My understanding is Natco will receive a part of profit (20% and 50%) from Mylan. If there is no profit, there would be nothing to get for Natco. I would expect Any profit calculation would be after all costs such as litigation.

2 Likes

Mylan has exclusive rights for Glatiramer Acetate in several key European markets, including Germany, France, Spain and the U.K.

Mylan is partnered with Synthon, the developer and supplier of its European Glatiramer Acetate Injection 20 mg/mL and 40 mg/mL products

Not sure if this news item has been picked up

@MONK88888 Thanks for sharing. How is this relevant for Natco?

But Matlan is partnered with NATCO for generic version where litigation, marketing part is with Mylan and research part with NATCO on profit sharing basis. I don’t understand this new fact that Mylan is partnered with Sython. Patent is with Teva. Can you elaborate it please. Sorry to ask silly question.

I wanted to highlight that only US supply deal covers for Natco and the EU deal is with Synthon. So its not across all markets as I initially presumed-just wanted to clarify to other boarders.

I presume I have answered Rajesh 1975 query as well

For NATCO -Mylan covers the marketing & litigation related areas for US

For Synthon-Mylan has exclusive distribution rights for products in EU / Denmark / Norway / Finland / Cyprus / Malta & Switzerland(27 EU/EEA member states)-this is for the popular 40mg/ml

Also Synthon has apparently partnered with Pfizer for commercialization in US

2 Likes

Teva & yeda (drug innovator) hold the patent which is now being appealed at US courts of appeal.

There are five other filers : Amneal , Sandoz/Momenta , Dr.Reddy, Synthon & Biocon/Apotex

From litigation point of view , Natco was removed from the chargesheet by Teva/Yeda

for Sandoz/Momenta (US approval to launch ) the manufacturing of the drug is by Pfizer (which is having FDA issues on factory) whereas Synthon marketing partner for US (40 mg/ml) is Pfizer

I am not sure if I am aiding or adding to confusion

More information about ‘At Risk Launch’ philosophy

My notes from Natco AR 16-17. MDA section is very insightful to understand where the Pharma industry is heading towards between Developed market and Developing markets (they call it Pharmerging).

Comparing between this AR and last years AR, messaging is very pronounced. Only niche drugs, if any, to US. (same was evident in Q3 concall where they had provisioned/expensed decent amount as contract termination fee to partners) where the product was no more commercially viable to them.

Four subsidiaries (Brazil, Australia, Canada and Singapore) will be growth engine for them in the Pharmerging markets.

Steady focus on India Oncology segment where they are a strong player. Intent to expend the BMT portfolio.

• In a volatile and uncertain world with a new wave of protectionism, businesses need to constantly recalibrate their strategies to survive headwinds and thrive. The pressure of change is perhaps more pronounced in the global pharmaceutical sector, where the regulatory landscape, competition, channel consolidations, emerging patient needs and technological breakthroughs drive industry players to think afresh.

• During the year, we observed that the industry environment in most developed countries was turning towards uncertain times with higher barriers for entry. We decided to intensify our strategic focus and resource allocation towards India and other emerging economies where we can lead in many therapeutic segments while staying on course with our US strategy. This shift in focus, we believe, is critical for our long-term sustainability.

• Brazil Subsidiary: Backed by a strong portfolio of Oncology products we expect to file niche products in the year 2017 along with a value speciality-driven product pipeline for strong non-retail participation in local tenders (Brazil) and major tenders like PDP to follow for the years to come.

• Use Capital Prudently, Maintain A Strong Balance Sheet, And Return significant Capital to Stockholders.

• As part of our wider strategy, we launched India’s first generic Bone Marrow Transplant (BMT) product, Thiotepa, as we intend to build a full fledged BMT portfolio.

• Target to launch 10+ products across all three domestic business verticals .

• Focus more deeply into niche molecules for the US market

• Pharmerging markets:

The spending of pharmerging markets is expected to grow at 6.9% CAGR from $243 billion in 2016 to $315-345 billion by 2021. Amid uncertainties in the US market, the pharmerging markets have been bright spots in the pharma landscape. These are high-growth markets with robust macroeconomic drivers and have achieved steady growth, despite price controls and currency fluctuations. In the pharmerging markets, the growth opportunities in the branded generics segment ensure a sustainable and predictable revenue prospect over long periods.

