Brilliant write-up. Though holding page for more than 8 years never ever tried to analyze page in such details against it’s rivals. Thanks again for the wonderful post.

Another important revelation to me and i have noticed this pattern across good steady businesses like page is that its not the actual growth that matters - its the perception of growth that plays a big role in valuation. All companies hit speed bumps now and then but perception is more resilient and doesnt change easily. Of course perception is rooted in reality but it seems to be relatively inelastic in general as long as there is some growth. When growth numbers are negative however its a different story and even a minor inconsequential negative quarter seems to impact the PE dispropotionately.

To give you an example Godrej Consumer Products - an otherwise fine business growing at a fast clip recently reported a negative June quarter & prices promptly fell by 18%-20% despite the fact that in the previous year (2016-2017) operating earnings had gone up by a sizable 45%. PI Industries is another example - after years of posting stellar growth numbers it reports one negative quarter and mayhem ensues.

There are some companies which exhibit this resilience as manifested in their PE ratios and to its credit Page has never had to face a no growth situation (at least in the data i have looked at) . The PE ratio should be called the perception about earnings ratio rather than the price to earnings ratio

18 Likes

That’s a very new way to look at pe. And it is very hard to guess when that perception is gonna change. Whether it’s just one quater of bad result or multiple quarters. When you buy high pe you are left to the perception of the people about the stock. But it is also true that some stocks like astral poly, eicher motors, symphony continue to enjoy high pe for a long time now.

2 Likes

Jockey India to double production capacity by 2020

3 Likes

The sleeping giant of the industry (stock price point of view) is finally waking up. Doubling of capacity in less than 3 years may mean more than doubling of profits in this time frame. That also, by a business which generates around 50% ROE and is the market leader.

I am also observing a lot more aggressive advertising by Jockey in recent times. And more visibility of Exclusive Jockey stores. GST implementation will also add to volume growth as organized players become stronger.

Patience in holding on to the stock may be paying off.

10 Likes

Listen to the last 15 seconds of the interview:

Question: 20% revenue growth for the next 20 years?

Genomal (promoter): VERY COMFORTABLY

You only have to decide whether to believe in what the promoter is saying.

1 Like

Being invested in Page has been one of the most interesting experiences for me in terms of understanding how the market perceives quality businesses.

I have flitted in & out of Page more times that i would care to admit because i felt at that time that the PE is high & because my knowledge was really half baked. I did all these DCF type calculations which always told me to stay away from Page.

In general , High PE - bad, Low PE - good was the lens through which i looked at everything.

All through though, Page never disappointed me. My biggest disappointments & painful experiences were all the low PE stocks i held. I used to hold Page for a while sell it at a modest profit and put the money into these low pe items. Only to see the low pe go lower and page galloping away.

I am glad that happened because it taught me a lesson in a way only the market can teach you.

All else being equal the high PE stock is better than that Low PE stock. It is most certainly not the other way round.

32 Likes

I fully agree with you. Page and Gruh have taught us that high PE/PBV is not bad and can sustain if the results are predictable and consistent with a long runway.However when there was a blip in Page in the last 2 years the 3 year price CAGR did dip from 50%+ to 25-30% now.Given the new dynamics after GST it seems Page is back on track

5 Likes

Just a word of caution. During bull markets valuations are roaring high day by day and it becomes very frustrating to see oneself missed out. Though I don’t know what will happen tomorrow but it seems that all valuations are running away so high it’s hard to find value.

I agree that Page is a great company but are the valuations justified ? I haven’t looked deeply but from top it feels on higher side. But in this market it may go higher who knows. In the end want to finish with these thoughts.

• First-level thinking says, “It’s a good company; let’s buy the stock.” Second-level thinking says, “It’s a good company, but everyone thinks it’s a great company, and it’s not. So the stock’s overrated and overpriced; let’s sell.”

- Howard Marks

“No asset is so good that it can’t become a bad investment if bought at too high a price. And there are few assets so bad that they can’t be a good investment when bought cheap enough.”

- Howard Marks

4 Likes

Kindly desist from personal attacks. It is a violation of community guidelines. If you find something that is inappropriate please flag it and let the moderators take a call.

6 Likes

Just to put things in perspective and put gene back into bottle.

Below is sayings from Charlie Munger and Warren Buffett (no intro needed of these guys in this forum) on how they got their knowledge and all they did is application of that knowledge.

“I believe in the discipline of mastering the best that other people have figured out. I don’t believe in just sitting down and trying to dream it all up yourself. Nobody’s that smart.” – Charlie Munger

“I’ve mainly learned by reading myself. So I don’t think I have any original ideas. Certainly, I talk about reading [Benjamin] Graham. I’ve read Phil Fisher. So I’ve gotten a lot of ideas myself from reading. You can learn a lot from other people. In fact I think if you learn basically from other people, you don’t have to get too many new ideas on your own. You can just apply the best of what you see.” - Warren Buffett

PS: Boss, we are investors not inventors.

