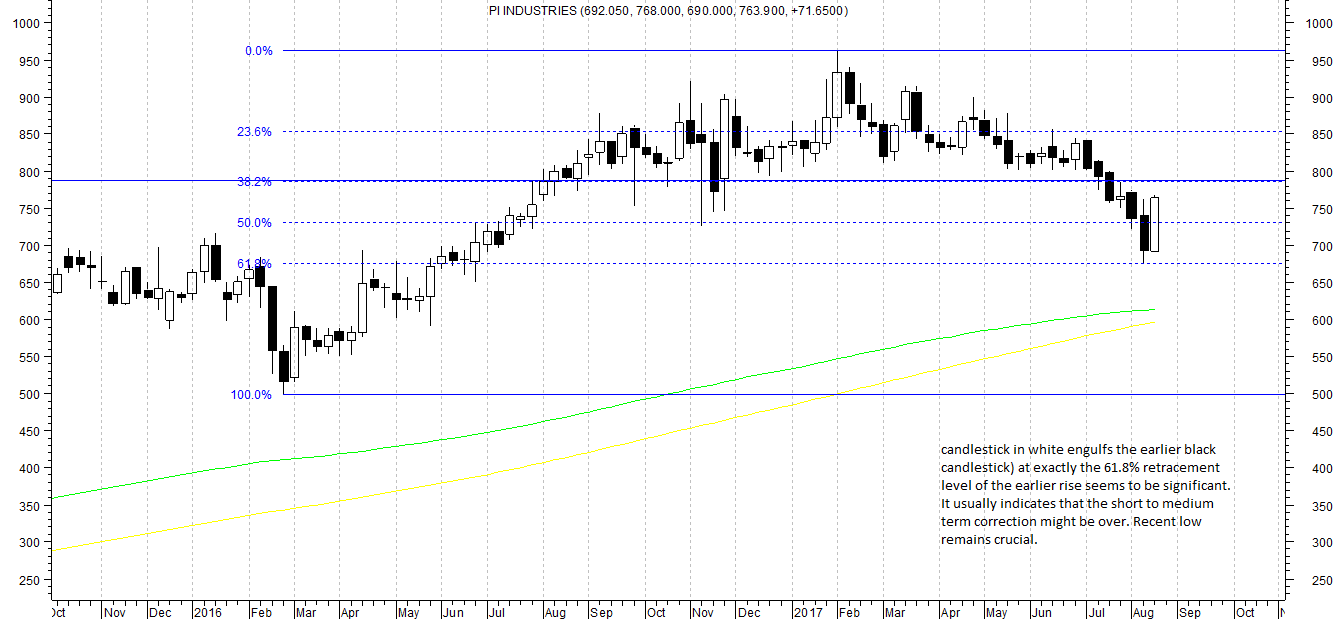

Interesting candlestick pattern on the weekly chart of PI Inds. Sometimes these engulfing patterns are followed by few weeks of sideways moves. We need to see how it plays out in next few weeks.

chart attached with comments put in.

Keeping aside the reaction on price, I found the annual report of PI quite encouraging. Some of the key points I noted are given below:

-

Diversifying into fine chemicals, speciality chemicals and pharmaceuticals: 'Acknowledging the fact that one stays ahead of the curve, we endeavour to expand our value proposition by leveraging our assimilated expertise and skills in the fine chemicals universe, thus going beyond agrichem.

‘Being at the forefront of new technologies, we continue to sharpen our ability to leverage them (our abilities) across different segments of chemistry with biology’.

‘We are also working with global innovators in fine chemicals domain with a view to leverage our respective capabilities to provide a wider range of solutions, beyond agrichem’

‘During the year, R&D undertook development work on 25 new projects covering different sectors i.e. Agro, Pharma and Electronic chemical applications. In the custom synthesis area, eleven new molecules progressed to the next stage and four molecules were commercialized during the year’.

‘Working on new age chemistry, it has carried out synthesis and development of molecules in the fields of Agrochemicals, Fine Chemicals, Speciality Chemicals and Photographic Chemicals’.

Agrochemical CSM industry has size of around USD 5 Billion while the speciality chemical, fine chemical and pharma intermediates size combined will be manifold of it. If one goes through the recent EC report of PI, it clearly comes out that the company’s new expansions are targeting molecules in these segments (even flavours and fragrance and solar chemicals).

-

Updates on domestic agrochemical business:

‘Staying focused on existing patented/proprietary molecules in agrichem space, we are developing many new products/solutions for the Indian markets’.

