You mentioned

ok, if you could just expand on “The current redemptions are now crossing 50%”.

Thanks

You mentioned

ok, if you could just expand on “The current redemptions are now crossing 50%”.

Thanks

That is the information I have seen. That is why I mentioned one can find out oneself. Don’t ask me for source  . Not that it is secret; it is in the public domain. Please seek it yourself or ask your mutual fund to provide the information to you.

. Not that it is secret; it is in the public domain. Please seek it yourself or ask your mutual fund to provide the information to you.

PS: I hope it is understood that I cannot name any particular fund here as it is not right, hence my hesitation in taking a name.

@valuestudent

Totally agree with you. Patience is instrumental for success. Many thanks for sharing your views. I appreciate it very much.

@valuestudent At last, the wait (& feeling of despair) is over. Great to see NIFTY 10K once again! I am excited, however not ready to buy yet. Not sure if we are in the “happy zone” yet.

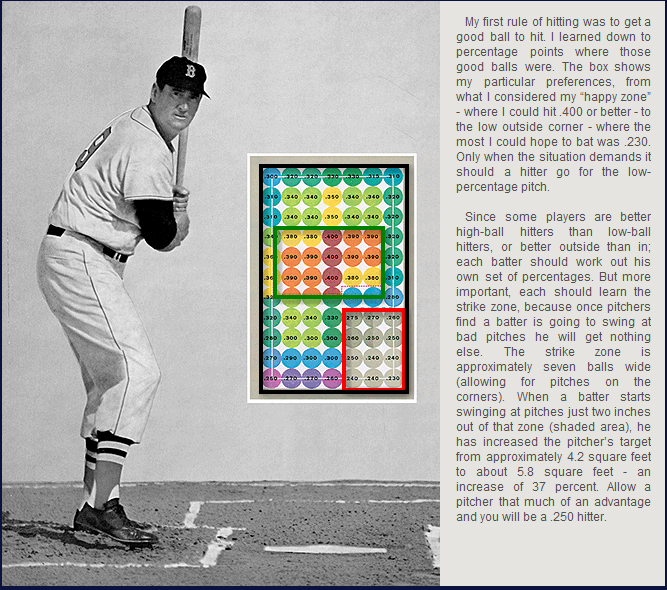

@vasuadiga Very well said and a great image. Waiting for the fat pitch.

Happy zone awaited here as well, fingers crossed for a super shopping zone. When the signs say… fire sale!

Best of luck and happy pickings.

