To clarify further-

The promoters have sold 18 lac shares to raise 28 Cr. They will retire high cost NBFC debt with that. They will in turn bear that debt as an unsecured debt to the company. So from NBFC the debt is now gone to promoters. The cost would be 12-12.5 % instead of 18 to 19% for NBFC loans. Also this debt will be unsecured and less restricted than NBFC kind loans.

yes… benefit of 6%…

but ideally it should have been zero percent unsecured loan… which gives more comfort

So, no more selling from the promoter side hereafter ?

Whats the minimum percentage shareholding would be maintained by the promoters ?

( as per June-2016 end declared pattern, the promoter % is 56.18 ).

there won’t be any selling further… everything has been completed…

and i believe at present its 58% and not 56%

So, I guess it is Buy time Again… Looks undervalued, if Lasa is finally getting demerged (if they’ve made-up their mind and put forward a date).

Paresh Bhai,

Did they give any specific date, like March 2017? Or is it just your personal reading?

When asked on demerger… they didn’t give specific date…

Sebi Approval Received… Now there is some approval pending with High Court…

Once that is done and all shares are de-pledged… this de merger will be taken up…

But they expect this listing to be completed before March 2017 they said… (No specific dates)

1 Like

Yeah, I’ve seen this. It is a strange procedure actually. I’ve seen the same in the case of Mastek-Majesco demerger also. The shareholders, and Sebi gave approvals early, but the HC did drag the case for months (I can’t make the sense of it). And even after the HC’s approval, it took quite some time for Majesco to List.

So, I think that unless they’re hell bent on demerging (without second thoughts), it will take much more time than that.

Seems to be worth the while to wait, and Buy on Dips.

DISC: Investment Initiated @145 Levels.

Orientus Emerging Markets Small Cap Growth Fund has submitted the disclosures under Reg. 29(2) of SEBI (SAST) Regulations, 2011aquired2011http://www.moneycontrol.com/livefeed_pdf/Jul2016/CF67ADEA_F4A4_46CE_ADD4_5DE6D48EB868_151908.pdf

CONFERENCE CALL - from Capital Markets

Selling of part of their holding by promoters was necessitated by the need to de-pledge promoter holding to facilitate demerger and repay company’s loans taken at high interest rates

The company held its conference call on 19th July’16 and was addressed by Mr. Pravin Herlekar CMD of Omkar Speciality Chemicals

Key Highlights

-

The company did a capex of around Rs 180 crore for increasing the capacity from 1700 tons to 4500 tons, 4 years back, and a further around Rs 140 crore to increase the capacity further to 9000 tons in last 18 months. There was also a high working capital days which were recently brought down from 200 days to 110.

-

Funds were already borrowed from banks and company had no other option but to raise funds from NBFC as well by pledging shares at 2.5 times cover at 18% interest rates. The Rs 45 crore borrowed from NBFCs were to be paid in next six months, but the company does not have enough free cash flows to do the same. The company did try for QIP and private equity, but market was not favorable and due to high leverage things were not going for the company.

-

Hence Promoters had no option, but to sell part of their shares in the market, give the funds so raised to the company at lower interest rate, which will be used to repay the NBFCs and release the pledged shares.

-

The company has borrowed around Rs 45 crore from the NBFC companies @18% and rest around Rs 200 crore is borrowed from banks @ 12% kind of rate.

-

The Promoter has sold off around 18 lakh shares and raised around Rs 28 crore from the market. Of which around Rs 10 crore have been paid to NBFC. The Promoters are having around Rs 20 crore of funds with them. They are confident of paying the entire sum of funds of around Rs 35 crore in next 6 months and thus releasing the entire pledged shares in due course.

-

As per the Promoters, the whole idea of selling the shares is to de-pledge the shares, to reduce the interest costs and for better balance sheet and credit rating of the company.

-

The money which has been pumped in by the Promoters in the company will be treated as unsecured loans and the Promoters will charge interest @12%.

-

With no major capex required, management believes to be a debt free company in next 4 years.

-

As per the Promoter, there will not be further requirement of any selling of shares. Total of the 93 lakh shares that were pledged, around 75 lakh shares still continue to remain pledged, which will be de-pledged in next 6 months.

-

The promoter shareholding which was at 58% at the time of IPO went up to 67% due to warrants and creeping acquisitions, now went back to 58%.

-

The company would use more of packing credit and non fund based facilities to reduce interest cost further.

