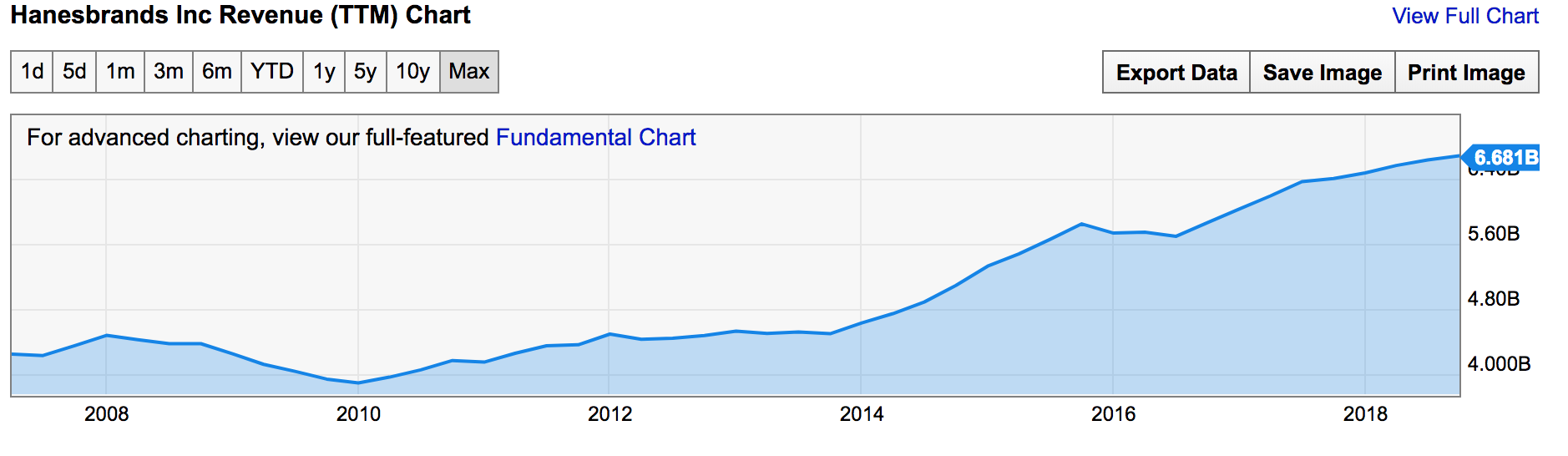

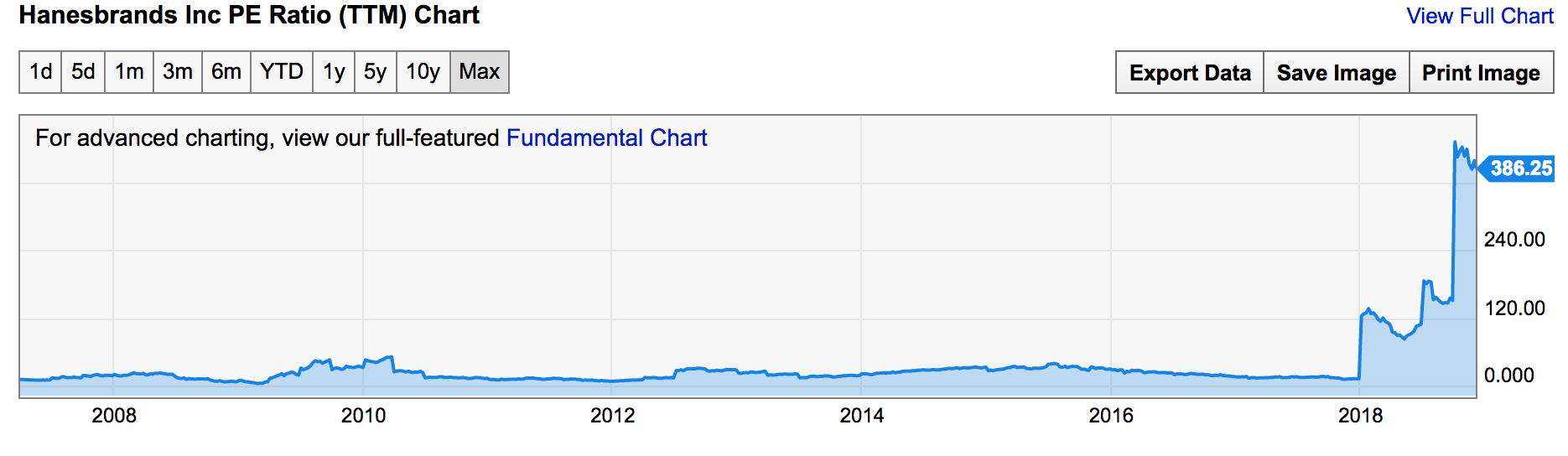

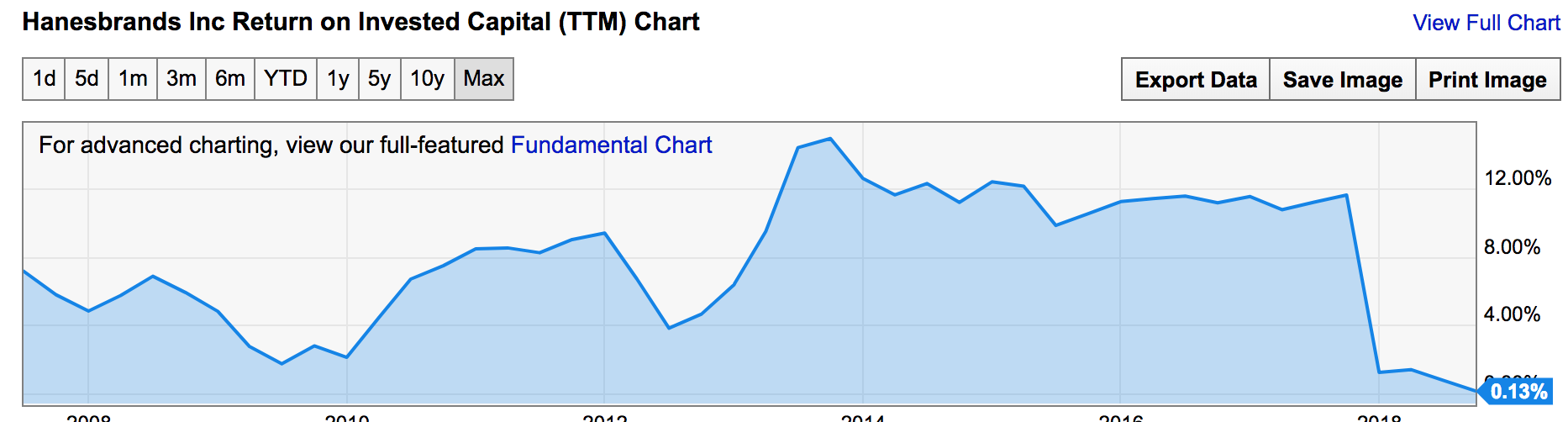

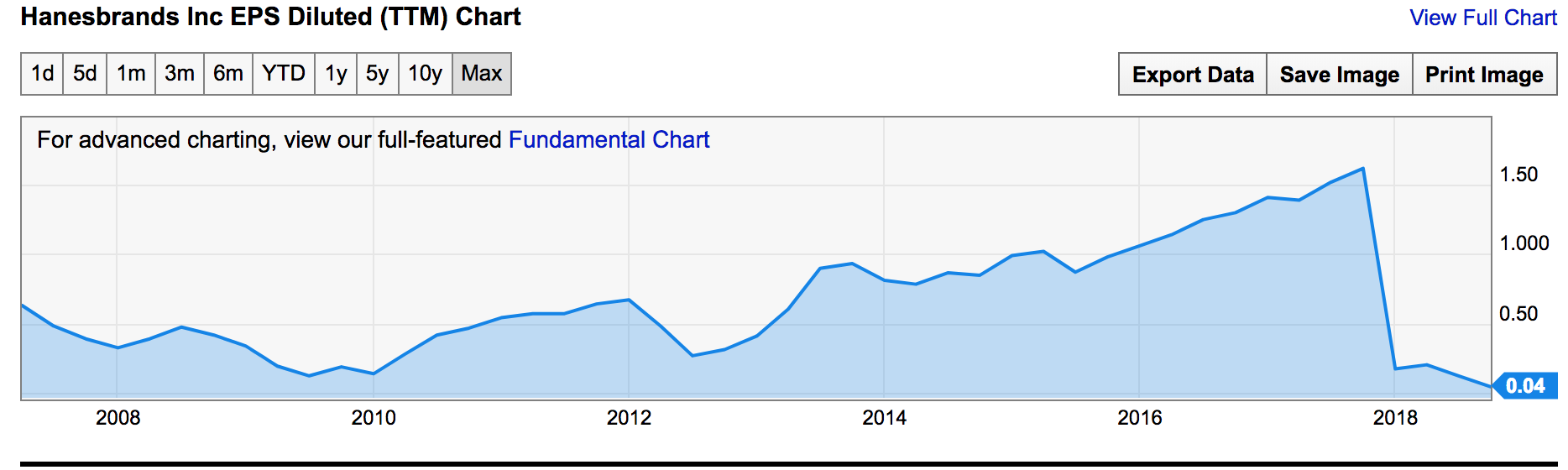

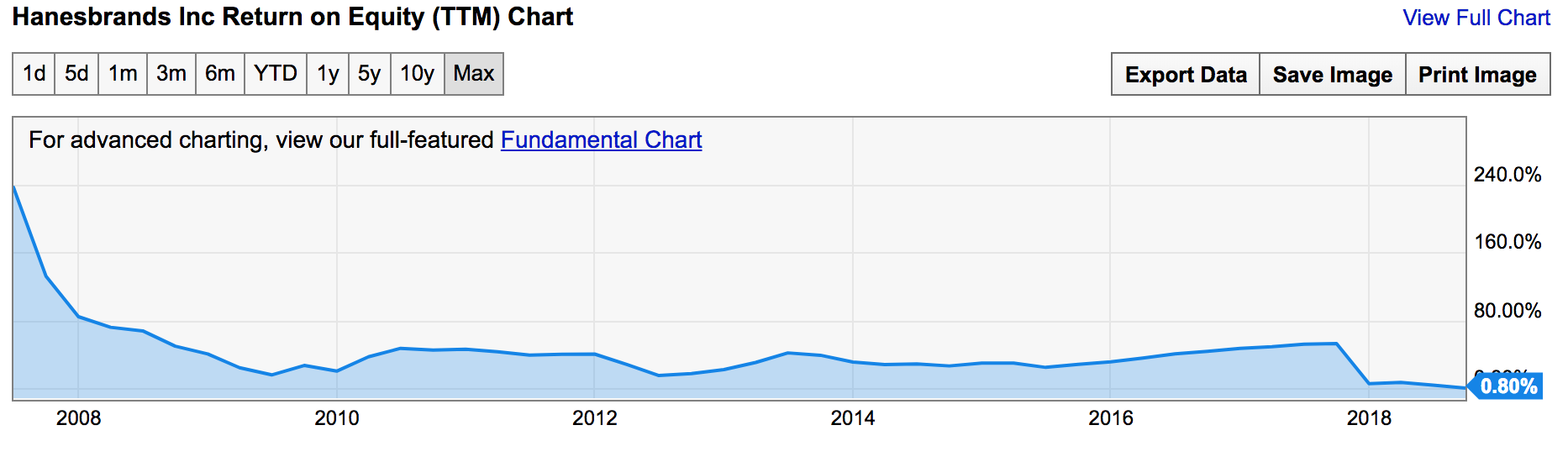

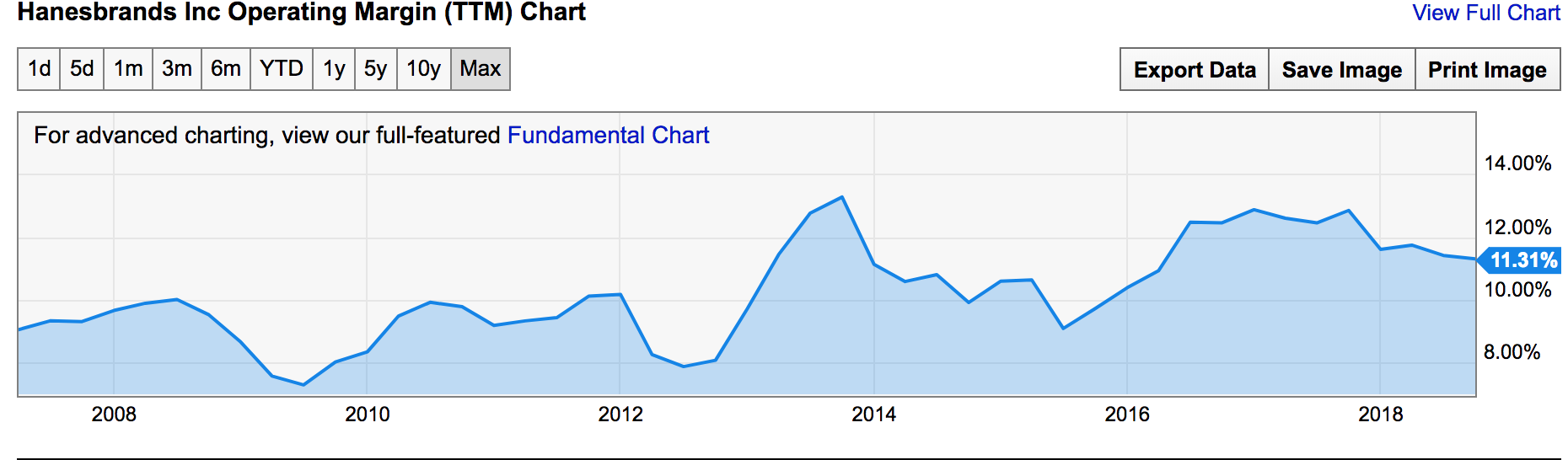

The companies are in entirely different orbits , and the target markets are in different orbits. Amit Jeswani’s comparison seems like apples to oranges to me. Basically Hanes has lost market share , and also return rations deteriorated as it grew to this size, it lost its moat or ‘aspirational’ status. My takes is - Page is young and future cant be foretold looking at hanes terminal value, as the ‘terminal’ market size for Page is definitely 3 times that of the USA.

Disclosure : not invested in page any more.

Further disclosure is I do trade in page from time to time. I moved out as an investment is because I m trying to move to financials n tech etc, which is just the overall portfolio level direction.