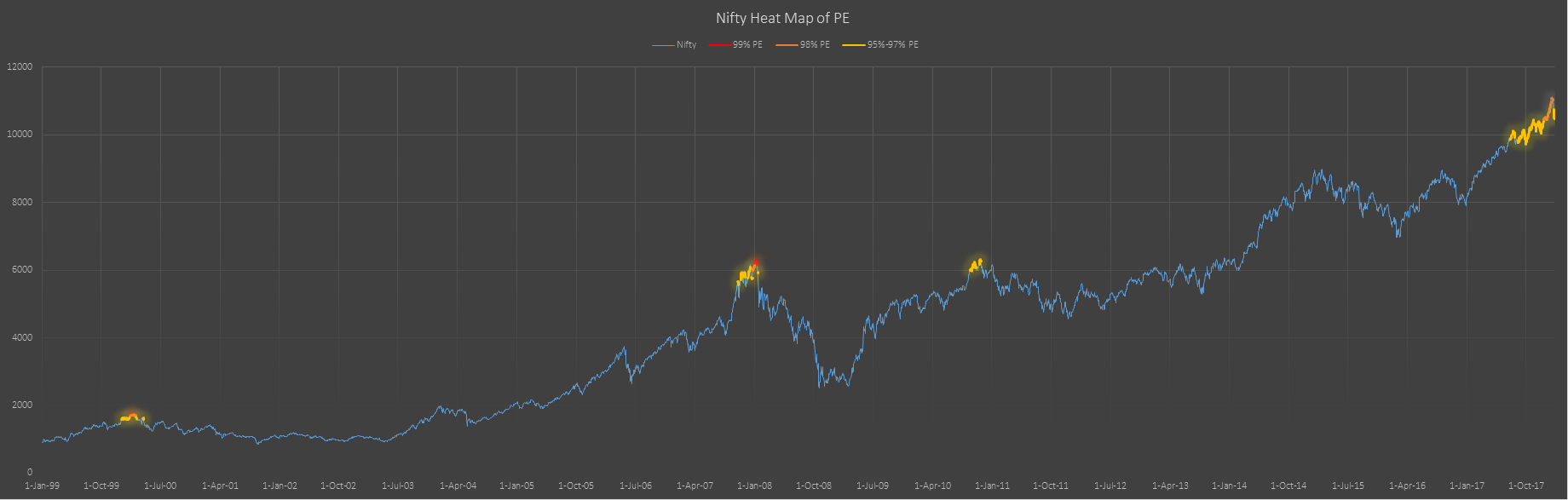

Please find attached the current Nifty 500 PE data. Hope it is helpful.

Even after the recent fall, the current Nifty 500 PE is still higher even than 2008 peak. That means in general stocks are valued very high to their earnings on the top 90 percent of the entire market cap.

This says a lot about the psychology of buying high. Just because they look lower does not necessarily mean that are now cheap or even fairly priced. This is only on a entire universe of the Nifty 500 level.

Some individual stocks if not cheap may be at close to fair value.

1996-2018.xlsx (218.1 KB)

Hi

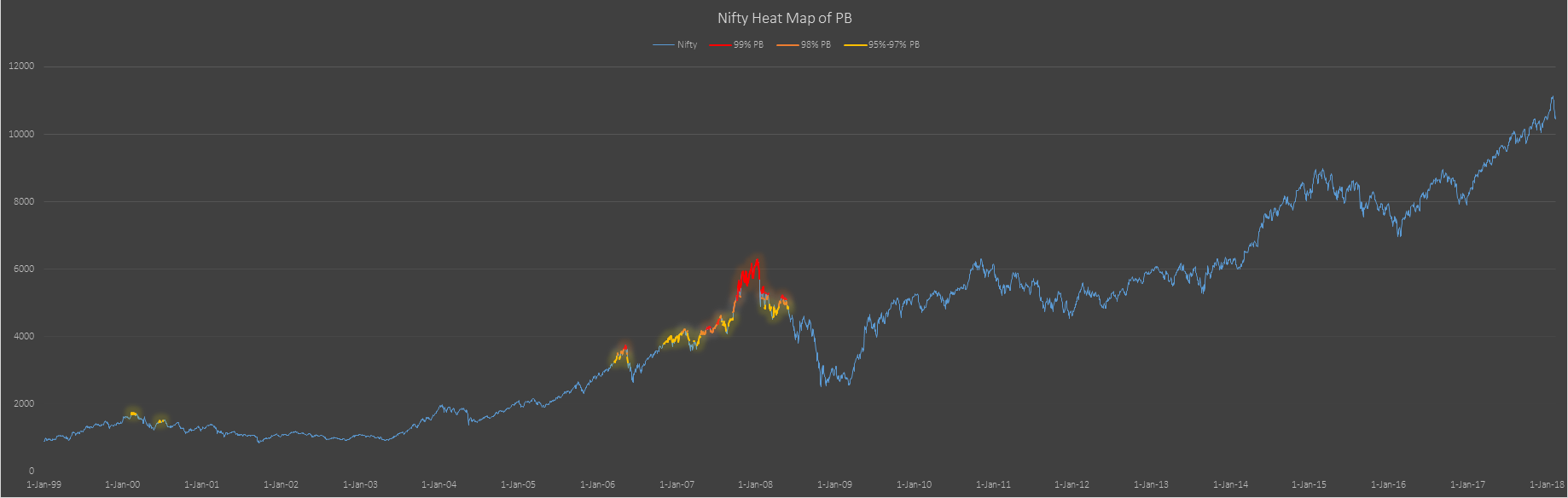

Well to put things into visual perspective from a Nifty50 PE and PB pov we are not currently in peak zone compared to 2008.

Rgds

Hi @deevee

Thanks. Do you mean if we consider BV as well?

I personally have always chosen to ignore the BV for two reasons:

a. The BV as far as I know is really only valuable for financial businesses. The BV of most if not all non financial companies does not say anything about their real value. An example would be lets say… Nestle.

b. It distorts a pure earning and multiple relationship when other data is thrown into the mix of looking at the PE multiple.

