after a 15month long consolidation that started in Mar 2015, are these the new signs of break out ? what are the technical charts for PAGE speaking ?

from the day PAGE has been included in F&O, the growth in share price has been curtailed to a range, when would this cease to happen ?

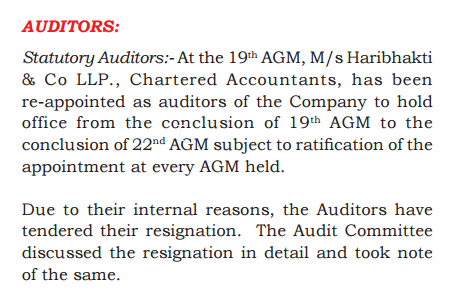

Was going through Page Industries annual report and came across resignation of auditors - Haribhakti & Co, who have been auditors for atleast 10 years…Strangely, it says for auditors resigned due to their internal reasons? Anyone knows the reason for their resignation?

It could be due to new provision in Companies act that auditors needs to be changed every 10 years. Please see old news item on this subject

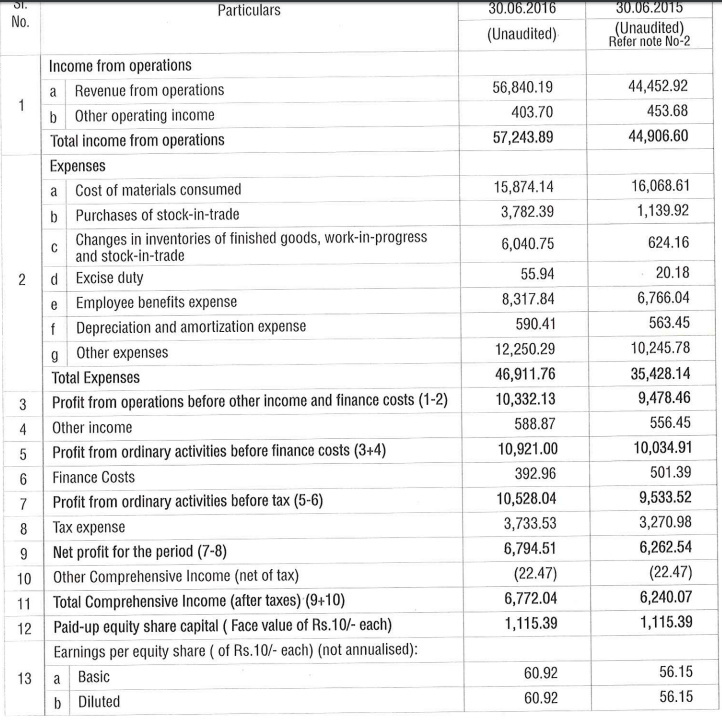

Results came few days back for Page

Good increase in Revenue by 27% but subdued profits due to Change in inventories of finished goods.

(Don’t understand this expense, reasons and impact well)

1 Like

changes in finished goods inventories by 1000% !!

what would be the reasons ?

Certainly on the higher side as this equals the quarterly PAT figure. May be they are preparing themselves for the coming growth as per their communication to analysts. Volume growth of 21% certainly points towards that.

Has management spoken post results? How you know volume growth is 21%as revenue growth is 27%.

Sumit what does the chart says now about page industries

Boss, absolutely zero idea about charts. Not tracking closely after exiting more than a year back. @Hrishi they provide data to covering analysts. I think I saw somewhere published these growth figures (volume +21%, price +4.5%)

Thanks @sumi00 .

I just found it at:

It says:

Page Q1FY17 results were mixed with robust volume led growth. Key highlights:

-

Revenues at Rs 5.7bn up 28% yoy, with volume growth of 21% led by men (+19.8%) and sportswear (+31%).

-

EBITDA at Rs 1.1bn, up 9% yoy, on back of gross margins declined by 520bps to

55.1%. Lower other expenses (-140bps) and employee cost (-50bps) curtailed EBITDA

margins decline to 19.1% down 330bps yoy.