5 Likes

14 Likes

The results of Page have been muted for some time now. Q1 FY 18 was a welcome surprise. Is it a one off Quarter or something has significantly changed in the recent months compared to past 2 years of muted growth!?

1 Like

I think it was one-off. IMO, distributors were restocking before GST. I sold off long back but looking back few concerns need revisiting.

Promoters stake selloff finished as soon as supernormal growth of 35% ended.Now they can’t sell anymore. At the same time he handed the CEO post to someone professional who ensures 20% growth going forward. This could be coincidence as well but overall well timed for sure.

1 Like

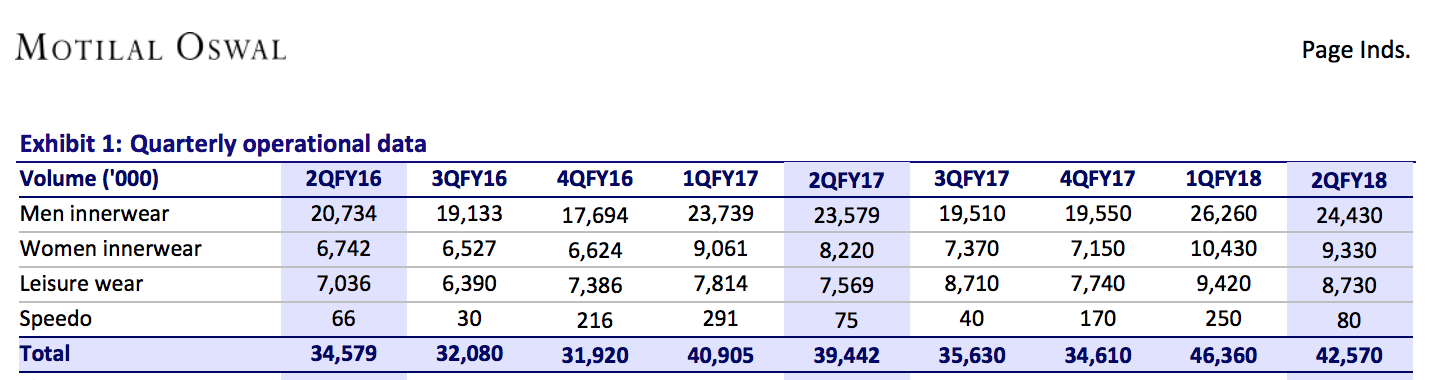

@sumi00 I don’t think so. The growth has been of course far less than the 35% levels but still strong around 20% in the last 3 quarters. See the data presented below:

The main drivers being Women’s Innerwear and Speedo sportswear. But the real question is if they can sustain the 20% growth levels with moderate growth in Men’s segment!?

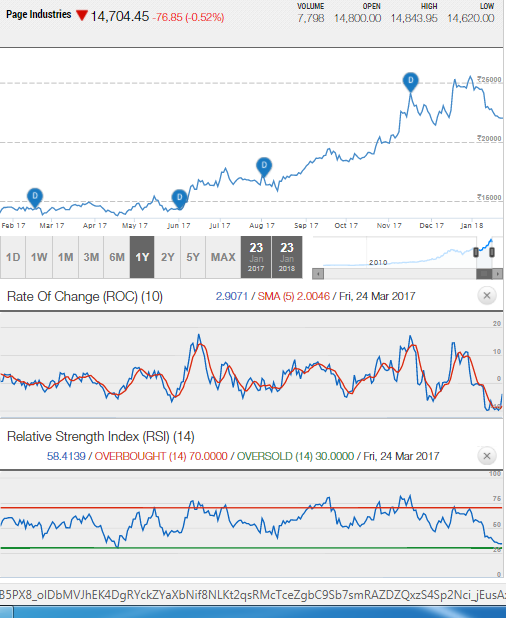

Though Page has historically commanded higher valuations, another point of debate should be if one is still comfortable with rolling 1-year PE forecast of 60x!

1 Like

ROC is down now. By past trend it should go up. RSI is near to bottom. By past trend it should go up.

Slowing growth of from 35% to 20% is priced in, it seems.

Hoever some trigger, good news is required for an upmove.

2 Likes

Jockey gains brand share, pips Amul Macho, Rupa:

Do the company publish this data?? I am trying to locate the source of this data…

Elephants can dance…outstanding results by Page Industries…

FY2018 pat up 39% over FY2017

Q4 2018 pat up 40% over Q4 2017

Philip Fisher’s words come handy here…

“If the job has been correctly done when a common stock is purchased, the time to sell it is – almost never.”

8 Likes