Just my 2 cents. Please do help me understand if my logic is incorrect on totally ignoring BV.

Hey

No I don’t mean to consider BV together. Just to give a view Of shared this that’s all. Its the PE we should be focussing on.

Agree with you.

Rgds

Ignoring Book value is a bad idea and saying book value is only valuable to financial businesses isn’t correct IMHO. First lets understand what goes into book value. The main components are fixed assets (plant and machinery) and cash and equivalents. Fixed assets are what generate your revenues. Some companies (like nestle as you mentioned) have better asset turns where they can produce 5x revenues from their assets. Some companies are not so lucky and have large assets but generate only about 0.5-1 times their assets’ value as revenues (say Inox Wind or most companies in the Cement, Power, Steel sectors).

If you take an individual who works in IT and freelances, his fixed assets could be his house, car, bank balance, FDs and his laptop altogether worth a few Crores. In this only his laptop generates revenues and his asset turns from a 1 lakh laptop could be 1 crore. In this case although overall asset turnover may not look good, his actual plant & machinery is just the laptop and on that basis asset turnover is great. For an individual, non-income generating assets are not really assets at all but that’s a discussion for another day. Now if this person loses his job, his fixed assets still remain. If you value this person based on his earnings, what price multiple would you give him? Will you give him zero if he is without a job for a year or will you value him based on his assets and/or will you give him a chance to get another gig?

The critical thing to look for is capacity utilisation. This is going to depict the asset turnover. There is a maximum possible asset turnover when the capacity utilisation is 100%. Currently capex cycle is depressed because most businesses have unused capacities and are waiting for demand to pick up. Valuing these businesses based on current earnings and ignoring unused capacities is not a good idea unless you think the economy has reached saturation and no fresh demand is possible. This is where book value comes into play again. In 2008, P/B reached peak valuations while the capacity utilisations were peaking but currently we are at lower P/B and lower capacity utilisation both of which point to possible topline growth, margin expansion and profit growth when the demand picks up (When and not If, IMHO).

Now coming to P/E - It tells different stories for different businesses. For a commodity company like IMFA trading at a P/E 3.59 and a P/B of almost 1, it tells one story and for Nestle at 61 P/E and 18 P/B it tells another and for DMART at 115 P/E and 18 P/B it tells quite another and for several loss making companies with an indeterminate P/E and positive book value and positive cash flows over a complete business cycle - something else. On top of this there is the problem of P/E numbers in NSE which doesn’t seem to include consolidated earnings. With so many faults built into the model, there isn’t anything coherent that you can read from a index P/E or P/B although you can derive some rough estimations of valuations but this is in no way going to correlate to a high degree with individual company’s valuations so it might be worthwhile to dissect individual company’s valuations here than try to read anything concrete from index P/E and P/B.

Dear @phreakv6. Let’s see what is the most important thing that Peter Lynch tried to teach us. I don’t remember him teaching book value as a consideration (outside special situations) and for sure not asking us to ignore the PE etc.

As per Mr. Lynch and his advise is very simple advise is as below. According to me, the mistake is that when nothing is available within the below parameters, then it is sad that people invent future growth and reasons why it will happen etc.

I have always found it funny that whenever I have said that the markets are expensive, and that it will sometime play out, I am told you cannot predict; but then everyone predicts earning growth is coming, which never seems to come. Is this not a classic cognitive bias to what people believe to be true, in-spite of all evidence to the contrary.

So finally, after my rant above, here we go:

Peter Lynch.

“The P/E ratio of any company that’s fairly priced will equal its growth rate … If the P/E of Coca-Cola is 15, you’d expect the company to be growing at about 15 percent a year, etc. But if the P/E ratio is less than the growth rate, you may have found yourself a bargain. A company, say, with a growth rate of 12 percent a year … and a P/E ratio of 6 is a very attractive prospect. On the other hand, a company with a growth rate of 6 percent a year and a P/E ratio of 12 is an unattractive prospect and headed for a comedown.”

“In general, a P/E ratio that’s half the growth rate is very positive, and one that’s twice the growth rate is very negative.”

End of Quote.

