It is very interesting debate between @zygo23554 and @richdreamz . I thought of adding few points to discussion.

What is value of nominal growth has to been looked also in context of inflation … This will help us understand why PE rating or derating has happened in FMCG stocks which have relative stable earning profile

In 1990s : when inflation used to be near double digits and interest rate on bonds used to exceed 15% - market used to discount non levered FMCG company at ( 1/ inflation rate ) 2 or 2.5 for normal growth companies and ( 1/ inflation growth ) 4 for superior growth companies ie @ 10% inflation the PE multiple was 20 - 25 for normal growth companies and superior young companies @ 40 PE +

2014 onwards inflation dropped significantly - Now with inflation @ 4% the value of stable earning goes up and growth earning goes up even faster … using same formula

ie PE = ( 1/ 4% ) * 2 = 50 PE is given for Low gr stable non levered FMCG

and for Young companies PW = (1/4% ) * 4 = 100 PE for faster growing non levered FMCG companies .

Is it ok - that depends upon our assumption of inflation in future and growth in earning in these companies.

Why are Midcap and others cyclicals not given these rating … because in deflationary or low inflation scenario - their earning can decline over period of time in spite of revenue growth .

Sirji, why are you considering Exit Multiple 30 PE? That is a flaw on its own .

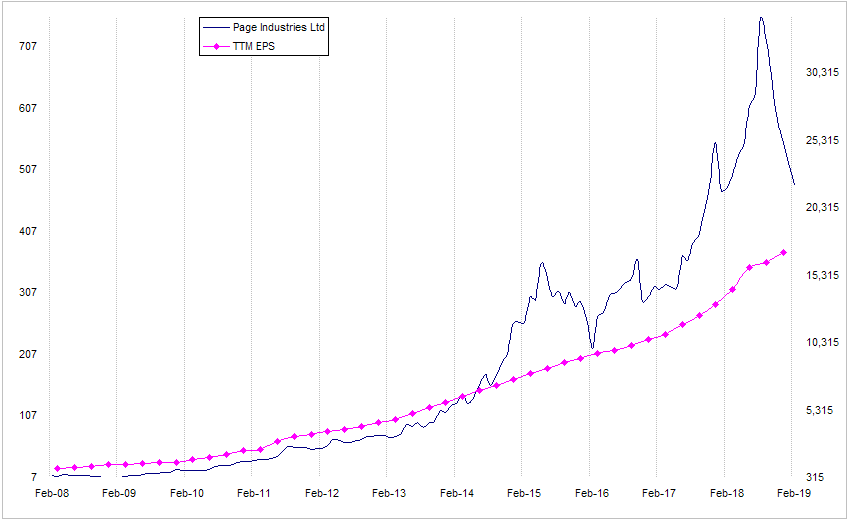

In 2012 , People thought when Page will come down in 20% growth then it will quote at 20 PE but actually that did not happen (consider current scenario). Please search with 'exit multiple’key phase in page thread you will understand…

Now the question is why it did not happen ?

My thought is because Page keep widening its Franchise value and when growth happened in FV , IV also keep increasing thus the terminal value.

Let us research first why current PE is not 30 when Page is growing at 20% growth then we will think about assigning future Terminal PE at 10 % growth / will provide FD kind of return etc etc…

It is my sincere question to not you , to those old Valuepickers who calculated Page’s valuation on 2012 and considered at stratospheric level when Page was at 2500.

