Vprs, how do you accumulate when you feel it could be a market bottom. Suppose for eg, if you feel NIFTY has bottomed at 10k during October 2018, do you deploy all the CASH you hold at once in your favorite stocks at 10k or do you go after individual stock bottoms?

I see INDEX bottom need not necessarily be a stock bottom. I always struggle here.

Please throw some light on this based on your experience

The following chart is an update for the Nifty Bank Index going as far as 2009. It can be seen that the price has run way above the historical PE band and is currently trading at 60X PE mutiple.

I also crosschecked this with the PB ratio and that is currently at 3.8 as per the NSE calculations. The 10 year average for the PE is at 21x and one SD above the average is 34.3x while the below one is 7.9x. As it is quite clear that markets are pricing in the elections. The banking sector can go through a massive re-rating if the earnings does not come through.

2 Likes

You mean derating?

/* *******/

Setting the right context is important here.

When we talk about ‘Averages’ (Nifty PE isn’t exactly an average but an aggregate - of market caps over earnings), one thing you have to make sure is there is no data which is skewing the facts. In financial terms, this is called ‘Normalizing’.

My view is that the E being used to calculate Nifty PE is highly skewed, making the valuation look uncomfortable. Currently, though the NIFTY PE looks extremely expensive based on long term average, it is hugely skewed by the Tata Motors loss of ₹26k crores and SBI NPA recognition of ~₹11k crores in March & June quarters in 2018 which forms a part of the TTM aggregate profits. There is a huge probability of these turning into some ₹2-10k profits next year if not more (assuming TAMO 0 profit and SBI 2006-2016 average net profit of ~2.5k per quarter).

Total Nifty profit including banks and TAMO was ~₹60k crores. When assuming TAMO & SBI’s profits to be zero next year (because there might be some margin reduction in the OMCs), we see a 40-60% bump up in earnings - taking the PE to 0.63-0.7 of the current PE reflected in the market - which comes out to ~17.5-20 which is moderate valuation as per history.

I believe it can give 12-13% return over the long run (10+ years) from here.

Cheers!

7 Likes

Correct. One shouldn’t read too much into these aggregates, it is a waste of time. Nifty is not an index of “best” companies as is commonly interpreted, since parameters for stock selection are technical such as liquidity, floating stock etc. I don’t know why no one has created an index of “quality” companies based on parameters such as ROE, ROCE, Margins, Debt to Equity etc. Even the sectoral representation in Nifty is totally detached from the real economy. So what does Nifty indicate, really?

4 Likes

There are different index with Quality, Value etc.

http://www.niftyindices.com/indices/equity/strategy-indices/nifty100-quality-30

1 Like

Wow, that’s interesting ! Will check it out. Thanks.

This mindset makes sense right now, as PE is 28, highest in decade and is showing no sign of relenting. From this level, in the past, market quickly found its way down. Any bad news hit hard. We recently averted a war, and yet Nifty blinked only 100 odd points. This is unprecedented.

On the flip-side, there is a rule, another strong possibility: The more time market spends being overbought, it will balance out being oversold! It is a rule seen on most timeframes. Putting it in numbers, Nifty has been overbought i.e. PE > 24, for almost a two years now, first day of crossover above PE 24 was May 15 2017. So it will spent an equivalent time below PE 15.

1 Like

Hi

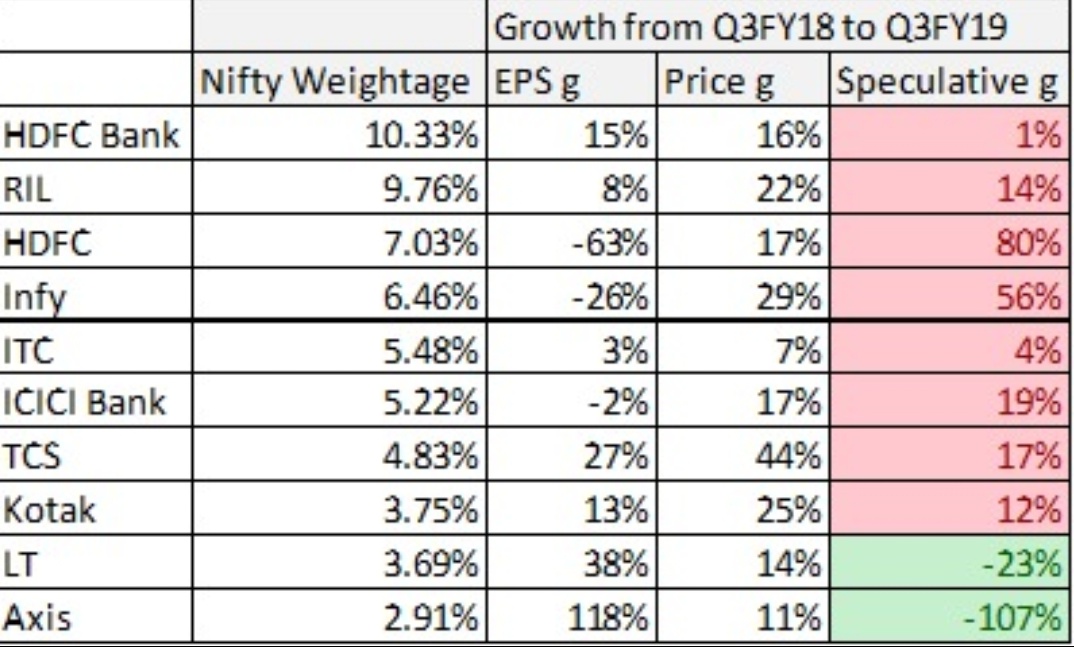

Some numbers related to the growth in earnings of 60% of the constituents of the index below.

