Can anyone who attended post summary of today’s concall? Thanks

2 Likes

Yes, please post the call summary!!

Register yourself with https://www.researchbytes.com/ and search by company for “Omkar Speciality”, under the company page, you would notice the “Conference Transcript (Voice)”. Click on the same to listen to Today’s call.

2 Likes

This is the gist of the call and what promoter said in the call:

Praveen Herlekar explained the events that caused them to sell their stake. He said the company still has 27 Cr from July sell off but that money is parked in WC. The growing business needs more WC. They have requested banks to enhance the credit limit by additional 50 Cr. The approval process has taken time. The banks have longer approval cycle due to NPAs etc. The promoter said they are expecting the approval by Nov end or mid Dec. It is now gone to corporate office for final approval. Once those funds come they can use this 27 Cr to pay off Rs 19 Cr NBFC loan and release the pledge. The depledging is their highest priority. By Dec they want to release all the pledge. hence the decision to sell off additional stake and raise the cash. From this cash they released 25% pledeged shares recently.

In Jan 2016 they had 55 Cr NBFC loans against the shares. They have paid off 36 Cr till date and so 19 Cr is still pending. They are also paying back term loans as per schedule and the interest. The shareholders are paid regular dividends. The business is generating cash.

They don’t see any issue with bank NOC for demerge scheme of thing. He explained why bankers did not attend court meeting. They are waiting for corporate approval. In the meeting they have say Yes or NO. Without corporate decision they cannot give their verdict. In next 15 days the final approval may come. Another court convened meeting may be held in next 3-4 weeks.

They said they are confident that demerger process will go without hiccup. They do not see any risk.

They anticipate demerger to be consummated in the last quarter of this fiscal.

5 Likes

My notes in addition to what Girish has already captured from the Conf call:

11,50,797 shares which is 5.59% of shareholding, of the promoters, were sold

23,40,000 de-pledged amounting to 11.37%

Total shares actually pledged till date is now down to 26.9% from 38.28% of shareholding [difference ~ 11.37%]

Total share outstanding in the company = 2,05,78,004

Shares that are still pledged/ held by the bank = 55,36,232 [this is 26.9% of Total outstanding shares]

Reduction in loan prepayment on Pledged shares from 55 cr in Jan > 35cr > to 19 cr today.

Working Capital[WC] interest cost is 12%

Pledged loan Interest cost is 18%

per mgmt. - apart from the depledging related complexities, the mgmt. claims, that they have never gone back on their words or side stepped any statements.

History on ‘Pledging necessity’

two years ago - capex required for enhancements. of capacities

close to 180 Cr spent in the last two years in Capex.

36 cr - Bank Of Baroda

50 cr - Bank Of Baroda, another loan

86 Cr

74 cr - OP Cash flows generated in the last two years.

out of this 35 cr have been used for repayment of debt &

6 cr in dividends to shareholders

—sub total = 41 crs

Remaining 33cr (=74-41) has been used for WC needs & Capex.

86 cr loan + 33 cr internal crores =~120 cr

the remaining gap was achieved by pledging shares for 55 cr

Every year 16-18 crores have been repaid religiously - target to be Debt Free in 3-4years.

No further loans planned for big capex, but loans to run the growing biz to support Capex will be done.

My take:

- If the company knows how to manage the growing biz (25%) and working capital, why did they have to be blocked for WC funds. awaiting approval from the bank to release the loan sounds crazy. Why could they have not foreseen this coming and build sufficiently liquidity?

Hypothesis - company is growing biz steadily @ 25%. Working capital needs have been taken as loan from banks on short term basis [typically @ 12%] in supplement to the internal cash that has been generated by their operations.

since the biz has grown, needs for WC have increased.

Given the circumstances especially in regards to non performing assets (NPA) from a bank perspective & the bureaucracy involved in the banking system with multilayer approvals required [ branch office, zonal office, head office, corporate office, etc.]- this has caused delay. ( similarly in the case for the bank and creditors not turning up at court proceedings and providing the required No objection certificate.)

