re e commerce - its not big enough to affect brick n mortar players

if at all , it is more in ladies section where Jockey is growing at 40% +

Its a one of the thrust area for Jockey too and it is also planning rather already doing the ecomm act via its own site and tie ups with all major players

check out its tv advts - all suggest buying through their website in the end

Jockey is expected to Launch Premium yet affordable Terry Towels… Apart from Kids wear and Company Online Portal, Terry towels will be the 3rd factor adding to the growth.

Can anybody confirm that Jockey is on the verge of launching Sports terry towels …

You are breaking news and asking for confirmation too! Page already has online portal for e-ordering. As far as I know they are completing implementation of new supply chain mgmt. software which is expected to reduce inventories and lead to better demand management (and sales!?). May be e-com portal would get revamped too.

last month i was in a mall. as usual page was doing great business. i had read that a listed comp called ashapura intimates fashions (valentine brand) opened an EBO in the same mall. i asked the jockey salesman if it had any impact. to my surprise, he hadnt even heard of brand valentine. i then visited valentine store. it was empty and i was the only one. i checked out a few products. it was not at all impressive, priced on par with jockey. i visited again, after an hour or so. again not a single customer inside. and this was on a weekend evening.

Thanks for the update! I too looked at the stock but could not build the conviction. Page’s strategy was to build brand, distribution and then they ventured into EBO. They have grown in concentric circles as far as strategy goes but Ashapura wants to jump into success right away. Page has built a solid supply chain and now front end. Lovable has failed to break the fortress so far and let’s see Valentine could challenge. I remain skeptical

We are comparing apples to oranges. Ashapura is in same stage, as what Page was some years ago. I know who is a colleague of mine, who lives right next to a valentine store in an upmarket location in BLR and he confirms that the store is always busy. At this time, Ashapura has to do many other things right and years away from being mentioned in the same line. Also, Ashapura is mainly a lingeri firm and there are other things like the related party with Momai etc. So, it will take its time but don’t base your opinion because of a store in a mall. I had seen Hyd mall, with dedicated space for Jockey, where hardly there was a sale and if I had concluded that all this fancy for this stock is a waste, I would have missed the stock…

PS - invested in both

I was comparing the evolution of strategy. The difference is when Page came there was virtually no worthy competitor but Ashapura will have to contend with giant which is not slacking either. In many sectors there was no second miracle. (e.g Infy in IT, HDFC Bank in banking etc etc). In the same sector, Lovable too has marquee investor names but seems to have failed to create value so far. I wanted to say that despite best of intentions Jockey is very well entrenched.

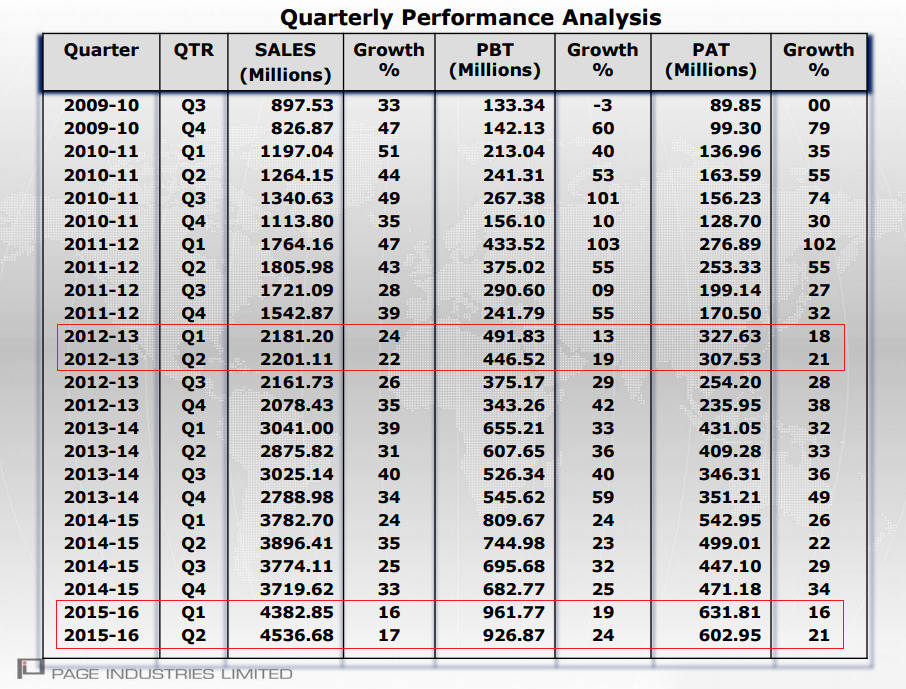

My only limited submission would be check growth in sales, which was more than 20% in 2012-13, which decline to 16-17%. While I understand that on such large growth maintain is 16-17% growth is also difficult take, but then valuation of Page at 16K had limited scope for error in my opinion. Also, the growth in Speedo would take time to make material difference in Page business and it is too small currently.

Disc: Holding since last 2 years and sold 1/3 position 6 months back.

I too visited Valentine store run by Aashapura and page are into completely different league, while I found page offering premium quality, valentine has been average quality and they may achieve volume, but will not be able to achieve the kind of margins enjoyed by page,

I have seen CEO’s interview in which he was talking about benefits of EBO. I’m not a marketing guy but EBOs works best when you have multiple offerings and loyal customers (e.g. Nike, Tommy etc). It will definitely get customers but good enough to generate great returns? I find it a tall order.

FY16 would end up with an EPS of 200 thereabouts against optimistic EPS estimates of 240-260 estimated earlier.

QoQ FY15 vs. FY16 comparison:

14.8% increase in revenue and 16.1% increase in profits.

Dividend of 21 INR declared.

The tax expense this time around is lesser then last year’s despite 16.1% more profits, so need to find why the tax expense is lower.

Point to note here is, despite the lower tax expense, the profit growth came in at 16% is something what market would be terribly disappointed.

At prices of 10,000 per share the PE would be 50 on FY16E EPS of 200.

FY15 EPS of 175.75 vs. FY16E EPS of 200 is about 14.3% growth YoY.

Given the market sentiments, the high valuations the stock is still commanding versus the growth it has shown thus far, there could be tough times ahead for the stock.

200 EPS looks be worst case scenario. Page is all set to enter next phase of growth. Valuations look slightly stretched but it is growing like any FMCG company with high ROCE and cash flow. If we compare with likes of Colgate, HUL, Nestle and Marico; it does not look expensive.

It is still a multi-year story and urban consumption will get a leg up with 7th pay commission.

I guess results were just a trigger to get aligned with overall market correction.

You are right comparing Page to FMCG to some extent but underwear is not so fast moving normally, maybe in these market conditions. Its one notch below true FMCG unless it can continue growth rates of 25%.

200 is not the worst case really. I think best case is 210. I remember many people had factored in 250 EPS for FY16 so 200 is a disappointment and it was reflected in price.