Wonder whether there is any story behind the resignation of CFO and the last minute spike PI. http://www.bseindia.com/xml-data/corpfiling/AttachLive/8fea2ac1-96cc-4f94-8477-be1459dac1b9.pdf

1 Like

I believe todays gain was mainly because of the update from the company that the board will consider interim dividend in upcoming board meeting.

It could play out if the results support and on management commentary

Cartica decrease it’s Holding in PI by more than 2%. It’s currently holding 3.51%, down from 6.17% in quarter ended March’17.

Cartica still holds 5.01 percent. Please recheck

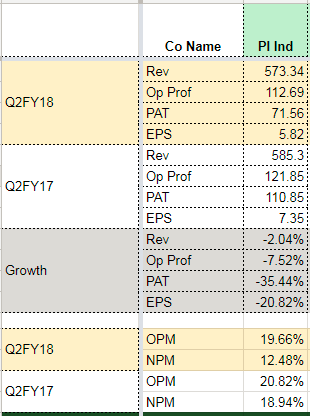

Q2 Results -Quite a poor show from PI. Awaiting management commentary.

-

Not correct. Cartica has only 3.51% as of now. Check the link.

http://www.moneycontrol.com/stocks/reports/pi-industries-disclosures-under-reg-292sebi-sast-regulations-2011-9602621.html -

Ugly results. Bought in April 2015. One of the wrong decisions to keep holding for so long…

http://www.moneycontrol.com/stocks/reports/pi-industries-unaudited-standalone-financial-results-forquarterhalf-year-ended-september-30-2017-9620121.html

Q2FY17 profit was bumped due to usage of 64 Cr inventory. Numbers seems to have got impacted due to below two factors QoQ,

- Increase in inventory of 13.18 Cr in Q2FY18 vs decrease in inventory of 63.77 Cr in Q2FY17

- Increase in tax payment: 24.32 Cr tax on 112.69 Cr Profit (~21.5%) in Q2FY18 vs 18.24 Cr tax on 121.85 Cr Profit (~15%) in Q2FY17

1 Like

Poor show again by PI. Waiting for management commentary. Management mentioned in Q4 FY17 concall that they are finalizing on pharma initiative and will have something by May. It’s two quarters already, and still no announcement.

Shouldn’t pharma pull down valuations in current market scenario.

Q2Fy18 Performance Highlights

- Domestic sales grew by 13%.

- Overall revenue growth of 3% primarily due to softness in export shipments following suppressed global demand.

- EBIDTA margin marginally lower due to product mix and softness in export demand.

- Q2 FY18 PAT was at Rs. 80 cr primarily impacted by a one-time tax adjustment.

- “Performance during the first half of the year was a result of projected softness in exports combined with uneven rainfall distribution in Kharif season and impact of GST changeover. However, pick up in rainfall distribution in the later half of season is a positive sign and this is expected to support domestic sales in H2. Further, we are expecting increase in export shipments in H2.” ~ Mr. Mayank Singhal

- The mid to long term outlook remains positive.

Source: http://www.bseindia.com/xml-data/corpfiling/AttachLive/5b8a48d2-9ec7-4a72-8072-6b4e44dc45e1.pdf

5 Likes

Q2FY18 conf call notes:

Overall:

Total revenue 3% increase, 13% growth in domestic

EBIDTA 122cr 21.7% margins (lower due to softness in exports)

PAT 80cr ( one time adjustment, effective tax rate was higher) 29% vs 21% in q1

annual tax rate 21-22%

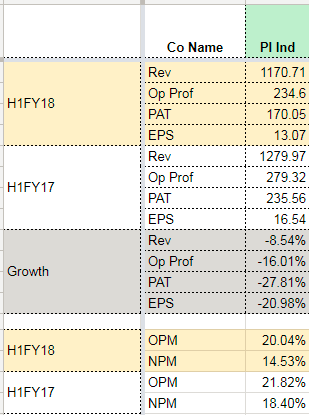

H1FY18 - sales 1114cr, degrowth of 6%

Full year margins will be similar to next year around 23%

200cr capex this year.

