Debt equity is not related to market capitalisation further Bank have protected the debt at the cost of equity holders which is a prudent measure(for Bankers). The cash if any not leaving the company for share buy back will be used for debt servicing.

1 Like

Team,

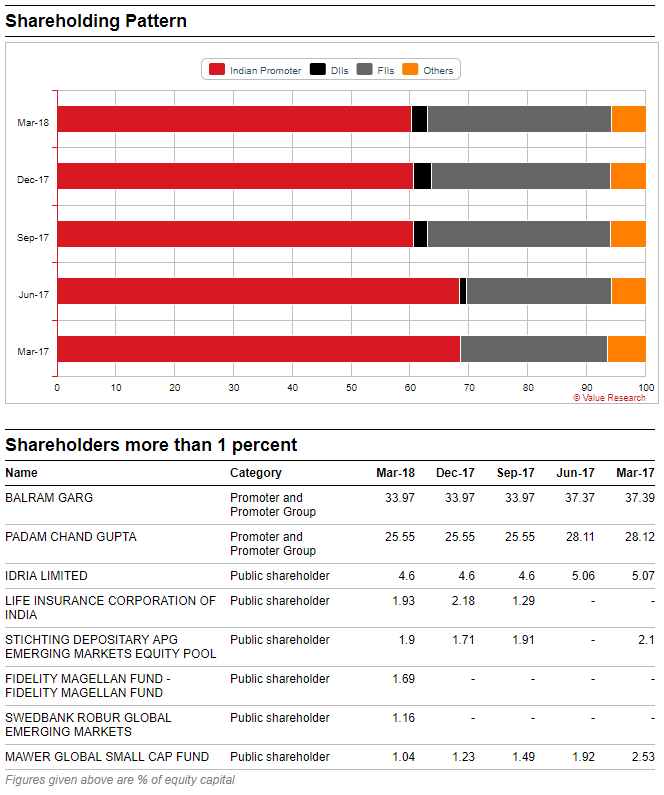

Can anyone help with throwing light on the Promotors holdings in last 6 months ?

They yet to share the SHP for June-2018. As per SAST updates, no change in promoters holding. But not sure if they comeup with surprises in that too.

1 Like

Thanks.

Any guardrails on when the SHP is expected ?

Can the following info. from valueresearch be considered authentic for upto March-18 ?

It’s authentic indeed! You can check for more details in one of the exchanges (BSE/NSE).

1 Like

They have to justify soon on media otherwise many investors will be ruined.

Hi, I am new to Financial Statement analysis. Kindly refer to the table of PCJ results (Annual trends tab) as listed on BSE. https://www.bseindia.com/stock-share-price/stockreach_financials.aspx?scripcode=534809&expandable=0 Now, what I can see is the annual results of last 5 years - March 14 to March 18. For the years 2014 to 2016 the PBDT is calculated as follows. PBDT = Total Income - Expenditure - Interest. (For example: for March 2016, PBDT = 7308.63 - 6532.70 - 214.65 = 561.28) . This seems correct to me. However, for the years 2017 and 2018 the same row PBDT is calculated as PBDT = Total Income - Expenditure and the Interest amount is not reduced from the profits. (For example: for March 2018, PBDT = 9587.93 - 8797.30 = 790.63 This totally ignores the interest cost of 301.29 Cr). What is it that I am missing? Thanks, Regards,

(1) I came across this discrepancy while calculating % OPM in another forum. There is too much noise on that site. I hope I will get the answer here.

(2) I have 1500 shares of PCJ at 130 bought last month as the IV was very high. Now, I have no open options positions.

It is right as of March 2018. The SHP for July 2018 is yet to be disclosed. Still, this is not the latest info. I am sure that you are aware of the gifting controversy. The details related to this gifting are captured in the postal Ballot Notice (page 6/11) and I am reproducing the same here.

Promoter Padam Chand Gupta gifted 1,03,00,000 (1 Crore 3 Lac) shares in 6 tranches from April 2nd to April 20th. Thus his holdings in the company are now 9,04,43,600 or 22.93% This number is 25.55% as per your slide. The recipient of the gift is not mentioned in the notice but in the conf call (if I mistake not) it was mentioned that it is given to his daughter-in-law. Questions about logic behind gifting in tranches were not answered. It was suggested by the person who raised this question that if the shares are sold in less than 0.5% tranches by non-promoter then it need not be reported. I am not sure if that is indeed the act/rule but this was not contested by the management in conf call. Hence all this controversy of this not being a gift but sell by the promoter. Please note these changes to SHP. Anxiously waiting for July SHP. regards, Disclaimer: Holding 1500 shares at 130.

3 Likes

I had earlier noted down the “gifting” controversy. This gifting is not new to them. They did it in early and mid 2017 also to Shivani Gupta (PC Chands Daughter-in-law). She has been selling some amount. That is why the recent controversy is so surprising to me. And the gifting has only been happening in PC Chands family not Gargs family.

