there was a time when gitanjali owned the highest no of stores may be around some 5000 thousand globally but now as the company is not functioning and most of their store was franchised so these franchisee are now moving to other brands which may be a good step for pcj given franchisee local connections

gitanjali gems cheated their franchisees(by overvaluing the inventory provided to franchisee), many franchisees of gitanjali gems filed complaints against the company, now these franchisees are moving to other brands

1 Like

tanishq also operates by taking gold on lease, under the gold on lease scheme price of gold are fixed on day of sell is made to the customer so it provides a natural hedge against the gold price fluctuation and this time period for which the gold is held is called credit period and company has to pay a 3% annual interest rate for the entire credit period

2 Likes

Thanks for explaining the credit period and the concept of how the Gold price fluctuation is hedged. Currently Silver is 1% down on MCX and Gold is down too. I was not sure whether price of Gold/ Silver affects the jewellers in some way and if yes, how? Now it is clear that at a hedging cost of 3% p.a. they are immune to the price fluctuations. Under such consideration I believe a lower price of Gold helps increase volumes and the interest costs will reduce drastically as the turn around time is short. Please correct me if my understanding is wrong. Thanks, Regards,

SadaBahar?

According to an article in Hindu,

“Demand for gold jewellery has been stagnating in recent years, according to World Gold Council data. While 2,043 tonnes of gold was consumed by jewellery makers in 2010, that declined to 1,988 tonnes by 2016. Gold jewellery demand peaked in 2013 as consumers used the fall in gold prices to buy in. But all the major gold-consuming countries, including China, India, West Asian countries and the Americas, have seen gold jewellery consumption decline after peaking in 2013.”

Even in India people now NOT buying gold as investment but only for use/ornaments. This is change in Indian culture also.

@pkk123

Thanks for the numbers.

My remark was of qualitative nature.

From your numbers I see -

(1) 2043 - 1988 = 55 Tons. That is 55 / 2043 = 2.75%

(2) 2016 -2010 = 6 years

(3) So, less than 3% decrease over 6 years.

(4) That decline when the World moved from financial chaos to false sense of security and stability is at least as good as constant (SadaBahar) to me.

@hnk_so

(1) For their investments smart, educated people moved from Physical Gold to paper Gold (in various forms). Good luck to them.

(2) I like that trend as there is no crowding / competition for me in buying physical Gold.

regards,

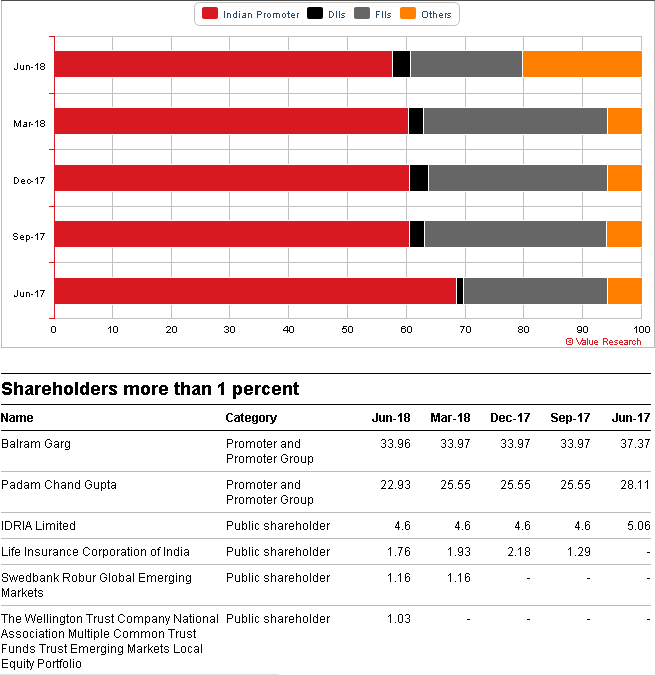

Shareholding is out. Where is the problem ? I think we should lap it up.

https://www.bseindia.com/corporates/ann.aspx?scrip=534809&dur=A&expandable=0

Retail share holding seems to be up by nearly 10%. But things must have changed after the cancellation of buyback. Has the retail holding increased even further ? Or, the retail sold in panic and informed ones lapped up ?

Compare with earlier qtr - promoters and MF holding reduced and please note that this is up to Jun 2018 and does not reflect July 2018.

