Good move. Hope does not create two power centers with CEO in US and founding chairperson and MD in India, like Infy.

1 Like

Our usual valuepickr style analysis does not translate well to the IT industry for the following reasons in my opinion -

- The industry structure has and will be fragmented since IT Services is a very profitable business to run. I am yet to meet an IT Services company which makes losses, good companies squeeze out higher margins while bad companies squeeze out lower margins.

- Bad companies will continue to be in business, they do not fall away like in other industries.

- There are no economies of scale in such sectors where variable costs dominate, if business does not do well you fire some employees and keep the balance intact

- While IT companies will say that employees are their biggest assets fact is most employees are commodities and can be easily replaced. The same set of people will move from Infosys to TCS and vice versa

If one is looking at a company like Persistent which is hardly doing 3500 Cr sales from operations in a sector like IT Services where the addressable market size is > USD 1 Trn, on the face of it looks like the company can grow but it usually does not happen easily. For players at this scale (Persistent, L&T Infotech, Mindtree) one needs a high quality sales team which has connects with F500 in place and knows how to acquire and scale such customer accounts.

Market appears to valuing Persistent as a company that will never grow fast but is a decent investment since the IT Services business is not that difficult to run profitably. On the face of it market appears to be right. At best one can call Persistent a value play where one is swinging for a 30% spike at some point of time but this cannot be a long term hold till one us sure that market leading revenue growth can be achieved which can take the company to a revenue of USD 1 Bn in 4-5 years time.

Long story short unless one is able to figure out how hungry the sales team is and how hard they are being driven to acquire new customer logos, investment ideas like Persistent will end up being a value trap. For this one needs to speak to some account managers and sales folks at Persistent, also get a sense from them and management in terms of what is their approach to get in new customers and to mine existing customers. If you have 100 customers today where the revenue is USD 2-3 Mn, in 5 years time at least 4-5 of them need to become USD 10mn+ accounts and a lot of the other needs to scale to deliver USD 5mn.

Assessing the quality becomes a subjective activity that calls for a lot of primary work, arm chair excel work and reading annual reports will not help at all - all IT companies have smart marketing & PR folks who know how to write impressive sounding strategies and annual reports. It is not like a manufacturing company where a well articulated annual report stands out and can be used as a proxy to evaluate management thought process and vision.

We also need to ask ourselves if the business analysis and management quality analysis skills we have in place will suffice for the specific industry in question. In a business where intangibles matter more, a lot of primary work is needed compared to a brick and mortar business where a lot of things can be understood by looking at product, distribution channel and pricing. In IT Services & KPO these things do not reveal any meaningful information since the players look similar on these parameters.

33 Likes

Agree. Higher growth for smaller and niche players when industry has matured is going to be very rare phenomena. Just to set the context, Cognizant was founded 4 years after Persistent and now commands as Market cap of 55x

IT services is, in a way, a network effect business. The large will get larger because their incremental cost of operations is smaller than a smaller player. For example, if a $100 million company gets a $100 mn project, it needs to double itself (hire 70-80% of its staff strength, double its office space, increase bandwith etc etc), whereas if a $10 billion dollar gets the same project, it will not need to do much else. They can then focus completely on delivering to the client.

2 Likes

Highlights of the concall (source: capital market):

In FY 2019 $ revenue stood at $ 480.97 million, up 2.2%.

Indian Rupee revenue stood at Rs 3365.94 crore, up 11.0%.

FY 2019 PAT stood at Rs 351.68 crore, up 8.8%. PAT margin was 10.4% of revenue.

In Q4 USD revenue stood at US$ 118.30 Million, down 2.1% QoQ and growth of 1.2% YoY.

In Q4 revenue in Indian rupee stood at Rs 8,31.85 crore, down 3.7% QoQ and up 10.5% YoY.

In Q4 EBITDA stood at Rs 126.55 crore. EBITDA margins stood at 15.2% of revenue. EBITDA fell 25.7% QoQ and grew 13.9% YoY.

Q4 PAT stood at Rs 84.48 crore at 10.2% of revenue. It fell 7.9% on QoQ basis and grew 14.6% on yoy basis.

Q1 and Q3 are stronger and Q2 and Q4 are weaker.

Lower IP led revenue had adverse impact on margins at gross and EBITDA level. This was partially offset by cost optimization and better utilization of resources.

Christopher O’Connor who joined on February 25, 2019 has been appointed by the Board as the Chief Executive Officer and Additional Director (Executive Director) with immediate effect.

The management is excited with the new leadership team as it initiates next phase of growth.

