Updates to the Gloom & Doom Report By Your Friendly Bear.

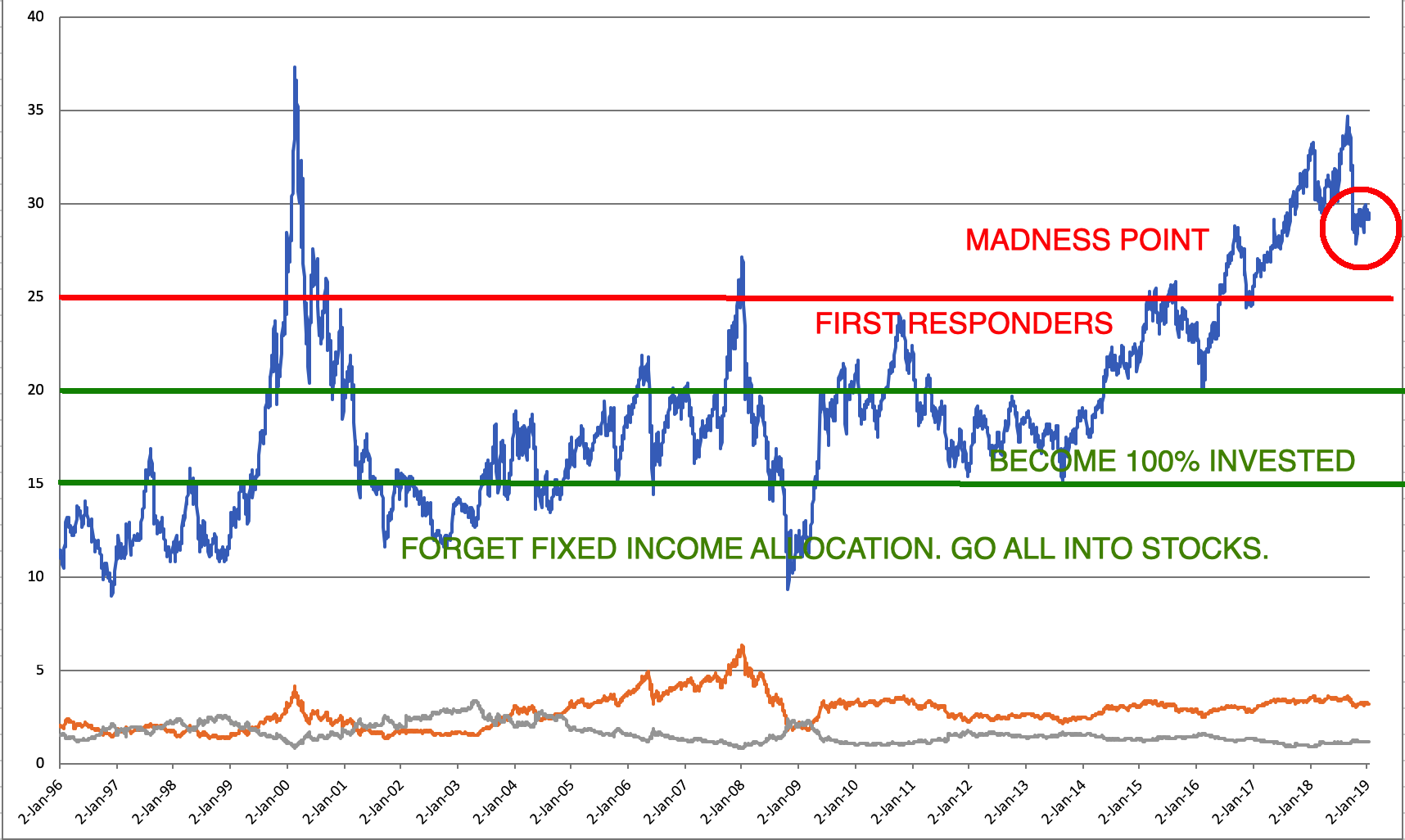

The markets are still very overvalued. The chart below is the current updated Nifty 500 as it stands as this week. Yes, it is 23 years of data you are staring at.

As you can see we are still at madness point for the entire stock market (Nifty 500 no less, not just 50 stocks of the Nifty). The full downloadable sheet is attached at the bottom of the post.