much was discussed on the thread about the business of page industries. now the price has corrected to desirable levels according to me. i might even go and replace it with last few investments picks of mine…at the cost of sounding repetitive …such corrections seldom come in such businesses and one should try and latch on.

disc: planning to invest at current levels and add on declines

Page Industries, Mindtree: Market grapevine has it that an offshore fund, which shares the name of an ancient university, is offloading some of the stocks that it has held for a while. The talk is that the fund has been selling Page Industries, Mindtree, Supreme Industries, V-Guard and Kewal Kiran Clothing.

@hitesh2710, have always learnt a lot from your post, sir . PE wise page industries is very high , however has corrected quite a bit considering its high quality . Dcf analysis has always made page look overvalued to me but reading many post here , it seems dcf analysis does not work here and am confused whether to invest in page at this point or not . Request your guidance aa to what price point can one target for such companies and how to value them ? I already missed investing in page in 2014. Would like to express my gratitude for learning a lot from sharing your experiences. @richdreamz, have got a lot of investment knowledge from your post too . Thanks for that . Seek your views too on page industries currently

Also , is the growth trajectory still on ?

The announced yet another special dividend. What could be the reason for yet another special dividend?

This year 303 dividend in 9 months ( 41+41+110+41+70)

Page has been increasing outsourcing for last few quarters. So capex requirements have gone down. I think management realized that there was excess cash in balance sheet and lightening it by paying out extra dividends.

In today’s zee business news channel , they mentioned some adverse report of Kotak on page industry . They mentioned some adverse accounting . Does any one knows about it ?

Disclosure: I hold Page but I’m not writing this to support my conviction but to a) convey that there are no issues with the results as such - to drive away the devil 2) quell unnecessary allegations of corporate governance issues raised on management in social media. 3) To pity the quality of the analysts in our brokerage houses (the same brokerage has buy calls on very low infrastructure, material building low quality companies just because they are at very low valuations, does not matter if the balance sheet is junk or not!).