Enterprises business continues to invest in building software defined businesses.

Its investments are aligned, and client interests remain strong as demonstrated by exciting new projects and opportunities.

Value of forward contracts hedged stands at $ 112 million at 73 per dollar.

It was a tough year and growth was less than anticipated.

Revenue from top customer declined which impacted the sales.

As of April 26, 2019, the company purchased 2,230,113 shares for a total value of Rs 1,42.17 crore, representing 63 per cent of the total buyback size. The board had approved a share buyback via open market route for Rs 225 crore with a maximum buyback price of Rs 750 per share.

The management thinks that it is currently in the position to hold on to margins.

The management wants to use the current cash for couple of quick acquisitions especially with the new management on board.

The company faces challenges in its services business in terms of growth rates.

In last 2 quarters percentage of offshore business has grown more than onsite business. Offshore trend is expected to continue in FY 2020 as well.

In FY 2019 multiple new projects were started which will deliver long-term revenue growth.

Digital business accounted for 24.4% of sales in Q4 against 22.9% qoq and 22.0% yoy.

Top customer accounted for 20.2% of sales against 26.3% in qoq and 25.7% yoy.

5 Likes

One of the most well written and lucidly explained post

There has been a dramatic rise in the stock price of Persistent in the last few days itself. I am a bit surprised that no one here is interested in this stock anymore

Disclaimer: invested since many years and the stock had barely moved up. Tested my patience, until the recent run up, which has been a very pleasant surprise.

6 Likes

Mr. Christopher O’Connor resigns from the position of

Executive Director and Chief Executive Officer of Persistent Systems Limited due to personal reasons!

Quote from Dr. Anand Deshpande, Chairman and Managing Director:

“We thank Chris for his contribution to Persistent over the last eighteen months. He helped in

building out certain capabilities and improved positioning to tap the opportunities, which

helped us achieve a good quarter under difficult circumstances. On behalf of the Board and

the Company, I wish Chris all the best in his future endeavors.”

Quote from Mr. Chris O’Connor:

“I have very much appreciated the opportunity to be part of Persistent. Over the past year

and a half, we have done significant work to strengthen our operational and offering

capabilities to better serve a rapidly expanding client base. At a personal level, I’ve held

multiple interests beyond technology, and the Pandemic, with its constraints on travel

contributing to improved personal health have given me ample time to appreciate those life’s

blessings. It’s with excitement that I look forward to those endeavors on the back of

Persistent’s best quarter ever. I wish the entire Persistent community well and wish everyone

the very best.”

1 Like

1.7 yrs is a short stint for top guy, reasons may be genuine but believe he was a catalyst for current performance- easily takes 2-3 Qtrs for new guy to show results and setup strategy execution.

Added perception of tailwinds to Midsize IT on Digital deal traction, run up has been quite good, technical and fundamental in sync.

Trimmed majority holding- would like to see how new leadership works out - services firm it matters a lot, runup has been quite decent as well.

1 Like

Agreed, if it was indeed the CEO who brought out a change in strategy and also executed it - though I personally have not looked into the details.

The wake up from slumber has been ‘quite’ phenomenal for this stock, in my view - and now I am really wondering what is next - it forms a significant portion of my portfolio.

However, the overall macro economic factors have been pushing IT sector up and this could help Persistent to ‘persist’ at ~1000 levels for some more time.

In the US, the energy sector seems to be now the new favorite and IT seems to be losing the preference. This could affect Persistent, Infosys, and others perhaps.

Persistent continues to deliver good results. Net profit is up 64% and the stock is now above 2100 Rs (and now all time high.)

I am truely surprised that the stock still has muscle to move up considering the the run started from 600 level.

