Totally agree - larger point being access to investor base, especially when there’s a bull market in the entire ‘‘spec chem’’ space. Fully aware that this was an iodine company a few years back but recent developments warrant a closer look.

No idea Saran. But I guess in current consolidated form it might not be so attractive for PE or other large investors. All bets are off till Lasa comes out of Omkar sp. Chemicals. That business may not find it so difficult to get access to capital due to its better quality. That may also be reason why management wants to separate it from parent Omkar so it is not shackled by the parent.

Another reason can be a debilitating inability to sell the merit of the investment to professional investors. The management is neither very articulate nor savvy. Just look at their reports and announcements and you will find silly mistakes like wrong additions etc. Will you part 50-100 Cr to people who cannot add?

Absolutely agree - I’ve been coming to the same conclusions. I think they need to add management bandwidth if they want to scale up. While I think they’ve done a great job (scaling up Lasa from nothing to a 170cr biz / increasing production capacity) , believe they need to add bandwidth and reliability to get to the next stage.

I cannot believe there’s a company (that too with an IR firm involved), that’s not able to sell itself to the market, esp. when their business is relatively firing.

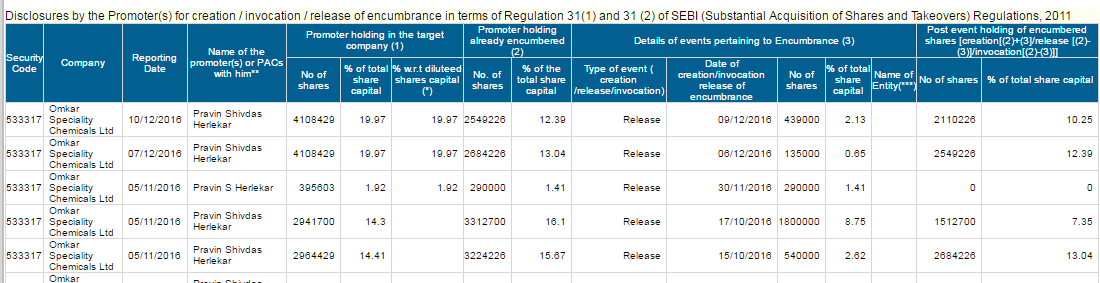

The management shareholding de-pedging is complete and no more share sale is needed by them. Their holding is now 51.2 % and will stay at that level; minimum. They may buy back from the market is my opinion over the next 2-3 years to again increase their holding. The last de-pedging was done around 10th December 2016. The sword over them that was there due to pledged shares is non existent anymore; although, their reasons for pledging the shares were very honorable, but they were being measured by a very tough yardstick.

On the financing front, the reason they pledged their shares was only to help the company’s customers as they were sitting on orders of products that were urgently needed by the customers and they needed to do capex to be able to keep their promises to their customers. The impact of this is clearly visible in the growth of their sales. Also, the customers they have have a very high pedigree themselves. That is a great thing.

BOB is their bank and it was taking them ages to try and get further funding. With pledged shares would any of us as a PE company be able to buy those shares? Dilution of equity would have placed them in a precarious position. They were in a catch 22 and that the have resolved even at a great personal cost to themselves of having to sell their own stake. Plus all this while they still kept on paying a dividend which they could well have not paid and reduced their headaches.

This is what is is an exceptional company at an exceptional price with an extremely rare and exceptional management. Now that everything is resolved, and the capex mostly done, you can see the performance of this company over the next 2 years. The topline and bottom line will double just with existing capex which is online and more coming online in next 2 quarters (including the numbers of lasa) and a positive rerating is now overdue.

Disclosure - Invested with 20 odd percent of PF from before this clarity came.

2 Likes

When did this clarity on de pledging complete came?

Do you have any source…i can’t see any new disclosures.

Dear Paresh,

The share pledge and release data will point you in the right direction…

http://www.bseindia.com/corporates/sastpledge_new.aspx?expandable=5 then search for omkar and click submit… the maths is sort of clear. I was also not able to put an exact number till the link below, but it maps up correctly. The link is: http://www.moneycontrol.com/video/business/omkar-speciality-gets-patent-for-beta-ketoester-chemical-process_8110801.html

Best regards.

But still it shows… 10% is pledged

Maybe I am wrong in my opinion of the management’s integrity where they clarified that this is now their stake. They have said it openly in the interview. They are by law allowed a few days to file a disclosure. But even then, the direction of de-pledging is quite clear, it is moving one way. Let’s see the updated data in a few days. Best regards.

1 Like

Also Paresh, forgot to mention; for the shares pledged with the NBFC, the NBFC will have to transfer the shares back to their demat account and that can take a few days from the payment to release the shares. Only then can they file the disclosure.

I do not think 100% depledging is done. Some way to go for that.

I think I have to agree with Girish ji here . For example, let’s take the 10th Dec filing. The total promoter holding end of period is 33.67% + 13.0% + 2.51% + 1.85% = 51.03% (similar to the 51.04% mentioned by Pravin herlekar on the TV interview).

The pledged portion of total outstanding share is 7.35% + 10.25% + 3.51% + 1.59% = 22.70%. This means that over 45% of the promoters shares are still pledged !

Please let me know if I’m calculating wrongly here. L

1 Like

If any seniors are monitoring this post can they give their calculations and opinions; It would be most helpful to me at-least and I believe I can probably also say so on behalf of Saran, Paresh and Girish. Can we request for some help with regards to the de-pledging logic? Experienced help please. Also, Girish, your understanding of Omkar is excellent I must admit and commend you for it. Best Regards.