-

The de-pledging of shares was also required for the approval from all the bankers including the NBFC for the de-merger of the company. This is another reason for the sale of shares and getting the pledging removed.

-

Of the total Rs 45 crore to be paid to NBFC for de-pledging the promoter shares, around Rs 28 crore will be funded by loan from Promoters and rest will be from internal accruals.

9 Likes

All over the world spin offs usually take 8 to 10 months. The only reason is court approval takes time. All other approvals can be arranged within 2-4 months. The court takes its own time. Even in US this causes delay.

The management has indicated by December demerger should be consummated and listing of Lasa can happen before March.

Addition to gist of conf call:

In the conf call the promoter said that they will not go for pledging their shares any more. The rest of the pledged shares will be released in next 3-4 months. After that no more pledging business.

To my query he answered that the business has a reached the stage where it can fund the WC needs using internal accruals. No more ST debt to fund WC needed. I found this comforting. This was my key concern. We can make peace with reality that chemical biz will always have CCC days of 100 or more. And biz has to bear the cost of this WC. But ST loans at 18-19% to fund this WC was huge risk factor and put off.

(Note- Always do your own due diligence and thinking before your buy any stock. Omkar is not exception to this rule.)

Discl- Hold Omkar. Bought more after the conf call.

3 Likes

Talked to the CFO Mr. Agarwal regarding the recent disclosure by the company. This was an internal share transfer to Mr. Omkar Harlekar.

58% was the promoter stake on 19th July as told by promoter during the conf call and it is the same in the recent disclosure (58.01% to be precise). No further stake sale has been done after conf. call and will not be done as was told in the conf. call. Entire pledge will be released before demerger as was told in the conf. call.

Disc: Invested.

4 Likes

Thanks for the update. So, it seems to be the time for retirement for Mr. Prakash.

Disc: Invested. Bought more today at lows.

Stock Sitting at a strong (Multiple tested!!) Weekly Support Line. Looks like a rally is on the cards!!

DISC: Invested. Bought more today.

2 Likes

Seems… it can’t pick up pace upwards till positive Q1 announced…

Waiting eagerly for some positive news…

Disclosure: 10% of my portfolio now

thanks mr vaibhav. it creates confidence on omkar.

disc; invested

1 Like

I think the next trigger will be Q1 results. There are no announcements regarding the same. Last year, it was announced on July 17th.

When are they going to publish Q1 results? Does any one have any idea? Considering that the management already guided for a mute FY17, chances of good Q1 results are very less.

Hi Guys,

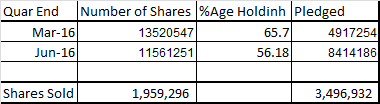

As per BSE filing, the number of shares held by promoter and shares pledged for the quarter ending Mar’16 and Jun’16 is as below

Promoters sold 19.6 Lac shares and at the same time the additional pledging done by them for the same period is roughly 35 lac shares.

If we assume that the shares were sold by promoter at Rs. 165 (Avg. of 180-150 when stake sale happened) the sale proceed available to them was 32.33 Cr. If they utilize the entire sale proceed to pay off their high cost debt, they will be able to release shares worth 80 Cr (Taking loan to value of 40% i.e. collateral value of 2.5 as mentioned somewhere in concall). In number terms, they can get 48-49 lac shares released (80cr./Rs.165) whereas their pledging have gone up from 49 lac shares in March quarter to 84 lac shares in June Quarter.

Am I missing something??

Disc:- I am not invested but started tracking the stock very recently.

Hi Mukesh,

There seems to be additional pledging done between March 2016 to June 2016.According to a press release dated 13th July 2016 (link below),96,56,486 were pledged and promoters sold 17,25,035 shares to decrease pledged shares by 16,65,254.

Hope this helps.

Disc:-Invested and around 5% of my portfolio.

Regards

Bala

Reading the thread and doing my own quantitative analysis , I have developed some substantial conviction in this company. I guess anyone who intends to enter this stock should do it extremely slowly over a period of 1 to 2 years. I understand that many people have already completely entered it with full conviction. And I respect that. I was just going through the notes from @aveekmitra ji in one of a very old thread, where he shared his experience on how to go about buying in bear market (extremely slowly). Now again, one might disagree that this is a bear market, which is fine by me.

Disclosure: Tracking extremely closely with substantial cash in hand to allocate.

2 Likes