Thanks @dineshssairam.Appreciate the effort you are putting to educate novices like me . On emore query I have is regarding SOP. Do we need to consider ESOP? Could you please provide some clarification on finding it from AR?

SOPs are often mentioned as “Employee Stock Options” or “Warrants Held” or the like. It’s usually found in the Notes to Financials part of the Annual Report. Cupid has not issued any.

Do you use real or nominal GDP growth rate?

Nominal, since Interests Rates and all the other growth rates are also nominal.

It’s not a strict rule, but more like a rule of thumb saying that a company cannot grow too fast forever.

Posing a general question to everyone following this thread:

Currently, the model terminates assumptions at Year 10. But in real life, we have seen some companies grow at higher rates for as much as 20 years, before actually settling down (Maruti Suzuki comes to mind).

So would it be more logical to include an option to extend the termination period based on the company’s size?

Ex: A ‘Small’ company’s DCF will be projected for 20 years and then terminated. A ‘Medium’ company’s DCF will be projected for 15 years. A ‘Large’ company for 10 years.

The obvious effect is that Small/Medium companies will have a higher Value than usual because of the extended period of High Growth (But not by too much possibly, depending on the assumptions). This goes with the real world logic that if you catch a good company when it’s young, say at 50 Cr. your future payouts will be way higher than if you would have caught it when it was a 10,000 Cr. company. Size slows down everything.

The old model assumes that all companies will have a high growth of only 10 years, which seems a little illogical.

I think 10 years should be the conservative number. Historically, how many of these 50 Cr companies became 50000 Cr companies in 20 years? Maybe 0.1% or thereabouts? So thats a pretty low probability event. There is a possibility that the company we are valuing is among this pool but then what are the odds when the base rate is so low? We might like to delude ourselves that we have picked a winner early but we must infer the specific from the general (the base rate).

1 Like

True. But then, does including an option make sense?

Even if not for 20 years, 15 years would be an option for Medium sized companies. It’s theoretically proven that companies with a long runway (Smaller companies) have a High Growth period that’s sufficiently longer than the Mature companies.

Let’s say a 50 cr company grows at 25% for 20 years. It still becomes roughly a 4500 cr company, nowhere near a mature company in India, which is around 20000 cr.

I just thought it’s wrong for a 50 cr company and a 50000 cr company to have the same High Growth period.

Maybe to tell a story with some more optimism, it could be presented as an option, albeit a low-probability one. I don’t see anything wrong with that - so that we get a range of valuations and still choose the most conservative one or whatever suits one’s disposition.

Here’s another thing to consider - A company that’s at a 20k-50k Cr market cap might probably last 10 additional years on average than smallcap. Not saying anything about growth but just longevity. This is similar to saying that average term of survival for someone with a terminal disease is 6 months but for those that cross those 6 months, the term of survival could be in years. I guess using 10 years is a lazy substitute but its also a reasonable heuristic. I think tweaking it a bit for India does make sense as an option.

Yes. All I’m saying is that the option will be there. If the person Valuing the company assumes extraordinary things like 30% for 20 years, then they have to justify it with their story. Additional periods of DCF doesn’t necessarily mean distorted Valuation.

I read extensively today to understand why companies have an elongated High Growth period.

Prof. Aswath Damodaran and Michael Mauboussin were specifically very helpful:

http://pages.stern.nyu.edu/~adamodar/New_Home_Page/valquestions/highgrowthperiod.htm

In a gist, I have added a logic in the model which determines the length of the High Growth period based on ‘The Quality’ parameters of the company. Simply put:

- Companies which have very high Quality parameters will have utmost 20 Years of High Growth (High Growth doesn’t imply that the firm will grow at an extraordinary rate – it refers to the period when the firm’s Return on Capital is significantly above the Cost of Capital).

- Contrarily, a company with very low Quality parameters will have only 10 Years of High Growth.

- The in-betweens will have 15 Years of High Growth.

Here is the updated model (The initial post has also been duly updated):

In the real world too, this is the truth. Companies like Maruti Suzuki or Infosys have been able to grow so strongly, for such a long time because:

- They had sizable moats, which kept competition away and customers nearby

- Their management team was stupendous

- The economy itself (Including the government), openly supported their line of business

- Competitors were either low or were too slow to catch up to their ‘secret sauce’

I have also reviewed the model using all the points stated by Michael Mauboussin. So, I hope this model has come closer to becoming an ‘Economic Sound and Transparent Model’, like he says in the article.