‘During the year, we launched a high potential product in the domestic market (Legacee). We formed a joint venture with Mitsui Chemicals Agro, Inc. (MCAG) to provide registration

services for their proprietary agrochemicals in India. We also entered into a strategic tie-up with BASF, Germany, one of the leading chemical companies and a well-known name in the crop protection industry to market their innovative fungicides and herbicides in India (plans to launch four products via this partnership in the current year - one already launched)’.

‘Domestic demand for agrochemicals is expected to grow by 6.5% per annum while exports is pegged to grow at a much faster pace of 9% per annum during the same period (FY15 - FY20), Moreover, herbicides and fungicides are expected to grow faster in the coming years than insecticides’.

‘At 0.6 kg/ha, the consumption per hectare of pesticides in India is amongst the lowest in the world. It stands at 5-7 kg/ha in the UK and ~ 13 kg/ha in China’

‘Some of our significant brands like NOMINEE GOLD,OSHEEN, BIOVITA, CUPRINA, ROKET, FORATOX, KITAZIN, KEEFUN,VIBRANT have built a strong association with farmers and a strong recall value in the minds of our consumers. Several of our brands are ranked No.1 in the market in the respective to product category and some of our brands are more than a decade old’.

'Nominee Gold, a flagship product of the company faced generic competition during the year. Your company’s proactive marketing efforts coupled with strong brand recall for the product resulted in growing the molecule YoY’. -

CSM Business: Some of the issues that the AR tries to answer are whether the global agrochemical demand is bottoming out, impact of issues in Chinese chemical companies and how the consolidation amongst the global agrochemical players is affecting PI. Some of the key highlights were:

‘At a time when the global agrochemical industry is transitioning towards a greater consolidation and uncertainties in the Chinese Chemical industry, a greater share of global contract research,

synthesis and manufacturing opportunities are bound to head towards India.’

‘The trust, respect and partnership that your Company has built and nurtured with the leading global innovators over many decades would prove to be an unparalleled enabler of sustained accelerated growth’

‘Thankfully, with early indications of bottoming out of the global crop cycle in sight, the global

Agchem market is expected to grow at a CAGR of 2.7% from 2016 to 2020’.

‘As fallout of a major consolidation, the global agrochemical industry is headed towards emergence

of three global behemoths (formed out of six erstwhile companies), which would control about 65% of the global market among them. In view of the rising R&D costs, most of the global companies would increasingly focus more on their core competencies, thereby generating increased outsourcing opportunities for commercialisation of molecules and manufacturing for proven industry players like us’.

‘The industry is witnessing early indications of the crop cycle bottoming out, with leading indicators like the stock-to-use ratios for key crops standing closer to 10-year averages. The global agrochemical market is expected to remain flat in the coming year, with a gradual pick up in growth expected in the next few years’

‘The recent M&A activities will consolidate 6 large companies (ChemChina & Syngenta, Dow Chemicals & DuPont, Bayer & Monsanto) into three global majors and they will control ~ 65% of the global agrochemical market. With the rising R&D costs for most of the global companies, the consolidation will help them focus more on the core competencies apart from cost-cutting and improved synergies from a combined product portfolio. This could lead to increased outsourcing of opportunities for commercialisation of molecules and manufacturing for the proven industry players’.

‘China, one of the largest contributors to the global agrochemical Industry has been witnessing nationwide crackdown by Ministry of Environmental Protection. The government has worked tirelessly to phase out and replace high toxicity pesticides. Regulatory improvements have been made to achieve low toxicity and low residue. As a result, pesticides prices have remained at a low level in 2016. China’s 13th five-year plan for the pesticide industry (2016 – 2020) indicates of an industry consolidation being on the cards’.

‘There is a greater degree of comfort amongst the global innovators with respect to data protection in India, which not only enhances the number of innovative products launched in India but also gives a boost to the contract manufacturing industry in India. Several agrochemical molecules, worth ~USD 4 billion are going off-patent in the next three to four years. This provides significant opportunities for contract manufacturing and exports for the Indian companies’.

‘Our Company has longstanding relationship with more than 18 global innovators. We continue to further strengthen the relationships through strategic alliances & partnerships’.

‘As far as growth in exports is concerned, it is expected to be muted in the early part of the year as the outlook of global agrichem industry continues to be soft, which is expected to rebound from 2018. We have augmented the order book position and continue to significantly enhance our product pipeline in R&D for potential commercialistion’.