FY19 - 150cr-200cr as of now, can increase further based on possibilities

Domestic:

- portfolio of branded products, upcoming rabi season looks favourable

- 3 new products with BASF in rice segments fungicide, couple more products next year, products with sizeable opportunity - expecting double digit growth

- domestic revenue reported net of excise duty.

- nominee gold volume increase made up for price fall

- around 10% growth for full year

CSM

- Q2 302cr, H1 602cr vs 656cr last year (35% growth last year, upfronting), this year growth will backended in 2HFY18

- Overall 10% growth in annual basis in exports, 20% in 2H. orders/business tied, execution/ delievery pending, operating leverage benefit will be there

- trying widen the exposure with MNC, getting into adjacent chemistries like electronic chemicals, imaging chemicals etc

- set up best of kind R&D facility

- 3 products started on small scale in 1H

- second half commercializing 3 major products

- usually when a product is launched major revenue uptick in second/third year

- around 20 products totally commercialized till now

- before the end of this year will finalize on pharma, speciality chemicals foray

- CSM order book close to 1bn USD - this can all be done in the existing capacity

- global inventory levels (many of our products including) below threshold levels, offtake will start

- last 2-3 qtrs, getting into interesting products, R&D pipeline is better visibility for next 2-3 year

- chineese situation is uncertain

- can grow higher next year compared to 10% growth this year

- raw material,currency is pass through

Raw material - 25-30% coming from china, seeing price increase, passing it on

17 Likes

My notes from yesterday’s conference call on Q2FY18 results:

Domestic markets (Rs.258 crore sales in Q2FY18; 13% growth on y-o-y basis [adjusting for GST impact]):

-

Launched three products in the market in the first half of FY18 and plan to launch two more products in the near term. The new products which were launched (including two fungicide of BASF) were in an area where PI had limited/no presence. These new products are expected to pick up well in FY19 and FY20 and contribute significantly to company’s growth in domestic markets. The partnership with Mitsui and Kumiai is expected to augment our position further in the domestic market.

-

H1FY18 had uneven rainfall in few regions which affected Kharif sales. This along with GST de-stocking resulted in growth of low single digit for the company as well as industry in the domestic market in H1FY18. Although, acreages for vegetables increased, the acreages for rice and pulses declined during H1FY18. However, the indicators for Rabi season seems encouraging. Although, PI has normally seen pretty high sales during Kharif season, with the new launches and early indicators, the company might see some shift in pattern to Rabi season in current year. However, the management was not sure about continuity of the same going ahead. The management continues to maintain its earlier guidance of 10% growth in domestic segment for the full year FY18 implying higher growth rates during H2FY18 in the segment.

-

Impact of launch of generic versions of Nominee Gold: The launch of generic products have helped in expanding the market. Although, the company has taken price cuts to counter competition, there has been growth in volumes which has more than compensated for the price cuts. The volume growth for the molecule itself was 15%. Company will start selling the product manufactured in its own plans from FY19 onward (the technical is currently being imported from the innovator - Kumiai). The B2B business for Nominee Gold has also been slightly impacted due to genericisation.

-

On import restriction of technical and price control of agro-chemicals, management is of the view that although on cost basis, the overall contribution of agro-chemicals is small but it has highly critical for the crop. Thus government will taken any action consulting all the parties involved in it.

CSM (H1FY18 - Rs.602 crore vs Rs.656 crore during H1FY17)

-

Three products have been launched at small scale during H1FY18. The major revenue from these products is expected to come from H2FY18 which is expected to further pick up during FY19 and FY20.

-

Order book continues to remain strong at around USD 1 billion. The order book includes new molecules to be launched by the innovators as well as existing commercialized molecules. For newly launched molecules, volumes usually pick up from second and third year onward with registrations in new geographies. The company is seeing healthy inquiries and normally it takes 1 to 3 years for inquiries to convert into firm orders depending on the type, stage and life cycle of the molecules. 90% of the CSM order book consists of patented molecules. Maturity of a molecules can take around 15 - 20 year after launch. Current inquiries might results into sales in next 3 - 4 years. Raw material price and forex fluctuation are usually built up in our contracts and passed to the customers. Currently, our capacities are enough to serve the existing orders in hand. For new orders, we will have to build up capacities. The order book build up is based on estimates of the innovators. In case the innovator is not able to off-take a particular molecule, the company gets compensated with a new project/molecule.