If anyone Values a company with the new, updated model, kindly let me know if you faced any difficulties. I am yet to update my blog where I describe how to use the model. I might do that tomorrow.

Happy Valuation!

2 Likes

One way to check this is, value the Asian paints, Page, GRUH, Pidilite, BRITANNIA, Nestle, Gsk,Astral, Infosys, Hdfc’s and other highly grown businesses or high PE stocks by taking their 10years back no’s and arriving present value and test/check this model, may be we will get interesting info.

I did that, but in a different context (Not the exact same model, but a similar one):

As far as good companies are concerned, the market is very shortsighted. We can’t verify any model using back dated numbers, because of the sheer difference between what that company was actually worth and what price it was quoting at way back.

But yes, it confirms the fact that good businesses tend to have an extraordinarily higher value in comparison to current prices.

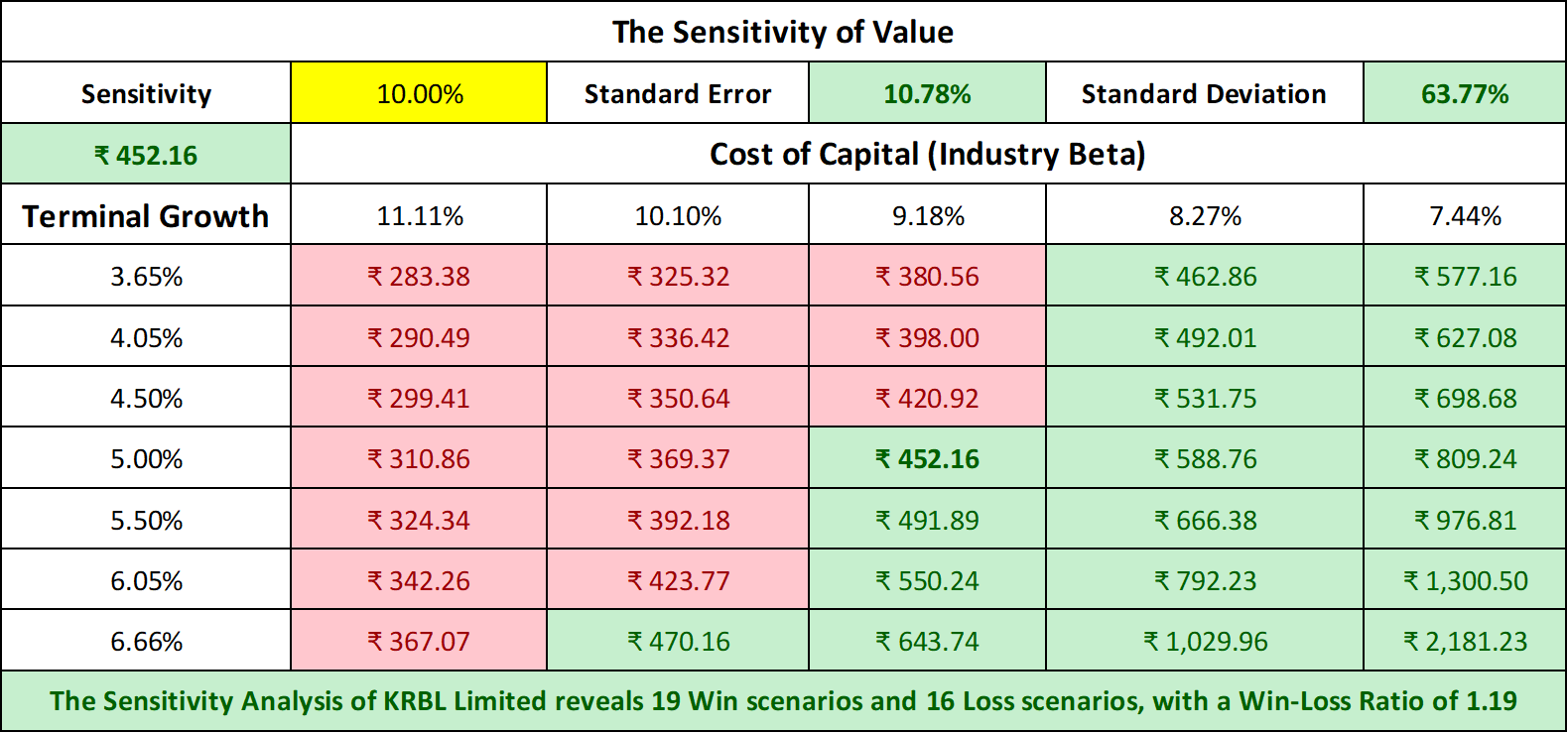

As mentioned in an earlier post, it bothered me that I couldn’t add a Monte Carlo Simulation tool to the model. Because, in fact, a company’s Value is not a single number. It’s a range of possible numbers. I solved the need for this partially by introducing a Sensitivity Analysis tool to the model.

The way it works, it requires an input percentage of sensitivity (Say 15%). Based on this, it simulates a range of possible values for the Cost of Capital and the Terminal Growth, which form an important part of the Value of the company:

Then, the Value of the company is re-calculated using the different simulated values of WACC and g. There is also a display of Standard Deviation and Standard Error for the sample set of Values, just to act as a control. The final output calculates a Win-Loss Ratio based on how many of the simulated Values are above the Price and how many are below. A >1 Win-Loss Ratio is preferable, of course.

You can access the updated model from the original post (I have made some other minor changes - you can read through the model updates list):

I still believe that a proper Monte Carlo Simulation is the best way to identify a range of Values for a company. If you are interested, you may want to revisit my earlier post:

Your feedback is important, as always. Thank you.

4 Likes

Great work Dinesh. Thank you for adding new dimension (monte carlo etc.) in valuation. This will help us a lot.

@LearningToFly I wish I could implement a MCS in the model. It’s not that I can’t, but the model will become too messy and slow. I have implemented a Sensitivity Analysis, which is as close I could get to a MCS without making it heavy.