The analysts who found “Devil in the details” in page industries Q3 FY19 results could not find “Angel in the details” in Q2 FY19 results? If Q3 results are not as good then Q2 results are not as bad as well!

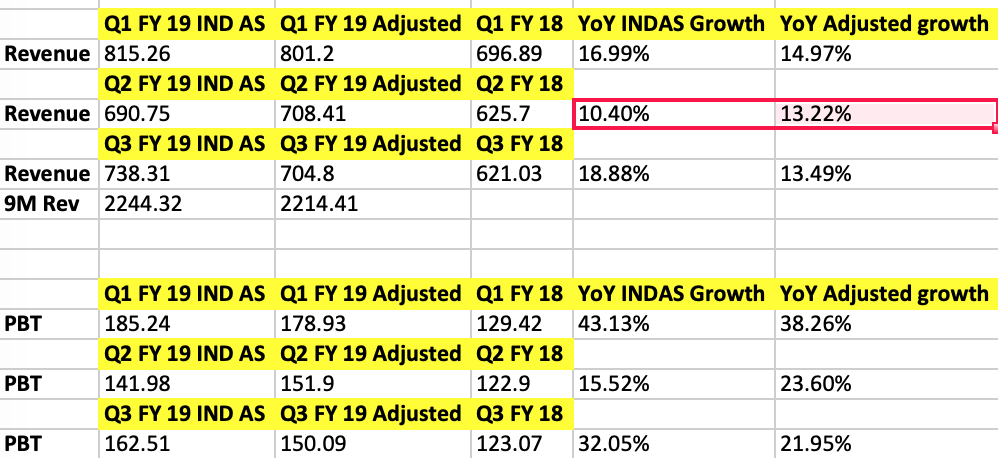

Re-worked as per notes provided in Q1, Q2, Q3 results and details attached in the screenshot. Though a bit lower revenue growth as per Page industries standards, the results are much better than the most of FMCG pack with exceptions. Consistent, predictable and gorgeously consistent margins even in these tough times. Irrespective of raw material prices, Page maintains consistent margins.

So, the Q3 results revenue growth is not 18% but 14%. Similarly, the Q2 revenue growth is not 10% but 13% based on which the stock fell in November! No one did this analysis after Q2 to say that Page did not slow down to historical levels but to moderate levels?

The cash flows are absolutely fantastic and the company being turned into asset light and low capex, most of the earnings are shared with shareholders instead of hoarding. This is fantastic for return ratios.

The performance is much better than the rest of FMCG pack which are struggling but have valuations similar to Page for 10% revenue growth! Page deserves premium hands down.

I can see absolutely fantastic franchise few years down the line and a strong business model once the GST related issues are sorted out. In fact, none of the FMCG pack show the pricing power that Page shows. They are not increasing prices to gather volumes but Page does it with ease and gather volumes too (though lower than historical but better than FMCG pack).

There will be another accounting charge of about 13 crores in Q4. (Hope analysis again do not come back with devil story). Company took ~ 29 crore revenue hit instead of ~16 crore, so the rest of the revenue will be added back in Q4, all things remaining same.

All the above analysis is done solely based on “Notes” as provided in the results. Q1: For the current quarter, revenue from operations is higher by ~1 ,408.79 lakhs and profit before tax is higher by ~631 .67 lakhs on account of adoption of IndAS 115. Q2: For the six months ended September 30, 2018, revenue from operations is lower by n61.14 lakhs and profit before tax is lower by< 121.4 7 lakhs on account of adoption of Ind AS 115. Q3: For the nine months ended December 31, 2018, revenue from operations is higher by t2,988.48 lakhs and profit before tax is higher by t1, 121.34 lakhs on account

of adoption of Ind AS 115.

EDIT: Not related to this, but a general observation: All misinformed messages gets shared on social media/twitter based on which shorts are making merry in other stocks but messages with real information does not get shared (may be) and lost in the noise.

Fantastic analysis! The slowing growth is a little disheartening. I am quite happy with the fact that they are coming up with new product lines. That will keep their engine growing for long time to come.