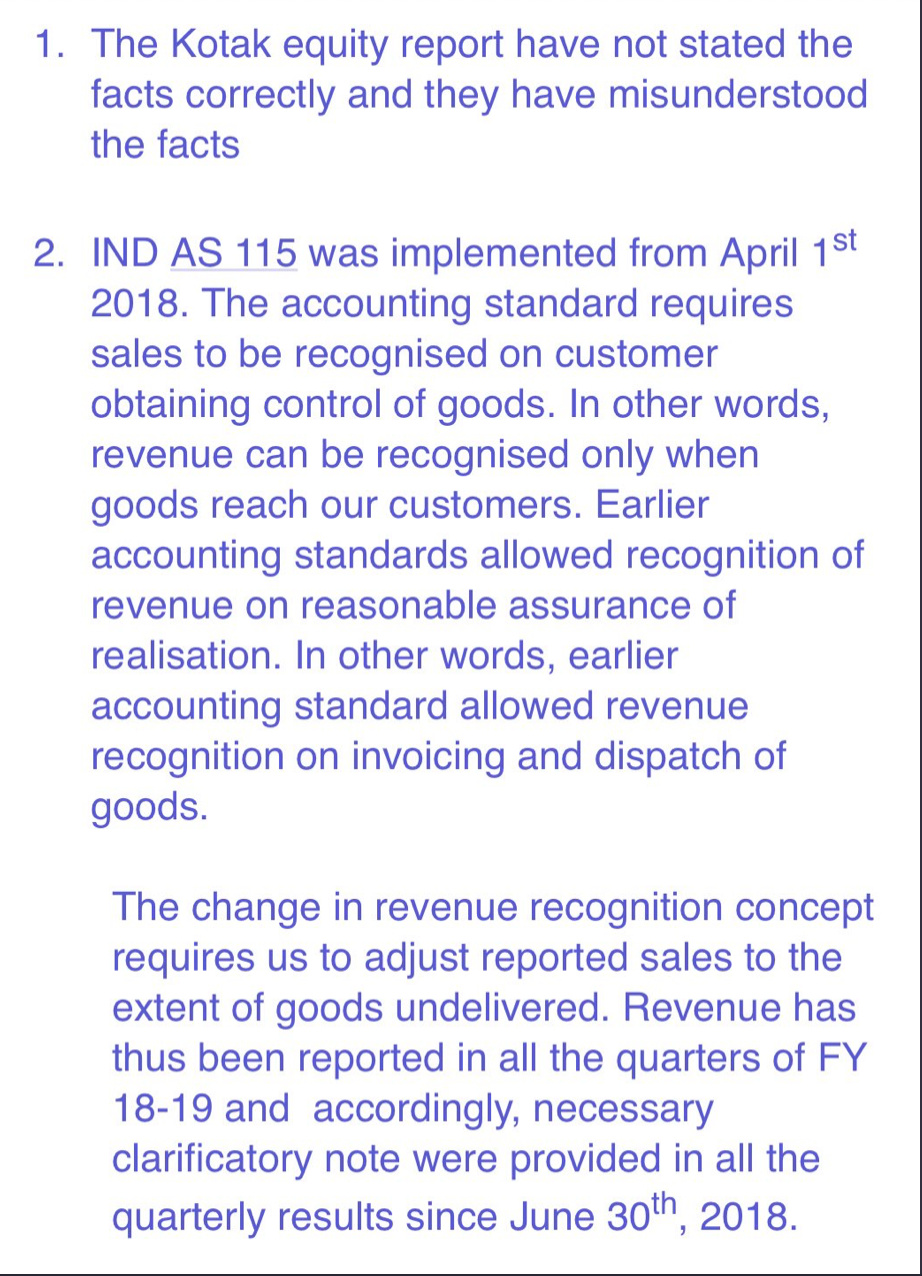

Page industries has issued detailed clarification yesterday itself to a business channel as below:

So, my above analysis that Q2 revenues were not as bad as reported is correct. So, Page management were very transparent as the notes to results has all the details, it is we who did not analyse properly. The issue is with the analysts selective publication in Q3 and not in Q2.