Hi One more query on ESOP. I was analysing PCJ which is having ESOP. Should we consider total number of options(26,79,330) or Number of Options vested during the year (72,630). Also the strike price should be the Exercise price (10). Also could you please clarify SOP expiry date? Is it the maximum period( which is 8 in case of PCJ). Also could you please explain the different types of debts and maturity?

Option Valuation

- The total number of outstanding options should be taken.

- Yes, Strike Price is the Exercise Price.

- Yes, it is usually the Expiry Period. However, if the Options are held by a closed group of people and you have an idea of when they will exercise it, you should use that instead. But yes, in the absence of any such information, use the default Expiry Period.

The idea here is to find out the probable Equity Dilution due to Option Exercise in the future, and then bring it back in Present Value terms. This will effectively be removed from the final Value of the company.

Market Value of Debt

A company usually borrows long-term from a variety of sources, usually a variety of banks. These loans differ in quantity and maturity. Consider the following example:

- 100 Cr, 2 Year Loan from Canara Bank

- 200 Cr, 2 Year Loan from SBI

- 500 Cr, 5 Year Loan from HDFC Bank

Ideally, you should enter:

-

‘Debt (Type A)’ as 300 Cr and ‘Maturity A’ as 2 Years. This is because both the loans (Canara Bank and SBI) have the same Maturity, so they will have the same Present Value Factor (Which is based on the Cost of Debt).

-

‘Debt (Type B)’ as 500 Cr and ‘Maturity B’ as ‘5 Years’. This is the loan from HDFC Bank.

The way the model works, it will convert whatever portion of Long Term Loans you have entered into the PV of Debt. If there is a remaining portion of Debt you have not entered, they will be taken at Book Value (No additional entries required here – this is automatic). This is because whatever is not a Long Term Loan, is most probably a Short Term Working Capital Loan, whose Book Value closely resembles its Present Value anyway.

I hope this made sense Feel free to ask away any more doubts in the model.

1 Like

Very basic video - helpful for newbies! Sorry for posting if not at the level of discussion here!

5 Likes

This was one of tens of videos I watched before creating the model. It explains the number part of the DCF quite lucidly. Thank you for posting.

Hi Dinesh - Q4 numbers for KRBL are out now and KRBL has duly crashed  . Time for your step by step post on all the inputs to the model with a link to the source for each input …

. Time for your step by step post on all the inputs to the model with a link to the source for each input …