1 Like

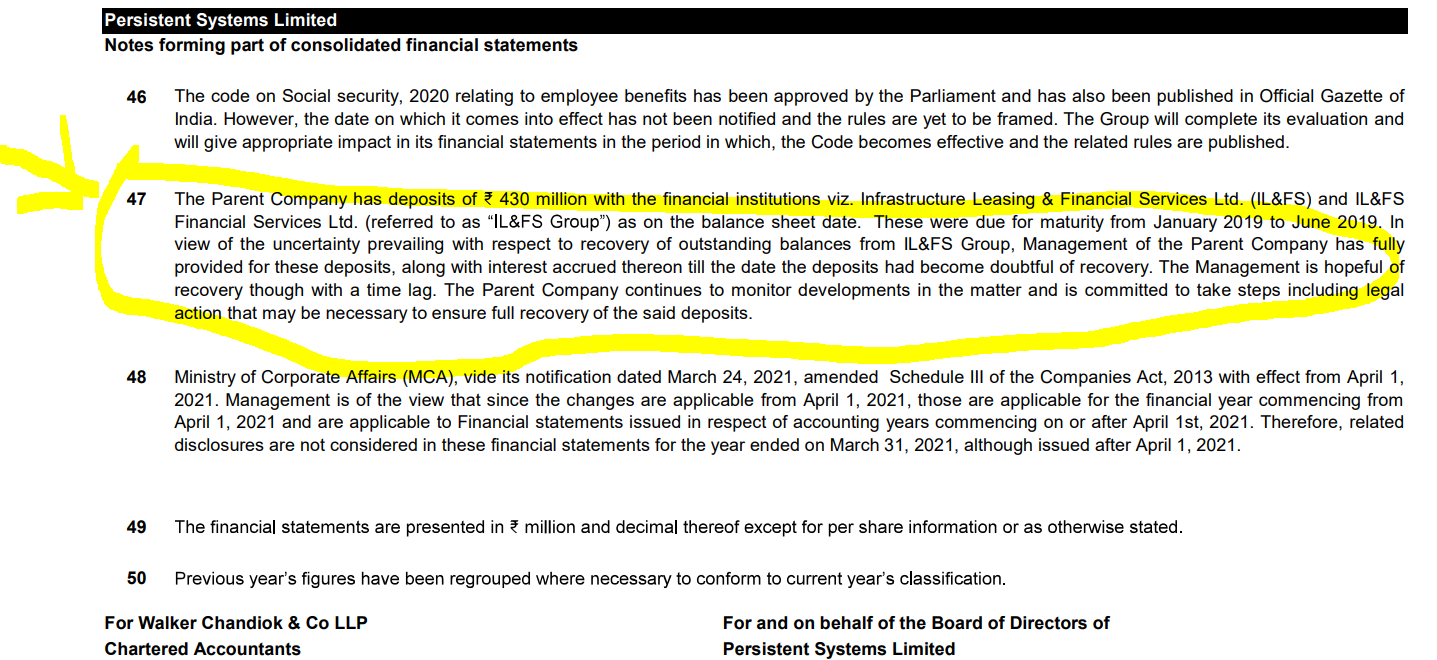

recovery is still not solved snip from latest AR

another negative

some contingencies liabilities

disc: invested

1 Like

I exited most of my holdings between 1800 and 2300 - which of course does look pretty cheap now that the stock is 2800+.

The momentum is very strong and maybe there are things which we retail investors do not know. Does anyone hear about a stock split coming up soon?

No idea about a stock split but the export oriented mid-cap IT cos seem to be on a roll. I also hold Sonata which has given similar out-performance…

news share

Certainly a nice gesture which will also help keep the attrition in check. But do employees really care more for long term equity valuation upside than the short term salary jumps?? Specially the new generation who dont even want to buy homes and are happy renting!

As an equity investor we must realize that employees are going to be more demanding to stay put, so even within IT, need to find firms which are more disruption oriented than the traditional IT firms which largely depend on employee strength growth! Employee strength growth is mainly useful for low end body shopping work which will not give super normal EPS growth. But the PE of midcap IT firms - Persistent and Mphasis have doubled in last 6 months, with PPFAS booking profits each month…

Invested and hence Biased and Cautious!

Another set of great results from Persistent, Revenues up 9.2% QoQ and 36 % YoY, and PAT up 46 % YoY !

They are growing revenues much faster than industry, and margins have expanded steadily. Growth coming from BFSI and healthcare , both sectors have potential for long growth ahead, at high margins.

However, product business is still soft. Attrition has gone up to 27 % which is a key risk in maintaining growth as well as quality.

Investor PPT : https://archives.nseindia.com/corporate/PERSISTENT_20012022200838_PSL_FactSheet_NSE.pdf

Audited results: https://archives.nseindia.com/corporate/PERSISTENT_21012022002407_PSL_AuditedFinancialStatements_20012022.pdf

Disc: Invested, and Persistent is now the single largest holding in my Portfolio. Not selling yet, but still a bit uncomfortable with valuations, but the recent correction in price, and good quarterly numbers have made it a more palatable PE of ~ 50.

2 Likes

Impressive results from Mid cap IT companies. Persistent Sys management guides for margin improvement going ahead whereas many analyst believe there would be margin pressure and they have been able to renegotiate better pricing with clients.

Disc - Invested

The acquisition of Data Glove Assets is expected to dilute EBIT margin by 75 basis points in FY23, said Citi maintaining its ‘sell’ call on the company’s stock.