They are good in isolation but pretty ordinary in relevance to the EV. The cumulative free cash flows for the last 5 years i.e. FY14-FY18 are about 713 crore, and for the last 10 years i.e. FY09-18 are 877 crore. At an EV of ~24000 crore, that comes to 34x EV/Last 5 years FCF and 28x EV/Last 10 years FCF. And those are cumulative numbers, not of just one year. The valuation is still ridiculous.

If you run a DDM (since Page is now consistently paying 40%+ payouts over the last 5 years) assuming a 20%, 15%, 10% CAGR in dividends for the next 10,10,10 year periods through 2048 (a relatively aggressive assumption), you still only get around 13K crore in EV (using 12% discount rate, 5% terminal growth in perpetuity), or 45% below the current EV.

Indian consumer stocks live in their own little bubble but once in awhile it helps to cut through the PnL rubble and view the businesses as a private acquirer would i.e. cash flows. As has been noted by another boarder, imagine the business in isolation and see if you would be willing to pay such a price in absolute (forget the relative valuation for a moment).

(Not directed at anyone but more to the mood prevalent in the market where apparently no price is high enough for a “quality business”)

I decided not to invest in Page Industries in 2012 when it was trading at a P/E of 25-30 since it looked expensive to me! In isolation I do look like an idiot now, but if I see the larger picture certain things become very clear -

I have made my money elsewhere, I can very well live and thrive without a “high quality conviction stock” in my portfolio. India has 7000+ listed companies and all I need at any point of time are 20 stories that can compound at a 20%+ rate over a respectable period of time

Page has gotten re rated to 60+ P/E since then but so have so many other stories during the meanwhile. Some stories that were trading at 10 P/E now go at 30 P/E, Page is not a lone ranger that has created wealth. It is just yet another stock that has done well.

I still refuse to buy the Page Industries stock since I believe the risk reward is not in favor. In short I do not like what the stock offers me but I continue to wear the chaddi they make. I can like a company’s products yet continue to dislike the stock.

I do enjoy intense debates where both sides of the argument are passionately presented supported by numbers but the passion can and will get misplaced at times.

End of the day we are all looking to make money in the markets, it really does not matter whether you make it from Page Industries or from some other stock. When you put in a lot of effort into something it is very easy to intellectualize things too much and start to put your thought process up on a pedestal. Every above average IQ guy investing in the market needs to deal with this at some or the other point of time.

When I look back over the past 2 years I do find I have been guilty of this to some extent - in the quest for differentiated insights I have ended up hypothesizing about things that just weren’t there and ended up missing things that were in plain sight. That’s how your mind can mess with you.

We need to get back to the basics and keep money making as the central objective, everything else becomes futile in the long run if you do not make money. If something makes money it is a good investment, if it doesn’t it is not. It does not matter if the business that lost you money was a high quality one. It helps to keep the objective simple and clear, else it is easy to carried away by how good an analyst you are or how great your excel modelling skills are.

I know this has not contributed anything to the current analysis on the company, bottom line is the business seems to be doing ok but the stock price is not - the big elephant in the room is obviously the valuation. This inference at least to me is crystal clear since I do not have a stake involved here.

We all (me included) need to see things for what they are, we should not see what we want to see.

Thank you people for your replies. I respect your views because they are different than mine and help me improve myself.

Time and market has answers for everything. Market will teach you with time.

As valuations are subjective and my views are well known I will not delve more into it except that I’m willing to pay a bit premium for quality and I certainly do not expect everyone in the world to pay premium. There are numerous ways to make money in stock market.

My only request for new investors is to remember the below formulas apart from the regular investment formulas.

a) 10 * Junk = Junk but never Diamond.

b) 40 * Diamond = Gold for 1 year but diamond thereafter.

c) You will lose time if you make the Mistake of valuation in quality stocks but same mistake in junk stocks you will lose both time and your money. When in doubt step away.

@richdreamz ,Very well written and I also experienced the same. It is more okay to get low return in first year and then 20-25% CAGR with less hiccups than investing in mediocre/Junk company with 100% return in first year and then 80% loss in next year (like 2018…) and then again switch to another junk company and repeat the cycle.

It is experienced by me and will happen with everybody sooner or later. Learnt many things in past two years.

By that logic, Page or an HUL or Nestle should be bought at any price watsover. I really don’t understand how is paying 50-60-70 times earnings a bit premium for quality. A good company by that logic is same as a good stock. Meaning investors should suspend all valuation analysis and solely focus on quality of business.