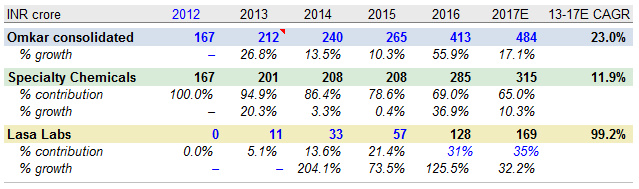

Please find below some calcs on how they’ve been able to grow a business from nothing. The numbers are purely sales and profitability should ideally show a similar picture.

@giridesh3 Sir, do you believe they have been sacrificing growth at their spec. chem business over the last few years to growth the Lasa? Are the 15%–20% CAGR’s you mention in the PPT earlier shared mgmt estimates?

One must definitely commend the mgmt. team for building a business from near zero, while staying cautious on other developments.

4 Likes

Dear Saran. Thank you for your input and clear assessment without any bias from noise. Helps make the picture so much clearer. Best Regards.

Yes they want to shift focus more on VET API…

They are building a base for that…

May be Pharma is also on the way…

“ALL STATEMENTS ARE QUALITATIVE JUST FROM MY INSTINCT”

I have just read the full thread of Omkar . The promoters Pledged seems to be very highlighted problem for Omkar , Can we assume that if there were no Pledged shares then the company too would have benefited from the Tail wind facing by Chem industry . Regards to financials margins have remained more or less constant which poses a steady business . If we are interested to bet on the chemical industry is Omkar protected in anyway by a Strong business model or a good Tail wind … and what I noticed was the company is not making FCF inspite of which it pays out dividends is what I wouldn’t want to see . so when I see Total Net profits for 5 years was 54 Cr and free cash flows for 5 years was 91cr than I could see more than a substantial sum is locked up in Working capital .

So De - Merger is the value unlocked here I feel , As mr Girish has previously provided his presentation on Omkar and Lasa . I would demand a more MOS from current levels to enter buy the Company . Where I’m placing my hypothesis is in another 2 years When Omkar the current Stand alone business has good FCF than Market will assign a better valuation .

Dear Raghav. You are absolutely correct that their cash was stuck due to WC requirements. The management has also said this in a recent call; I am sure you will be able to find it when going through the recent calls. They in fact to my understanding had the cash ready for most of the de-pledging but then could not complete it due to the more pressing in their opinion needs of WC (This also made me take an even more bullish view on the company) Where they have a need to clear their holding and still use the cash for WC as the business is growing at an amazing pace. What a wonderful and honest management.

I am sure, that when the haze settles, irrespective of the de-pledging complete or not as of the moment, then the prices of the stock will also be factored in and maybe even become a hot favorite of the “supposed smart money” who poor fellows knowing everything cannot invest till there is full clarity  Then everyone who wants to find the next Thirumalai can pay for the “Malai” Today, I find this a steal at the approximate prices temporarily quoted for the stock.

Then everyone who wants to find the next Thirumalai can pay for the “Malai” Today, I find this a steal at the approximate prices temporarily quoted for the stock.

I don’t pay much attention to de-pledging as such but it is a factor here and I am grateful that it is. Else, how would one buy an exceptional company at such a low exceptional price. No institutions interested either today, which make it even more fun to get a company like this. No fear and bullish like anything. Wish I had even more spare cash to invest now!

Also, correctly said Raghav, the demerger of Lasa is the icing on an already delicious cake. If we see the PE anyways even ignoring everything else and then add double the revenues in some time with the capex done, this seems like a sub 5 PE company with a 1-2 year view. Which cannot be for much longer. The big bulls will get in.

For the moment, Mr. Market can play games; I would buy this whole company anyways if I could afford it and delist it. That is my bullishness.

Also, “seniors” @hitesh2710 @Donald @ayushmit and to my favorite @mvmakadia (sorry other seniors ) Sorry to bother you but please can I humbly request you to look into this one if you find some spare time. I hold five stocks and this is a 20 percent…ish holding of the portfolio).

Best Regards.

Disclosure 1: 20% of my portfolio.

Disclosure 2: I am confident I am only 70% right on the data. 100% confident that there cannot ever be 100% clarity.

Disclosure 3: I have a low IQ. Please help the “special needs of low IQ” people like me.

Saran:

The sales for chem biz is 300 or so for FY16. From FY12 to FY16 the sales growth is 15.77% or so. Management is maintaining that estimate. The biz is hobbled by WC needs and that may put some lid on the growth rate. An that is not so bad. Growth at the cost of balance sheet is never good. In fact it will be good if they completely tone down the growth for year or two and improve the BS strength.

It is true that Lasa is growing in leaps and bounds. But also on smaller base. Still 136 for FY16 I expect it to reach at least 180 Cr in FY17. With EBIDTA margin of around 24% or so. The growth and margin may sustain in future also as they plan to introduce formulations in next year or so. In next 4 years 25% of revenue may come from formulations biz.

The LT debt on LASA BS will be around 75-80 Cr. If we assume the sales of Rs 300 Cr and ebidta margin of 25% by March 2019. Then they should be able to get rid of this LT debt comfortably. The WC needs are not that demanding for Lasa due to better payment terms.

3 Likes

Raghav,

The capex was high for last 4 years to more than double the capacity. For next 3 years no growth capex is envisaged and maintenance capex will be Rs 5 cr per year. So you will see spurt in FCF. In FY16 one can see 21 cr FCF at consolidated level despite 46 Cr capex.

For MFG companies , that too in growth stage, FCF is tricky valuation measure to use. Because large capex will show negative FCF for couple of years and then huge spurt in FCF when capex is done.

4 Likes