If it can sustain such a good growth in volume then we are back to 30%+ CAGR company.

Only worry with Page was the Volume growth and if it solves then Wow…

Anyone attended AGM? Any notes or links for the same?

ok . i didn’t know that u sold off. BTW what did you buy after selling page. just curious as i am unable to find something of same quality so holding on page with reduced no. Thanks

Have taken portfolio approach in pharma (Granules, Neuland and Shilpa) and IT (Take, Cambridge tech and Allsectech) after selling Page. Thankfully have made good money in all of them that I hold now. Last one year has been good since I could use all big dips to buy more. Traded some others with mixed results. These biz come nowhere close to Page’s quality but chance of outsize returns is low here. My theory was that consumption is late cycle play so would take longer to give returns especially at this valuation. If you want to remain in consumption, take a look at Parag milk, Manpasand beverages or even V-mart. I didn’t have cash but would love to own at right valuation.

Nice idea and picks. i also have some granules,neuland and cambridge tech. Ya I am in search of great compounders and history tells us that it can be found in consumption pharma private finance space and IT.

I have thought a lot about Manpasand beverages and parag milk but never built a conviction to sell page and buy them. Parag milk quality is no issue but what if tomorrow Nestle Britannia Danone plans to sell milk and cheese in a big way. Then will Parag be able to save its Turf and premium valuation. I have never tasted Manpasand products so not able to judge its quality so gave its a pass. it has a huze rural marketskare in gujarat.

But both are huze hits and made lots of money for its shareholders. I didn’t made any significant money in last 1 and 1/2 year as i was not able to churn my portfolio at the right time and holding to old stocks. Only new significant addition are Ujjivan and can fin home.

Any one still holding Page Ind? Do you thing it can give 15-20% upside from 16000 levels? A great company, one of the utilisation of capital, good growth in Profit and Sales but languishing at this level since 2 years.

Any news can flare the price up or despite one of the best performing financials, it may simply continue to be between 13-17K range. Any thoughts?

I am still holding page but with reduced quantity.i feel it can still give 15-20 return but earnings are not catching up. They are not able to ramp up their sales. Let hope new pay commission helps it. But it’s super expensive.offlate all stocks in that sector moving up so page is also moving. But frankly speaking I love holding page and so I am biased.

1 Like

I am holding it for very long time, divested a part of it in Eicher Motors sometime back. At times i do get frustrated with Page as returns are muted. But I believe as a business it still have a very long run ahead of it. It wont give spectacular results but over a long horizon it will give 20-22% returns. Short term can be range bound as per Hitesh sir as well.

1 Like

No activity on this thread for a long time. Understandably so, as the stock has gone nowhere since the last 2 years or so. Page has traditionally been priced as a 21% compounder . As is the case with all good businesses when growth slows down the stock doesnt crack or fall - it goes into a sideways movement and patiently waits for the management to make necessary operational changes for the company earnings to fall into place. After some years of below average growth, the June quarter operating earnings have been very good and have grown by 25% , indicating that the underlying strength of the franchisee has remained intact.

8 Likes

Bheeshma I bought this stock sometime back at below 60 PE.

I think with 20% CAGR growth and ROCE of 40% +, there isn’t much downfall. Companies like HUl etc trades at 50PE with 4-5% growth. Since I was short on funds, I couldn’t buy more but less than 60 PE will always be a buy for me given the pace of growth doesn’t go below 15%.

Kanv

1 Like

Hi, I have been working on Page Industries and its competitors and have done some work on comparing between Page Industries & its competitors with regards to Selling & Distribution expenses. Please find the analysis in the following link

http://investmentswaladost.blogspot.in/2017/08/what-they-tell-you-versus-what-they.html

19 Likes

@karu_lamborghi_ Brilliant brilliant work.

This is what everyone have to learn/understand and work on rather than just saying or rather shouting as EXPENSIVE, based on just price divided by earnings i.e; PE.

Excellent work

Some things are just expensive in life for a reason, that’s it. we have to find out why.