Some other key points

-

R&D expenditure of Rs.87.69 crore (3.68% of revenue) during FY17 as against Rs.81.51 crore (3.71% of revenue) during FY16 - primarily for the further development of new R&D center at Udaipur.

-

Cash flow from operations of Rs.336.80 crore generated during FY17 as against Rs.365.64 crore generated during FY16. Capex of Rs.141.79 crore during FY17 as against Rs.321.44 crore during FY16.

Disclosure: Invested

Crop acreage up 3.5% in last phase of kharif planting

Read more at:

http://economictimes.indiatimes.com/articleshow/60125836.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst

Hi Donald,

I was going through the complete thread on PI industries.

Not able to open the Q&A link of post no 511. If time permits you, could you please repost that.

Regards

Actively tracking, not invested

Updated the Link at post 511. Past management Q&As can be checked directly at www.valuepickr.com.

PI Industries Management Q&A Sep, 2013

we shall be careful to check such data on exchange. cartica still holds above 5% stake in PI. cartica even held a con-call with co mgmt. refer to links below.

http://www.bseindia.com/xml-data/corpfiling/AttachHis/28ee968a-abe7-406f-8456-25751ebd27b3.pdf

PI Industries

What is the annual report saying?

PI’s AR 2017 is giving lot of insight of what is going to come in. At the same time, it has left the future unquantified. But that is what the AR should do and that is what analysts should find out.

[wherever there are quotes, all italicised and colour changed fonts are mine]

Look at these sentences:

- A big macro promise or undertaking or whatever you might want to call:

at page 1 in the last para:

“…by leveraging our assimilated expertise and skills in the fine chemicals universe, thus going beyond agrochemicals. We are leading the innovation journey that will prove to be ahead of its time, in times to come.”

at page 31, last para:

“at PI Industries, Research and Development is one of our key strengths and is imperative to our business model. The recently inaugurated 1,25,000 square feet state-of-the-art R&D centre at Udaipur provides excellent infrastructure and lab facilities for our research…”

- On export prospects:

at pages 10 & 11 from the desk of Chairman, Narayan K Seshadri:

“a greater share of global contract research, synthesis and manufacturing opportunities are bound to head towards India”

Why? in management discussion

at page 31:

“Several agrochemical molecules, worth ~ USD 4 billion are going off-patent in the next three to four years. This provides significant opportunities for contract manufacturing and exports for the Indian companies”

and at page 29:

“The global agrochemical industry is currently going through a major consolidation phase. The recent M & A activities will consolidate 6 large companies (ChemChina & Syngenta, Dow Chemicals & DuPont, Bayer & Monsanto) into three global majors and they will control ~ 65% of the global agrochemical market.”

How does PI react to this?

at pages 10 & 11 from the desk of Chairman, Narayan K Seshadri:

“In order to give a further fillip to our future prospects, we are entering into strategic alliances with global agrichem majors.”

While I could not find any details about the incoming strategic alliances in any of the pages of annual report (hopefully, I haven’t slept over it), the latest conference call for the Q1Fy2018 has a fleeting answer. To a question on why other expenses were higher in that quarter, management replied that they had to pay fees to global consultants. Could it be to forge new alliances? Let us wait for the next annual report.

- On domestic prospects:

at pages 10 & 11 from the desk of Chairman, Narayan K Seshadri:

“Staying focused on existing patented/proprietary molecules in agrichem space, we are developing many new products/solutions for the Indian markets.

“We formed a joint venture with Mitsui Chemicals Agro Inc (MCAG) to provide registration services for their proprietary agrochemicals in India”

- On growth of the industry:

While all these statements are fine what are the estimates for growth of the industry?

at pages 12 & 13 of session with Managing Director:

“While domestic demand is expected to grow at 6.5% per annum, exports is pegged to grow at a much faster pace of 9% per annum during the same period.” (period from 2016 to 2020)

- What about the Indian macro for growth and how much did the industry grew in the past:

Few snippets before we go into that:

at page 27, the report has a chart of arable land. It is really scary that arable land has fallen from 163.6 Million hectare in 1985 to 156.3 Million hectare by 2015, while population was growing.

Most worrisome for India is exhibit 2, at page 28 which says that per capita availability of food grains has been flat in over 3 decades while the per capita income has increased 5.7 times.

Now, about the growth:

at page 28:

“The global agrochemical industry has slowed down in the past four years, owing to the lowering of crop prices”

at page 29, exhibit 3 states that global agrochem industry is witnessing a slowdown in 2015, after a multiyear growth from 2009 onwards.