2)What happens if there is further liquidity crunch where in the banks delay till say January and Company needs more funds for WC.

Hypothesis - now this is a tricky one with the worst case scenario in mind.

They have to go figure out some other methods of borrowing money - additional borrowing or

Raise additional capital by diluting the equity stake. [Now this is a slippery slope till they stay above 51.1% ownership.] Hopefully this scenario does not play.

All in all - this is a good company with ability to generate good Operating cashflows ( generated ~90 crores last FY).

De-Merger will unlock value.

5 Likes

Generally bank credit officer will know more than us. His u willingness to lend on working capital, which is lowest risk and can be monitored, worries me. I would avoid.

1 Like

Interest cost decline in near future may aid Omkar improve its working capital.

In AGM they said they plan to increase the exports and goal is towards 30% or so over a period of time. The advantage of exports is better payment terms and they can also avail soft loans for these export orders.

1 Like

Have they announced the results. They were supposed to announce today at 12pm, however, bse website has updated only the transcript of the last concall.

results announced.

available on NSE

I am unable to locate it on nse…could you please share the link

thanks…

results seem to look good at first sight…

specially consolidated current liabilities down by around 30 odd crorres…

thumps up…

lets hope everything bad has been done and now all good

Paresh I can’t see the results on my phone. Can you post revenue, profit growth and receivables, inventory levels.

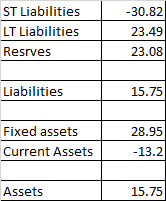

Following are the significant changes in balance sheet between Sep 30 and March 30 2016

(Read this as ST liabilities down by 30.82 crores as of Sep 30 compared to March 30 2016)

Looks like there is significant decrease in payable/ current liabilities whereas the receivable has not decreased by that much (- 30.82 cr vs -13.2 cr ) .

Looks like the cash inflow from operations and LT debt are used to fund ST liabilities.

Does this mean poor cash conversion cycle and stretched working capital ? Otherwise results look good on Revenue (27.8% YOY) and EBIT (31.6%) terms and finance costs have gone up ( which can come down once LT loan becomes loan from promoters)

Under current assets , we have other current assets of 20.03 Cr . Not sure if this is the amount that is going to be used for de-pledging.If I remember correctly, they need to repay 19 Cr to get out of the pledging mess.

Also Fixed assets have gone up . so looks like some capex was done during last 6 months.

2 Likes

Thanks kavin, the result seems good enough to me. Working capital position is likely to improve be q4.

If you compare standalone and consolidated statements you see that Lasa might have grown by 2x on YoY basis. May be around 45 Cr. You will also notice that although sales for chemical business has grown in single digits the receivables have grown in double digits. The business is still eating WC. But still WC has gone down on a consolidated basis. Teh reason is Lasa in my opinion. It has no receivables issue like chemical business. Slowly but surely it is becoming significant portion of revenues and that is helping. It seems they are allowing Lasa to grow full throttle and may be even curbing chemical business growth a bit. which is not bad as a short term measure.

I think Lasa has done well in first half and may do Rs 180+ Cr in FY17. That is just my estimate looking at the numbers so far. I expect EBIDTA margin around 22%-23% range. With economies of scale both margins and ROCE should improve over next 2-3 years.

Bear in mind that BS may be deceptive right now because the large part of LT debt (around 70-80? ) may go to Lasa as it should go. Chemical business may show 45 or so Cr LT debt after spin off.

Demonetization by Modi may be God send event for Omkar:slight_smile: Banks are flush with cheap deposit money after demonetization. Now their problem is how to lend all that money because the credit demand is still not there. Let us hope BOB corporate office quickly approves that Rs 50 Cr additional credit to Omkar.

4 Likes

moreover interest would also decrease…along with quick approval

these all are super positives…

Anyone attending the Conference call?

conference call. It’s already over. On researchbyte