Please note this is not adjusted for dividends/bonus etc.

Rgds

1 Like

Tata Motor and SBI are not in the above table, so, I wonder even if there was a major change in their earnings how much impact it would have on the Index.

Furthermore, it is evident from the table that most of the growth in Price of Nifty has been speculative, meaning, not backed by growth; just plain 'ol expectation or sentimental increase.

A heavy-weight like HDFC is a shocker… it has 80% speculative growth.

Infy has 56% speculation or lack of growth in its share price.

This table speaks for 55% of the Index weight. I wonder what kind of a mess the other 45% is in.

This is a little scary, because, having seen my share of these tables I know that most of this speculative growth gets wiped out in bear markets, and that is the purpose of bear markets: to bring the price to back to the ground.

This data is all wrong so is analysis. Infy has split. HDFC had one off earning last year due to investment sale.

Time correction is possible, but in the past that has not been the outcome after going in the overbought territory. I think it is the psychology behind why a stock gets overbought in the first place. And what happens, when that euphoria is “burst”.

nifty50_mcwb.xlsx (25.0 KB)

This excel shows 5yr CAGR price and EPS growth (1yr and 3yr as well). Here, for ex., Asian Paints is shown as being 10.78% “overheated”, if only this were to normalize, then the stock will have to fall to 900.

Bajaj Finserv and Finance are 45% overheated, price has run ahead of EPS by a difference of 45% due to the strong sentiment. Is this sustainable?

Heavyweights, Reliance, Kotak, ICICI are also high on sentiment.

There are others running much ahead, but do not contribute much to the overall weightage.

I intend to refer to these numbers and find which stock price is lagging behind its EPS (on a five year basis), like Hero, wipro, itc, infy, M&M, tatamotors.

The real question is, are many stocks in Nifty 50 high on sentiment? And what can happen to their stock prices when this sentiment ebbs away? I feel, a 50% correction at least. And I do not want to be caught in the eye of the storm, because I know I would not be able to hold amidst such an onslaught.

2 Likes

Tata Motors and TMDVR, SBI, ICICI Bank and Axis Bank are companies where earnings have been temporarily affected. Couple of others where earnings are depressed are Bharti Airtel and Sun Pharma are systemically affected companies where it is not likely there will be a sudden increase in earnings anytime soon. Apart from these companies, almost all companies in the index with the exception of a few cyclicals like Vedanta are close to lifetime high earnings with good growth in the last year.

However, if we just add the weightage of TML, TMDVR, ICICI, SBI and Axis - these 5 companies form less than 11% of the total index weight leading me to believe that even if the earnings here are drastically better, I dont think it would make a huge difference to the trailing PE numbers.

I am one of those people who has missed the bus (only 20% invested - 10% each in October and Feb) hoping that sanity prevails sooner rather than later. Currently happier investing in AA bonds which are yielding 10-10.5%. Seems like a slightly less riskier option. Currently waiting for the “fat pitch.” Hope this doesnt turn out to be an “oversmart” decision on my part few months/years down the road.

How to invest in bonds directly? I use zerodha… until now I was happy with liquid funds with 7.5 yield,.any pointers who use zerodha can be helpful

The desirable price range for Asian is around 900.

Its 5 year EPS growth has been 12.85%, whereas price rise has been 23.63%. For price growth to match EPS growth, in last 5 years, the price will have to come down to Rs.900. Being such a fabulous enterprise, I do not expect its EPS to reduce, unlike for other Nifty 50 participants where I expect to have a 5% to 10% discount.

Rs.900 is near its 2016 low, and the high of an earlier trading range from Jan 2015 to May 2016. This also makes it a nearest strong support.

Fall from 1450 to 900 is 38% correction. In bear markets, the best of Large Caps have corrected that much.

3 Likes

It will make lot of difference.

Another observation regarding Nifty PE. We saw inclusion of consumer names like Titan and Britannia to Nifty. Now this will have upward impact on Nifty PE. e.g. Britannia replaced a commodity company HPCL. Even depressed PE of Britannia will always be much higher than normal PE of HPCL.

1 Like

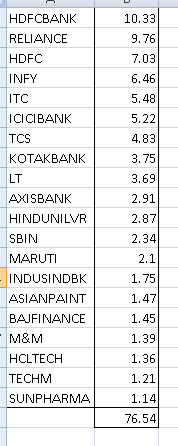

Top 10 companies by weightage cover 60% of the weight of Nifty

Top 20, cover 77%.

Therefore, in an attempt to get similar returns as Nifty 50, a retail investor can simplify his investment process by scheming around Nifty-20 alone.

PS: HPCL has 0.39% weightage.

1 Like

To invest in Nifty 50, one could take the ETF route. However, the next step in optimizing investment is fairly intuitive:

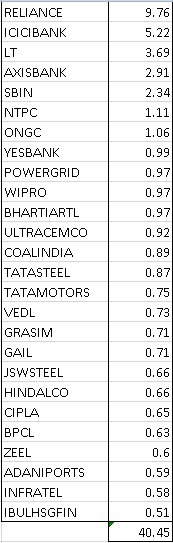

One could separate out non-performers, out of Nifty 50. Here is the list.

This 40% have been the laggards for obvious reasons. They are either asset heavy, PSU, Cyclical, issues with Ethics or plain simple slow.

I can confidently say that the rest of 60% are growth stocks. If India has to grow, if Nifty is to touch 20K, then not without these 60% companies leading the march.

Attn:

@ChaitanyaC

@deevee

4 Likes

But these are exactly the low PE stocks in Nifty so after forever arguing against investing in Nifty at high PE, are you now saying one should pick even higher PE stocks from Nifty for investment purpose?