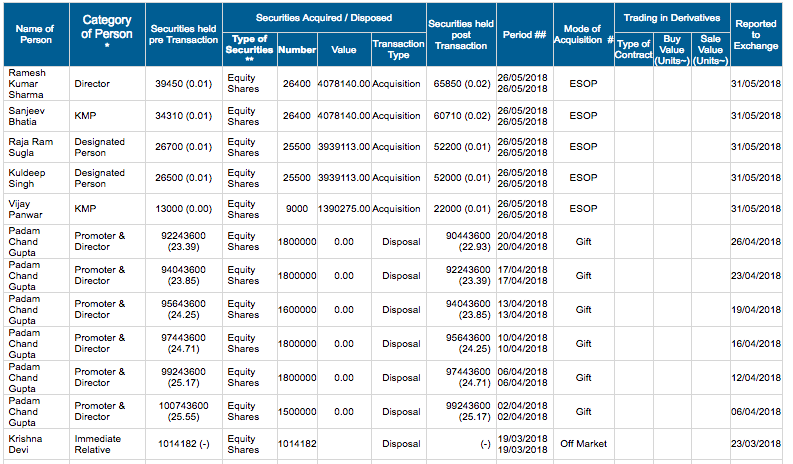

Why did promoters sold stocks after declaring buyback? Did they utilize the opportunity and fooled retail shareholders?

The promoters didn’t “sell”, they “gifted” to “unknown” relative, If I’m not wrong, the recipient is the promoter’s daughter-in-law, in all the probable that gift was encashed. That’s how everything unfolded.

I see following entities completely exited:

- Fidelity

- Mawer Investment

- Stichting depositories

New entrant:

- The wellington trust (they invested in some of the prominent names: Glenmark, TTK Prestige, also has controversial names: PCJ, Vakrangee)

No change: IDRIA Ltd, LIC

From the public and owner shareholding, there appears to be a high probability that at least a major part, or all the gift, given to the daughter in law were sold, as her name does not appear in the list of those holding more than 1 % shares.

[quote=“manivannan.g, post:639, topic:297”]

New entrant wellington trust sold recently in july and may be retailers are also selling in panic in july.

Could you pls point me to the source ? In both NSE/BSE bulk deals, I couldn’t see wellington name.

1 Like

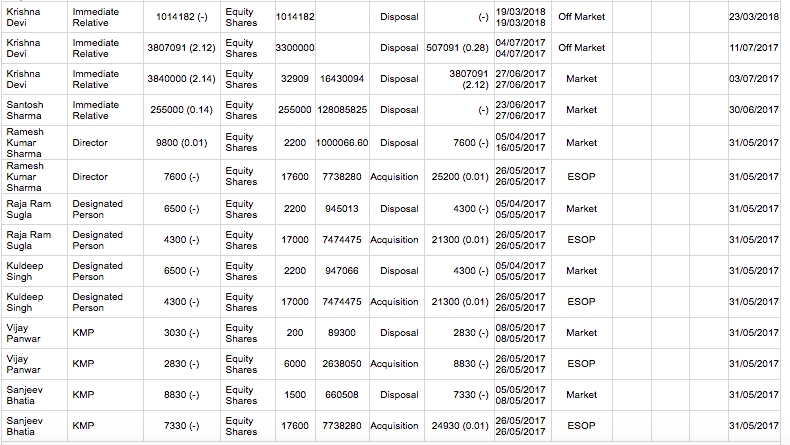

This “relative-gift-disposal” saga is not something new for PCJ. The relatives selling in off-market too ?!! Definitely in the name of relative promoters did.

Maybe biased as I am invested, but really do not see anything negative in the shareholding report. Disposal by promoters of 1.05cr which has already been disclosed. No other disposals since then.

Most importantly, no pledging. If the cash on B/S is actually false, which in effect means the sales are also fake, the company would have had to start pledging shares to post collateral for debt. Much of the debt is ST for WC, which would have been called by bankers by now.

My sense is fundamentally nothing wrong. Lots of insider trading but nothing much on fundamentals.

3 Likes

I am happy to see that the major sellers are FPIs. They have their own carry trades reversed so they must sell. Their selling can take the price down without any doubts on the management or biz. Your analysis on the pledging logic is on the spot - good insight. thanks, regards,

Exactly, DIIs is up. Yes, FIIs is down from 30% to 20%, as expected with Fidelitiy etc news. Promoter is reduced about 2% indeed. Retail share increases by 2x from, 6% to 20%.

Thanks @sameer80 for pointing out Well mgmt as reported in bulk deals is same as Wellington on SHP … I knew about Well bulk deal the other day but still could not connect it when I saw this new entrant. Thanks, regards,