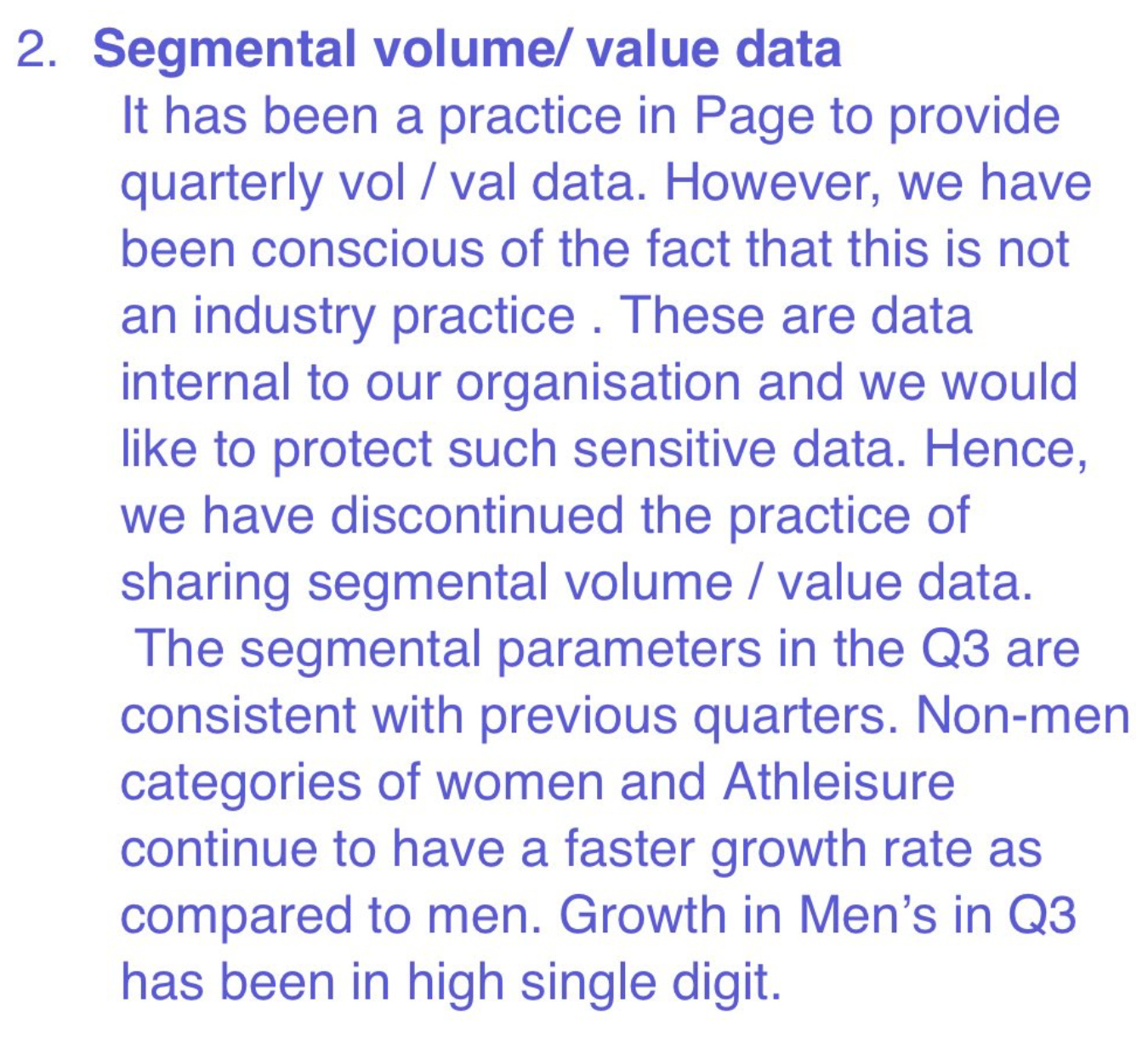

Anyway, the key takeaway for me is that volume growth in men’s is in high single digits (on top of last year Q3 volume growth of 11%) while women wear and athleisure is growing faster than men’s. So, blended volume growth could be around 10% in Q3 this year and realisation is around 3.5%.

Can you please put some light on this? It seems a new Formula to me .

As per Graham’s Growth formula like(Only applicable for companies which have Moat and don’t manipulate EPS)

Value= EPS *(PE with 0% Growth + 2g)

So as PE with 0% growth =1/COC = 9 when COC =11%

So Value= EPS* 50 , So assigned PE could become 50 kind of for a 20% growth (7-10 years of time frame)and for 30% growth (7-10 years of time frame) it will become near 70 (If and only if company have Moat),

But your formula is neither considering COC nor growth rate ? Can you please explain a bit?