So being the above, who does not understand that stocks are headed for a comedown?

Where is the rush? Why should I not wait to see 1-2 quarters of growth before I commit? If the growth will come will it be for only 1-2 quarters? No right. Then I can see that we have moved to that trajectory. I can invest then.

Currently the trajectory is clear as well. No growth generally, and where there is in some stocks, just until recently it was not fitting within any of the parameters above. Even now, not really and this is clearly reflected in our index.

There is a further slightly more complex calculation that Mr Lynch advised. This is also clearly useful and actually one that I prefer to use.

“A slightly more complicated formula enables us to compare growth rates to earnings, while also taking the dividends into account. Find the long-term growth rate (say, Company X’s is 12 percent), add the dividend yield (Company X pays 3 percent), and divide by the P/E ratio (Company X’s is 10). 12 plus 3 divided by 10 is 1.5.”

“Less than a 1 is poor, and a 1.5 is okay, but what you’re really looking for is a 2 or better. A company with a 15 percent growth rate, a 3 percent dividend, and a P/E of 6 would have a fabulous 3.”

My point remains the same. Can we find clean stocks with decent managements that fit the above parameters. Till Jan this was no more being even thought about, now I believe some stocks might start falling in this net sooner or later. Till things start fitting into this or a few more models, mostly cash is my opinion. I don’t want to argue with Mr. Lynch and his knowledge. I know there are many superheroes, I regrettably am not one and can’t see the future. But I can see the present clearly where many people had lost their sensibility when making stock purchases. This reminds me of Charles Mackay.

“Men, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, one by one.”

― Charles Mackay, Extraordinary Popular Delusions and the Madness of Crowds

Now it seems to me that people will slowly recover their senses, one by one.

I remain truly yours; a friendly bear.

Just sharing my thoughts. Please excuse my naivety.

Growth investing and value investing, the branches of fundamental investing, both have their loyal, devoted practitioners. And, we, as practitioners have some deeply rooted beliefs, biases about our investing approaches. It’d be futile to try and convince the other one to switch his/her allegiance from one branch to the other. On the contrary, it reinforces our beliefs. Different strategies have worked at different points of time. When a strategy will work is hard to tell. But, what’s certain is lower returns in the years to come.

Yet again, my intention isn’t to stoke a debate.

Dear Shreys. I was way more naive than you will ever be when I joined this forum ![]() . I have leaned most of the stuff on VP and also by reading books and trying to understand what they explained. I am sure you are way smarter than me and will do better.

. I have leaned most of the stuff on VP and also by reading books and trying to understand what they explained. I am sure you are way smarter than me and will do better.

You are right, growth and value are different schools. What is funny is recently we have had a new school of thought added to investing styles in 2017-2018. It is called Hope Investing ![]() Now it seems it might have been a fad and growth and value investors can go back soon to their old battles. But team hope investing must first disappear back into fixed deposits.

Now it seems it might have been a fad and growth and value investors can go back soon to their old battles. But team hope investing must first disappear back into fixed deposits.

I’ve been following this thread ever since I’m on VP forum. I seriously would like to know why you are always a bear ![]()

@manivannan.g See my profile photo. What do you think I look like  It is my real photo.

It is my real photo.

No really, I have only become a bear since last 9 months. I am waiting for my bull family to convince me I can come back to my family camp but I refuse to come back till they show me a screen full of stocks with my parameters. I am tired of playing special situations and turnarounds. It is very risky.

Regards.

I guess Nifty has adjusted for higher interest rate. PE is absolute term does not mean much unless seen in context of interest rates. So logically , stocks have not become any cheaper.

PE can be misleading. Facebook PE at $50 was 180 and at $180 it is 20. If one just focused at high PE one would have never bought. Courtesy FT

With due respect, that is case of hindsight bias and survivorship bias. Two biases in one. If one knows what will happen to which low profit making business at that scale at which earning growth happened in Facebook then one need not even buy a second stock to diversify.

Taking examples of survivors is dangerous.

Not all high P/E stocks are going to justify growth and not all low P/E stocks are value buys. We might do a lot better as investors if we don’t use P/E as an initial screening parameter but as one of the many final screening parameters.

I have nothing more to add  . As said Mr Munger.

. As said Mr Munger.