See details in this link:

1 Like

The promotor selling needs to be reported to exchange and at times taken by hate holders as negatively and share price gets corrected.Therefore this method is employed by some promoters which effectively hides their identity as sellers

2 Likes

Thanks LTInvestor for bringing out the past gifts. Now, it is really surprising why so much negative reaction to this gifting. Hope it is all creation of some bear cartel and not something really bad. I am holding equity and if the balance sheet is good, debt is cleared, and new stores are mostly franchisee based then the bear cartel will have to end its operations soon. Since right now I am not in FnO I am not under pressure and can wait for a few months. thanks, regards,

I think we now have sufficient information one after the other happening in PCJ to make an educated guess of how deep the hole is. Vakrangee including PCJ as partner, then buying a whole bunch of shares. Stock raising 4 fold for no reason. Promoters offloading a bunch of shares gift or otherwise. Directors with shady background and no relevant experience to justify their appointment, buyback fiasco. merely looking at the number of shares traded and wild swing in prices over the last few months. Gitanjali stores being converted to PCJ stores. If someone is still holding this, please recheck your conviction.

2 Likes

@SlownSteady as long as they are playing with the share price I am okay. Because then I am sure the downtrend will stop somewhere and convert itself in an uptrend whenever they want to. My worry is if they are playing with balance sheet and in general all sorts of fundamentals presented to public share holders. Like say cash on balance sheet, trade receivables etc. In that case there is no end to this downtrend and no hope of an uptrend. Price manipulation happens in the bluest of the blue chips so I can ignore that. As per balance sheet PCJ is a clear buy. I am hesitating because I am not sure of the promoters and it is a bad idea to average down. regards,

1 Like

Interestingly when the gifting started in 2017 March no one cared. Rather it was at Rs. 200 then and made its mad dash to 600 from there. I was not on this board then but would like to go back and see if any one raised any questions. This fall because of gifting looks very manipulated as things had started 1 year back.

I am invested mainly because of no promoter pledging and manageable debt. All Indian companies get into trouble due to promoter pledging and leveraged balance sheet. If there are sales and debt manageable, EPS takes of itself over medium term.

Disc: Invested. Started trading FNO at about 180 (during last bout of volatility) and now invested in cash at 130, though averaging for earlier FNO profit maybe about 110.

@neopandit . Buy a PE at 50, will help for results season.

1 Like

It’s not only gifting issue but also it’s link with vakrangee

From what I gather, Buyback did not seem such a good idea for the Company financials. So, its cancellation should be a good thing? For the company and investors?

With a 12% (or lower) buyback ratio, trying to factor the buyback premium into the price was, for the large part, just bad maths anyway.

Discl: 3% stake in PF, was 12%, invested since 1st week of May 2018, sold off in 1st week of July. Share price seemed like a bad joke with the incredibly high volumes, more like a gambling counter.

@vikas_sinha Yes, cancellation of buyback is a good thing because for the amount being spent, not enough shares would have got extinguished. So, from whatever I calculated it would have reduced the EV per share for the remaining shareholders. A disclaimer here I am very new to these calculations and have no education in it. I went with what I felt logical way of computing.

Having said that and again IMPO the current down fall is not because of fundamentals of the sector, or the company. I have two possible explanations for the current fall in price.

(1) Since the downfall is across the market with few exceptions, one explanation is that certain market participants are forced to liquidate their positions regardless of what they are liquidating and at what price. These participants are smaller FPIs (carry trades getting reversed), LIC (to fund purchase of junk like IDBI Bank and Air India), and Govt of India (mostly to meet divestment targets and contain fiscal and current a/c deficit).

(2) Company specific problem is trust. All the numbers in public domain are good. But no one is believing them. The management is doing precious little to address the problem. This gives birth to the suspicion that management is hand in glove with or is in itself the bear cartel. For example, falling promoter share holding (from 68% to 57% over the year) is a cause of concern and fertile ground for rumours then the management should have declared the latest share holding pattern by now. Almost 900 companies have done this by now. Waiting till the stipulated 21st day makes life easy for bears. Company gets weekly update of all the share holders so this is quite easy. A little difficult but not impossible was to publish the Q1 results by now. That would have quashed the rumours about company not having cash in banks (although March results show 1000Cr plus) but company has not even announced when it is going to declare the results. Buyback cancelled was a good idea but who on Earth will buy the clarification that bankers were “appreciative of the company reducing exposure to banks”?? So the suspicion is not without a reason.

As I wrote earlier I am okay if the management is playing with the price (lesser evil). I hope they are not playing with the financial statements. I hold 1500 shares at average of 130 There are no FnO positions. regards,

Check treehouse, no promoter pledge, no debt. The only point I am highlighting is only these two may not guarantee that it is totally safe. Treehouse had enough red flags to highlight without debt and pledge also it was a trap. So, a detailed analysis of PC AR may highlight. Note: This has nothing to do with PC Jeweller as I have never studied and hence would not like to make any positive or negative comment without a reason

1 Like

So one more fund exits today. Wellington Mgmt Co sold around 37.5 lac shares @ Rs. 85.43/share.