I feel the October 2018 drawdown got in the extremely early birds. When (not if) the Nifty 500 goes below a multiple of 25 I think we will then get the first responders.

Only after that it will drift down to below 20. That is where I will use my fixed deposits which are meant for allocation to stocks.

However, there is some good news. The whiplash of 2018 has removed the froth (though that does not mean upside has arrived) and since the froth is removed, very good stock pickers may have a good year; this today’s market is a market only for professionals, make no mistake about it.

Idiots like me should and will stand and watch from the sidelines, and directly speculate with interest income, if at all. Else, hand the job over to a professional you trust.

I would also not take advise on whether I need a haircut from a barber. There are many fund managers who are going on TV and claiming things like; on a market cap to profits ratio we are cheap, election years the index always goes up etc etc… See, we are private investors and we need to be clear in our minds on what is reality; their jobs depend on saying these things, I am for sure not listening to the barber. Each one has to decide if they want to listen and put their future at stake without using their mind to come to a conclusion. Best if we all came to our independent conclusions.

This post is just a friendly nudge to wake up and smell the coffee and realize what one’s skill level is. If skilled and you know what you are doing, one could do ok, but if not, it is said for times like these that “If you don’t know who you are, this is an expensive place to find out"

This year 2019, independence of thought and action will be very valuable.

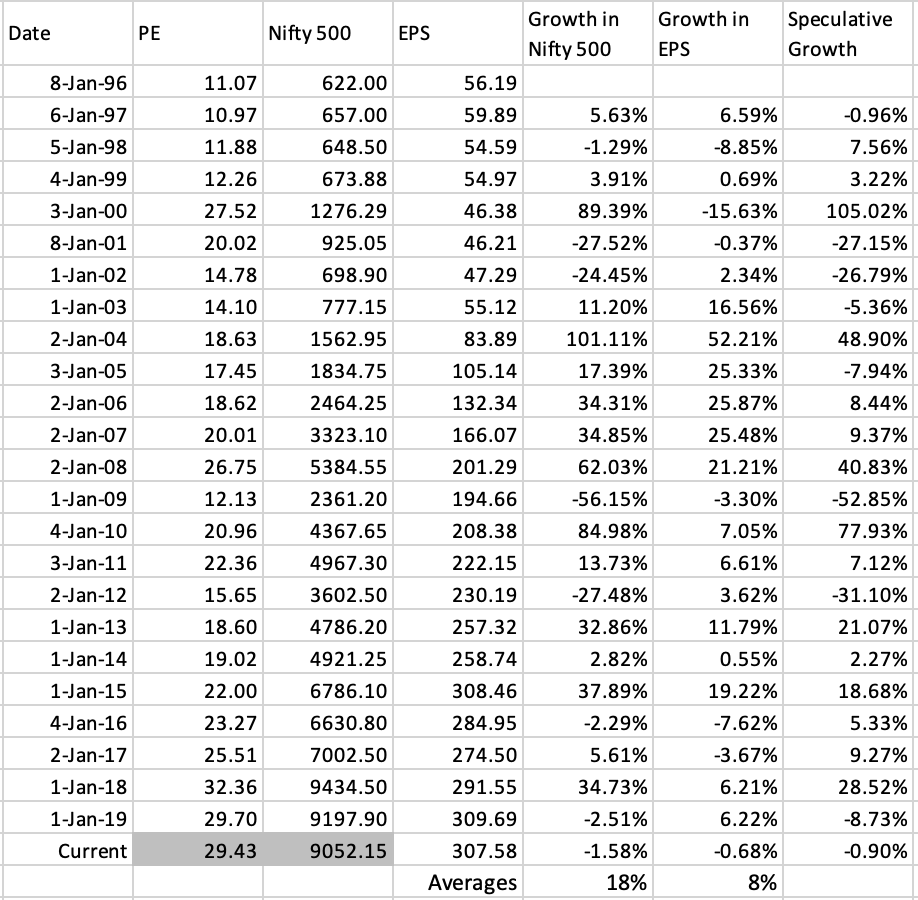

Please find below the valuation model from Mr Parag Parikh updated for Nifty 500. (Also part of the excel)

Happy investing. Be safe.

1996-2019.xlsx (351.7 KB)