Q3 Summary (source: capital market)

IT teams continue to leverage its Software 4.0 offering for incremental and iterative development.

Enterprises are integrating applications through APIs by bringing internal data, external data and events together, building insights that are actionable.

Machine Learning has become mainstream as customers move beyond dashboards to task centric actionable insights that are embedding Intelligence in applications.

Businesses continue to march on their journey to become software driven which is helping the company win customers.

Riding high on the splendid response from last year’s Smart India Hackathon, the third edition has been launched, with the finale for the Software edition slated for March 2019.

The management hopes this movement continues to provide students a platform to harness the true potential of technology for nation-building.

The Board of Director approved buy-back of equity shares under open market route for an aggregate amount not exceeding Rs 225 crore (10% of net worth) at a maximum buy-back price not exceeding Rs 750 per share.

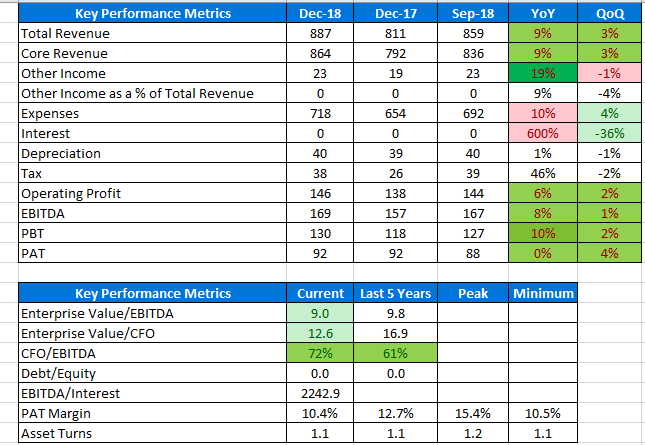

Sequentially Persistent Systems posted 3.4% growth in consolidated sales to Rs 864.25 crore for the quarter ended December 2018. On yoy basis it grew 9.1%.

EBITDA rose 18.6% qoq and 23.9% yoy to Rs 170.32 crore.

PBT rose 2.1% qoq and 10.2% yoy to Rs 129.52 crore.

PAT rose 4.1% qoq and 0.1% yoy to Rs 91.72 crore.

Quarter $ Revenues stood at $ 120.84 Million, up 2.2% QoQ and a decrease of 1.4% YoY.

Nine months $ revenue rose 2.6% to $ 362.67 million.

Nine months Rupee revenue rose 11.1% to Rs 2534.09 crore.

Nine months Rupee EBITDA rose 26.9% to Rs 453.99 crore.

Nine months Rupee PBT rose 13.3% to Rs 375.03 crore.

Nine months Rupee PAT rose 7.13% to Rs 267.21 crore.

In the last two years, its focus on digital has helped it build capabilities in key technology areas and experience in helping customers as they transform to being software driven businesses.

Looking ahead, the company is doubling down on three industry markets – Financial Services, Healthcare & Life Sciences and Industrial IoT in addition to its strong presence in Software and Technology.

The management is delighted by the grand success of the Software Edition of Smart India Hackathon 2018 and look forward to innovative solutions at the Hardware Edition in June this year.

Linear revenue grew 3.5% and IP revenue was flat in 9 months.

Linear revenue grew but IP led revenue fell in Q3 on qoq basis.

Staff cost was lower reflecting offshoring of certain projects.

Doubtful debt were higher by 10 million as they had crossed 80 days.

25 new clients in digital business out of which many were marquee clients.

Treasury income was Rs 225 million against Rs 195 million helped by m2m gain on MF as interest rates fell during the quarter.

It has Rs 43 crore as corporate FDs in IL&FS. It will take 9 months to address the liquidity situation. Deposits were due in Jan to June 2019. At this stage the company is not in a position to ascertauin the amount of hit or hair cut it has to take regarding the same. It will update going forward as and when possible.

It spent Rs 26 crore in nine months on capex.

Cash in books were Rs 1501 crore.

Value of forward contracts hedged were $ 120 million at Rs 71.54 per dollar.

IBM reseller business were less than expected in IP led revenues. It will move in next quarter and so the management expects to get it in this FY.

It expects to aggressively hire in the March 2019 quarter as well.

It is very close to making offer to the person identified to take over as CEO of the company.

Effective tax rate would be in the range of 28-29% in Q4.

Services revenues accounted for 75% of revenues in q3 against 74.4% qoq and 72.6% yoy.

IP led revenues accounted for 25% of revenues in q3 against 25.6% qoq and 27.4% yoy.

Digital revenues accounted for 22.9% of revenues in q3 against 22.0% qoq and 21.4% yoy.

Multiple new projects started will deliver long-term revenue growth.

It will continue to invest in new technologies and in enhancing domain and consulting skills in its customers’ geography.

Digital business grew 6.5% qoq.

The management sees good traction in digital business in healthcare vertical in the US.

The management is very confident of maintaining margins. As it sees steady growth in offshore opportunities, Offshore numbers will continue to go up and onsite will continue to go down. Thus, it will either increase or maintain margins going forward.

The company is focusing on cost management.

Steps taken due to softness in business in last two quarters have started giving yields. The management is confident of the momentum to continue.

Headwinds expected in next 2 quarter are salary for hard-to-get-skills.

There are opportunities to increase the margins at the EBITDA level and PBT level. However, the management refused to give range guidance.

The IoT market has been under lots of pressure as companies like GE have been seen backpedaling. However, the business is expected to be stable for the company.

The management is disappointed that there will not be a double-digit growth rate in the current year but hopefully it expects to get there in the next FY as the business has enough things going on. However, only by next quarter’s concall it will be able to give a clear picture on FY 2020.

Current organic growth is not dependent on the joining of the new CEO.

The management feels that there is no reason why digital business should not grow at 25-30% yoy.

. Nevertheless, I think subdued quarter results and IL&FS exposure have taken a big beating on stock. With 350-400 cr of annual cashflow n a conservative single digit possible growth in digital in sectors like. Healthcare n Financial, company is available at 4300 market cap n if m not wrong ,1000 cr+ cash . Though, mgmt has been accepting underperformance in quarterly concalls n inability to convert pre sales into deals , they spoke about new hiring to be done n without justifying anything, focus on action rather than reasons . So, I think though to drive sales , they might increased SGA cost, at this valuation lot of downsides look factored in . Disc: had completely exited my 2016 position in feb-march 2018. Have taken a fresh 2% position in last 2 weeks post IL&FS price crash

. Nevertheless, I think subdued quarter results and IL&FS exposure have taken a big beating on stock. With 350-400 cr of annual cashflow n a conservative single digit possible growth in digital in sectors like. Healthcare n Financial, company is available at 4300 market cap n if m not wrong ,1000 cr+ cash . Though, mgmt has been accepting underperformance in quarterly concalls n inability to convert pre sales into deals , they spoke about new hiring to be done n without justifying anything, focus on action rather than reasons . So, I think though to drive sales , they might increased SGA cost, at this valuation lot of downsides look factored in . Disc: had completely exited my 2016 position in feb-march 2018. Have taken a fresh 2% position in last 2 weeks post IL&FS price crash