I was trying to drive a point that why historical PE is not good indicator of valuation for FMCG as inflation % has changed … This is rough back of envelope calc tool used by me to see how over or undervalued a company is under different inflation scenarios . Now coming to Graham formula …

First lets understand value of growth … since it has huge impact on PE in Graham’s formula

A company with EPS Gr of 15% in a country with inflation of 4% vs in a country wherein inflation is 20% is totally a different animal .

In country wherein inflation is 4% the company is growing its future earning @ 4X time value of money and in country wherein inflation is 20% it is growing its earning @ 0.8X of time value of money .

So one cannot use Graham formula blindly . It works well to compare companies @ a point fo time in same geography . It cannot be used across the time in different inflation scenario unless you convert i Growth from nominal to real growth .

Second is relevance of Cost of capital to levered vs unlevered companies … esp companies with negative working capital … While it is easy to do it levered companies … for non levered companies it is infinite . So how to value it – Invert … Think from investor point of view .

In 1990s corporate bonds like bajaj etc gave 18% while today it is 8% to 9%. This is Opportunity COC to Investor.

Lets take assume a large FMCG company in 1990s Growing @ 20% ( when inflation was 10% - 12 % ) and now in 2016 -18 is growing @ 15% ( 3% to 4% )

As per Graham Formula

In 1990s : PE = ( 1/ 0.18 ) + 2*( 20% - 11% ) = 23.56

In 2018 : PE = ( 1/ 0.08 ) + 2* ( 15% - 3.5% ) = 36 ( HIgher PE in spite of lower nominal Gr )

Now for companies like PAGE - Historical data is small to extrapolate so you may have to take higher MOS on final PE that you get .

The way I see it there is actually not much of a debate between me and richdreamz - I actually agree with a lot of what he’s said here, which is -

You are better off buying a good business at a premium valuation than buying junk at low valuation

In quality businesses most of the time you see a time correction rather than price correction

There is more than one way to make money in the market - pick and choose what suits your temperament the most

Where we differ is in our definition of premium valuation, to me anything above 50 PE starts bordering on overvaluation irrespective of how great the business is whereas to others it looks like premium valuation that a quality business deserves.

In my post I did acknowledge that Page Industries is a damn good business, just that it is not a good stock at current levels. Missing this in 2012 looks a mistake in hindsight but actually was not since I found other stocks that gave me similar returns if not more. If I’d actually bought Page then I would have happily sold through most of early 2018 - once again looking like an idiot till the stock price started falling.

All my post stressed on was “Stay as objective as possible and stay true to the core purpose of investing - make money without falling in love with your stocks or your analysis” Funny thing is most investors of Page till the fall from 36000 were more confident about the company’s prospects than the management themselves.

Infosys lost more than 50% of its market value while the business went from USD 300 Mn revenue to USD 1 Bn revenue. History is so full of these examples that quoting them is not even necessary.

One can argue with inferences and views but one cannot argue with facts. Fact is that Page Industries PAT figure for FY19 will most likely be a good 22-25% higher than the PAT for FY18 and yet the stock is down 38% from the peak. I infer “overvaluation” but one can infer whatever one wants to

Let this not degenerate into anything other than an exchange of views and a constructive discussion

Sales and profit growth need not be 20%, 20% is what I want to make from the stock over say a 5 year period.

For that one needs to find a business that can grow at 12-13%+ over the next 5-6 years, thereby generating profit growth in excess of 15% at healthy return ratios of > 20% and a growth runway of 8-10 years. If you can buy such a story at a multiple of X and exit at a multiple of 1.5, you will most likely make your threshold of 20% return expectation over 5 years. If the company turns FCF positive during the journey and the balance sheet gets better, the multiple spike can be much higher. This is simple but not easy

The best return over the past 5-6 years was made by buying decent businesses at low valuation in 2012 and 2013 and holding them till the market came around to the view that the business deserves to trade at a higher multiple. Even after the 40% correction, select stocks have been 3-4 baggers over this period. Undervaluation with respect to business prospects (and preferably in an absolute sense) is extremely important to generate above normal returns.