But there is a silver lining at page 29: “…with leading indicators like the stock-to-use ratios for key crops standing closer to 10-year averages.”

Now where does it leave us with a company that is trading at ~ 23x historic TTM:

The Balance sheet is stronger today with a cash and cash equivalents (include investments) of ~ Rs.200 Crore. At the business level, major expansions are through, waiting to be harnessed and the core, the R&D lab is fully ready waiting to be commercially successful. The RoE and RoCE ratios are great while fixed asset turnover is commendable though the business in itself will have limitations on this ratio.

My guess is that if we assume that the company grows at industry level ie., on as-is-where-is condition, at max it can grow its business ~ 10%. Since the cake is not expanding, on the domestic front, the company needs to seize market share from competition by introducing new products. And that is possible by tie ups and increasing the distribution. On the export front, again it needs to enter into tie-ups with global majors to provide cost effective solutions.

What is worrisome is the dividend policy. While in 2013, the payout ratio was 13.2% it has fallen to 12% in 2017 (page 8 bottom chart).

What we need to watch out for the company, beyond the numbers, in every quarter is:

What are new tie-ups that are being announced both for domestic market and exports?

What is exports growth rate?

How are global food grain prices moving?

What are these consultants bringing to the table?

And of course, company need to raise the dividend pay out ratio to reasonably high level of 25%. Why am I particular about this? A high PE could be sustained with high RoE and that comes with a larger dividend pay out ratio when cash is not required for growth for the company.

I end this note with an impeccable statement from the management:

at page 2 in the penultimate para:

“Strong technical capabilities in the areas of research and development, manufacturing services, brand building, strong distribution presence in India and customer-connect initiatives help us chart a differentiated course for stakeholders’s value creation.”

Disclosure: I own this stock.

Generally large agro chemicals companies like Syngenta, Dow Chemicals, DuPont, Bayer, Monsanto, have their sourcing teams located in India and they are scouting companies like PI, Hikal etc for suitability of manufacturing of Patented “Agro Chemicals”

The consultancy money they might have paid for the due diligence which they are doing for starting the pharma Contract Manufacturing business.

Has anybody seen the price difference between ’ Nominee gold’ vs ’ Green label’( Generic version of Nominee gold by Insecticides India)?

10ml of Nominee gold is for Rs. 100

80ml of Green label is for Rs. 95

One can see the rates of the above products in the link below.

Understood that Nominee gold has a certain brand image, but dealers can bring in a lot of disruption in the sales of Nominee gold, by promoting ’ Green label’ being the same product ( generic version) at such low cost. And it’s not just Green label but also ‘Takila’ by Gharda Chemicals, which should be cost effective too, I presume. But PI management has not admitted to this challenge, which looks real to me. Need to dig deeper into Insecticides India to see how well accepted ’ Green label’ is and what revenue is it adding to the company, which implies that much share of Nominee gold( star brand of PI) been taken away. It does seem to be a cause of concern.

Insecticides India not only came up with an impressive Q1 FY 18, but is eyeing a 15-20% growth this fiscal.

This report is old but will put things in right perspective.

https://www.edelresearch.com/showreportpdf-32446/PI_INDUSTRIES_-_COMPANY_UPDATE-MAY-16-EDEL

According to the report Nominee gold market size is 300 CR.

So dropping the price 80-90% will crush the market.

I don’t think competitors are so keen to get a piece of the pie at any cost.

Disc: Invested

It’s not a belief or assumption that there’s a drastic price difference between Nominee gold and its generic version. It is a fact, a reality. Now how well is the generic version accepted needs to be studied. We can dig into Insecticides India reports to study that but as far as the other one, ‘Takila’ ( Gharda Chemicals), is concerned, I don’t know if a lot of reports will be available , as it’s not a listed company.

How can we find out the sales of the three new products ( one Maize herbicide and two Rice Fungicide) which PI has launched under the co-marketing agreement with BASF.

As per the conference call management has guided that the Contract Manufacturing Business will pickup in H2 of FY18

Interview with Mayank Singhal

I think there is some mistake in the price of Green Label at this site. For one, it is almost 10 times smaller than Nominee Gold. This article says that the price is Rs. 650 for 100 ml, which seems more believable

Hope it has nothing to do with Glyphosate or Round Up which are banned as cancer causing

Dear Donald,

Please share the Acrobat resources related to PI with me. email id is : shrenik three two one(all in numbers without space) at gmail.

Thank you in advance.

Not invested, actively tracking

Regards