It’s a reality that since 2008-09 crisis, profitability in many parts of the economy has been really depressed (infra, power, real estate, manufacturing, telecom, psu banking etc). This has meant more money chasing select few consumer stocks which have come out as starkly different compared to broader economy. A highlight of 2018 which was companies caught on poor corporate governance has not helped the cause of such sectors either. This is pure supply vs demand issue - investors have flocked to buy a few stocks like page industries simply because they couldn’t find earnings or earnings growth elsewhere. Since the float of stocks like page industries is limited in relation to demand, valuations have sky rocketed and have currently got no historical precedent (50x is like the new 20x PE in India when it comes to consumer stocks - aka - “This time it is different”). However this situation can’t go on for perpetuity. I mean can India really become a large economy demanding high quality underwear in huge quantities if 70-80% of the consumer’s wallet spending which comes from sectors like real estate, telecom, manufacturing, infra remain down to the ground forever earning measly profits (if that happens in perpetuity for argument sake btw then all sane businessman would open only consumer companies in India thereby creating serious competition for the incumbents thereby hurting incumbents’ sales growth meaningfully). Sooner than later many other parts of economy will do well compared to their past and this will lead to their re-rating. Simultaneously, as the investors money will find new sources, it will cool off the demand pressure on the little float of select few consumer and financial companies resulting in derating of the same. And yes, while a page industries may never give you an 80% drawdown but there are enough and more listed companies which will also not give such drawdowns while simultaneously also saving you from a 50% drawdown which a page industries can easily give given its lofty valuations (its already down 30% plus from peak sometime back).

Bottom line is - A stock which is trading at 50-60 times and growing earnings at 15-20% can easily go down by 50% in next 5 years and still be fairly valued in a different market setup than what exists currently. This is certainly much worse than what some of the boarders are advocating here - that the worst case scenario for someone with 5 year horizon in page industries is one year of 0% return (it’s already -30% btw) followed by four years of 20-25% yearly stock price appreciation.

PS - whatever happens to page industies, my arguments here are more from an investment philosophy point of view. I have certainly not done all the research required for predicting page’s growth trajectory but then I believe my investment philosophy gives me a good idea to find out spots where my chances of success are higher. And my investment philosophy tells me to keep away from most consumer stocks currently in India including page. Both Buffett and Munger I think would have agreed with my decision.

The above discussions is solely on the valuation front. Valuation is really a complex and subjective thing. What may be cheap for someone can be expensive for other. When you see a 6 , the person sitting in front of you see it as 9. Beauty lies in the eye of beholder. There is no perfect model to find the best entry price.

The debate around valuations is never ending and futile. It is better we keep the discussions around the opportunities and risks of the particular Business rather than on Valuations. Let Market decide what valuations it want to give to business and let individual investors decide what valuations they want to pay for the business.

There have been businesses (eg. Bajaj Finance) which despite remaining expensive created decent wealth.

Disc: I do not hold any share in the company. My buying price would be around 16500 as of now. If it comes , great. If not , lots of other options available in market.

@zygo23554

The below comment caught my attention. I have seen similar comments by other posters. But the question is do we really have such companies outside the Banking/NBFC space? ( I assume we are not talking about trading bets or cyclicals). For ex, in Q3, the only companies ( That have a long term visibility. Since we are talking about long term here) that did a > 15 profit and sales growth are Titan and Bata. ( I even reduced the number to 15% from 20%). I might have missed some companies. But I bet there arent too many. I know one quarter result is not the right way to look at it. But this has been the story since 2014. Only PE expansion. If profit growth is there, no sales growth. If sales growth is there, no profit growth. In some instances no profit and sales growth. At times degrowth. And excuses like demonetization,GST, monsoon, crude, rupee etc. The new excuse will be election. They are already talking about it in the con calls.

Note: I am not justifying page’s valuation. Also, not criticizing your comment. You have some very valid points. But I am curious how one can find 20 stories that can compound at 20% in the current business environment. For a moment, lets ignore the valuation part. But consider just the sales and profit growth at 20% or so. (I am talking about businesses outside Banking/NBFC)