The most important thing in this mental model is to focus on the quality of the investment as a whole and not just the business quality. It’s a different game altogether, if investing were all about buying the best businesses out there one does not need qualities like patience, good temperament and a valuation methodology in the first place.

PS: Continuing this discussion might take us away from the core purpose of this thread. Any more views please message me, will be happy to discuss offline

Here we are hoping that the company will get rerated. I think one should never invest with the hope of rerating. I know a lot of investors (very smart too) in 2017 to 2019 who bought low PE stocks with the same logic and then lose big.

Anyways let me also stop further discussion on this.

I 100% agree with you all. I believe that in our market with our scope for growth in consumer spending any company in the consumer space with a great brand and product along with high quality should quote at a maximum of 35-40x. This is because of the economics of these businesses. And the growth in the Indian consumtion. A 35-40x for a consumer company today will look very cheap 3 years and 5 years down the line. They are great business models however I do agree that 60-65x is too much.

I would like to know your opinion on if you would buy a HUL, Nestle, Asian paints, Pidilite, Havells etc at 35-40x. @8sarveshg

Thanks for the clarification. It is clear now

So as per Graham Formula g= COC rate -inflation growth PE is for the normal growth companies.

Correct me if I am wrong…

Please come up with your portfolio thread (or point out if you have any) so that we can also learn from you about the mental model which you applied to choose stocks .

Hope you will not mind but actually what we have seen that whoever talked for PE re rating ,multi bagger,Low PE stock ,avoid Page,DMART kind of talks they end up choosing KRBL,Mirza,DHFL and Indiabulls Housing Fin type of stocks . And we all know the result after that (33% fall is nothing near that).

So if you found great company with great valuation , please come up with your PF thread and we will discuss there .That will be great learning scope for us.

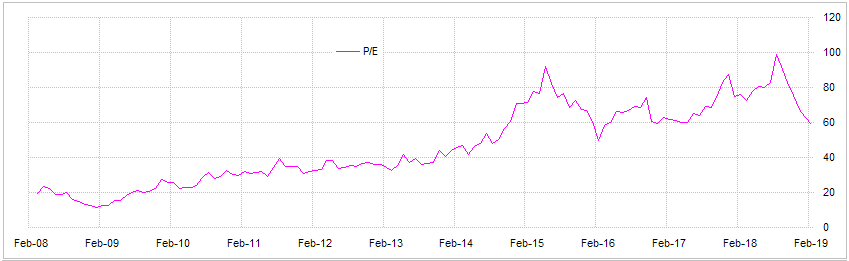

The pre-FY13 rate of growth (30-40 P/E) and the post-FY13 rate of growth (60-70 P/E). You can justify this based on whichever side of the investment one is on but this is the fact. Post demonetisation though, its been a steroidal madness (80-90 P/E). My guess is that it will come back to the post fy-13 rate of growth which is still a respectable premium and continue there (a slow time-correction from here or a fall to 18-20k levels for consolidation until end of year. 18k would also be 50% down from top.). If there are negative surprises though, it could de-rate down to the pre-FY13 rate of growth but I don’t see something like that happening anytime soon though in this quality starved market unless interest rates rise up drastically driving up the discount rates. For a FPI heavy stock like Page, the discount rates at the origin markets as well matter. Someone buying it close to that post-fy13 line could still expect to make 25% CAGR as long as the trendline holds.

and that’s because Page has posted impressive growth over a long period of time. I don’t know any other company that has posted such impressive growth over such a long time and that is still going strong.

Simply throwing your towel on stock prices doesn’t auger well

You need to substantiate with data…as what is wrong with business

NBFC and HFC are going through a trust issue here…if all companies fail…i dont imagine where india will be…as they are the backbone of economy

While the assumptions and the nominal 20% Margin of Safety will remain the same across, the ‘Cost of Capital’ for Page Industries can be determined based on how you view the company.