-

H1FY17 had seen healthy growth of 35% on a y-o-y basis in the segment which along with global softening of agro-chemical industry resulted in de-growth in sales during H1FY18. However, second half is expected to improve and company continues to maintain its guidance of 10% for the full year FY18 implying growth of more than 20% during H2FY18. The company has orders in hand for H2FY18 and just execution in left depending on shipment of customers.

-

FY19 and FY20 are expected to see higher growth in the segment because of following reasons:

1.Global inventory levels in many of our products have fallen below threshold levels. Clear visibility of offtake in next few years

2. Over last two to three quarters, the company has been able to get interesting projects and products - R&D pipeline has increased along with higher inquiries.

3. China issues has impacted many companies including companies manufacturing agro-chemicals and intermediates for innovators (gave an example of blanket ban on chemical companies during winters). These might help us in getting new contracts.

4. Global consolidation among agro-chemical companies. -

Plan to spend capex of around Rs.200 crore for current year (Rs.60 crore already spent in H1) and around Rs.150 - 200 crore for FY19. The asset turns for CSM are around 2 to 3 times depending on product mix. With installation of some balancing equipment, we can do turnover of around USD 300 million in a year. Current capacity utilisation is around 70%. Phase IV of Jambusar is currently not being planned.

Other points

- PBILDT margins declined during H1FY18 by around 150 bps primarily on account of product mix and negative impact of operating leverage.

- Effective tax rate of 29% during Q1FYas compared to 18% in Q1FY18. Annual effective tax rate to be around 21 - 22%. FY19 and FY20 tax rate guidance at 22 - 25%.

- Top 5 products in domestic and CSM segment constantly change. The company currently has 18 products in the CSM product

- The receivables have increased a bit as on September 30, 2017 due to GST issues which are expected to be realised in the near term

14 Likes

I think we need to watch the performance for the next two quarters closely. While there is no reason to suspect the management, there are factors (global demand) that are not in company’s control. Management’s own admission - situation with Chinese is not very clear. As China shut down more plants, more business was expected to flow to India. While there is no doubt that in the long run company may come back to previous glory, opportunity cost in a scorching bull market is something to think about.

Disc - invested, will watch for 2 quarters and accompanying management summary.

1 Like

It has been interesting to observe reactions to various newsflow and data flow from various market participants esp in case of PI inds.

I think the key learning is that in the case of companies which the markets perceive as great growth companies or compounders or whatever you wish to call them, markets tend to give a lot of latitude even if the company suffers from a poor runrate for 2-3 quarters. There is the usual correction which is expected out of these nos or newsflows and at the end of these things on the first sign of light at the end of the tunnel, people begin lapping up the stock. Today’s move was probably in response to management commentary airing confidence about the future which re inforces the confidence of investors in the company. Thats not to say we should go out and buy tomorrow morning. Its always great to buy when stock movement is lacklustre.

Its always great to buy when stock movement is lacklustre.

If we look at things closely the numbers have not yet started falling in place but stock price has moved almost 30% from levels of 600 to 800 plus. Someone who followed the age old dictum of buying great companies having temporary problems would be definitely sitting pretty.

The saga of PI Inds and its stock price in the recent past is a great lesson for us investors to see how investors and stock prices behave to a slew of newsflow and data flow. Especially from the posts put up by different investors expressing their emotions like faith, disgust, lack of confidence in management etc

This thread is a great place to learn market psychology and how to benefit from it.

40 Likes

One thing I got from the concall that mgt said that, global agrochemicals industry degrewthis year about 8%and last year it grew 1% in such scenario Co did very well, this shows strength of the company and for the h2, in both exports and domestic markets mgt sounded very positive. Dis invested

Big FII sold significant holding in PI. Who bought it?

1 Like

Few months back too one famous PE sold n another baught . What I have realized after few years , PE firms like to book partial profits . So, though I track but don’t consider it deal maker or braker. Would be interesting to know who were transacting anyway

1 Like