Risk-free Rate: At 7.72% Cost of Capital, the Value becomes Rs. 31,884.25. Only the GOI can offer a Cost of Capital that low. That is to say, Page Industries is overvalued beyond an ounce of doubt at this level.

Company Beta: At 9.77% Cost of Capital, the Value becomes Rs. 18,239.87. If you believe that Page Industries is a one-of-a-kind, unique business which is incomparable to the larger industry it is in, then you should consider purchasing Page Industries at this level.

Industry Beta: At 10.77% Cost of Capital, the Value becomes Rs. 14,710.18. If you believe that Page Industries is indeed a part and parcel of the industry it is in and is likely to face some competition that way, you should consider purchasing Page Industries at this level.

Opportunity Cost: At 15% Cost of Capital, the Value becomes Rs. 7,384.39. This is how I would Value Page for myself personally. Put another way, I may never buy Page Industries. This really doesn’t mean that Page is a bad investment in general. It simply means that I would find better Margin of Safety and lower Risk in other stocks than Page Industries.

Of course, these conclusions are valid if you believe that my assumptions for the future of Page Industries are correct. If you don’t, feel free to download the Valuation file (Numbers and Narratives (Compact) - Page Industries.xlsx) and knock yourself out.

@dineshssairam very good insights with numbers.

If i am an FII( Foreign Inst.Investor) where the cost of capital is “ZERO” (some times negative in some countries) then page is seriously under valued.

we also know who dictates or drive our market, mostly FII (some times DII, these days because of MF SIP money ) then we all should put rest the valuation debate on page.

First, the Risk-free Rate is not the Cost of Capital. There is an additional component, ‘Equity Risk Premium’ which is involved. In the US, even when the RfR is as low as 2%, Cost of Capital ranges from ~5%-15% (Source). In addition to this, FIIs usually need to add Country Risk Premium to their investments, which is currently 2.64% (Source).

I was researching with past years data . Few counter question for learning purpose. I am posting here because that could be helpful for deciding Page’s valuation.

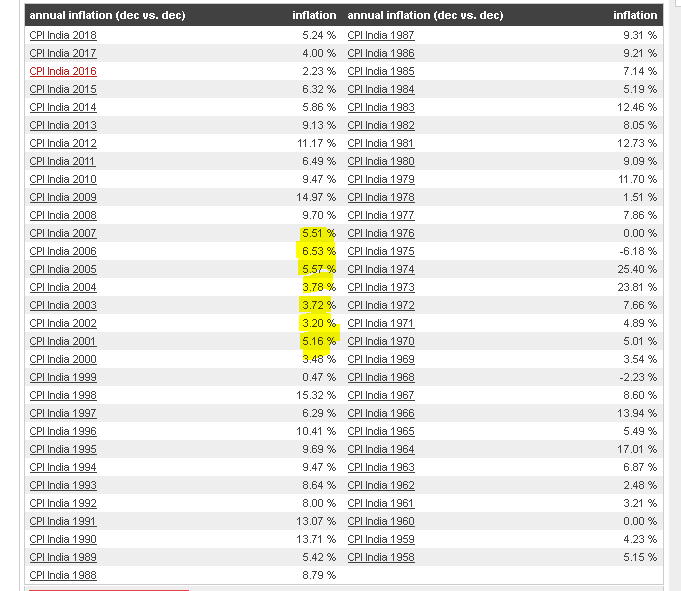

If we check Historic Inflation in India then found that from 2000-2007,CPI inflation rate was 4-5% which is almost similar to now (2014-2019)

PE multiples manifest from what you expect in future ( Earning growth , Cost of capital /inflation ) & Current Relative attractiveness of investment .

One can do absolute under or over valuation with Graham or any valuation metric . However many in market may not invest in undervalued stock if there are other opportunities that are more attractive .

In 2005 FMCG stock were undervalued by big margin and hence if some one had bought them then he would have earned mega returns for more than a decade …

Today these stocks are in over valued zone as all positives are priced in and people are not willing to price in any risk to ( inflation & Growth assumptions )