Disc:

Invested for some time now and had transactions in last 60 days.

Regards,

Tarun

10 Likes

5 Likes

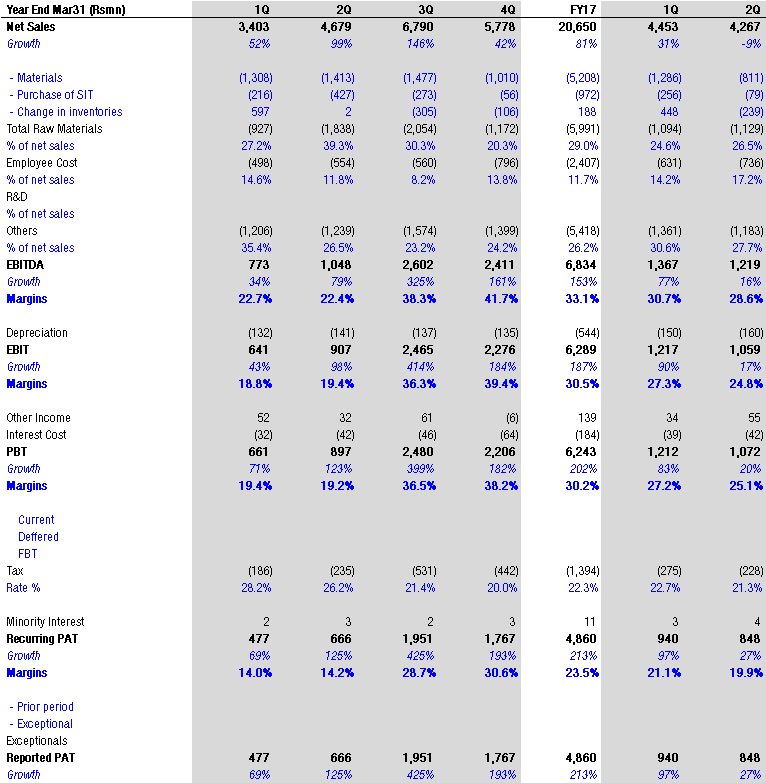

Important note along with results as provided by natco management

The company had a one-time exclusive launch of generic oseltamivir during last year’s period.

1500 cr fund raising by natco can anyone tell are they at premium to floor prices and how management is going to use it @T11

Natco Pharma: Alvogen to market generic equivalent to oseltamivir phosphate in USA

Natco’s marketing partner Alvogen first to market generic equivalent to oseltamivir phosphate powder for oral suspension in the USA.

Any thoughts on why raise money via equity? They have 1600cr in cash, so a total of 3000 cr? What are they planning to do with such money, I really hope they dont get into solar farms

G1

3 Likes

Mylan said it took a 16.2 percent share of new prescriptions and around 8 percent of total prescriptions.

1 Like

The analyst in this article estimates $250m revenue and $80m profit per quarter for Mylan. Assuming average 40% profit share to Natco, looks like $50m profit per quarter, at least for the remaining two quarters of FY18 is possible?

http://www.markets.co/mylan-inc-gets-a-buy-rating-from-mizuho-securities-2/117201/

Any views?

1 Like

Some Notes from Q1’FY18 Con call and Investor presentation:

Hepatitis C Franchise: Worldwide, Hepatitis C market was estimated to be ~$11.81bn in 2015, which is expected to grow at a CAGR of 15% to reach ~$27.63bn by 2021. Registrations filed in 40 countries and import permits and approvals received in 10. Key focus area is Philippine region. Domestic market has expended rapidly and they are number 1 with recent launches like Velpanet, Epclusa etc. however the segment is now short of stagnating on pricing front though volume growth is there. Evident from segment revenue:

![]()

RoW Subsidiary: Will primarily be about Hep-C and existing portfolio of Onco. Good uptick in short duration of time:

Canada - Filed 15 products with 11 approvals

Singapore - Filed 10 products with 5 approvals

Brazil - Filed 10 products with 5 approvals

Revlimed: is a BIG opportunity. A follow-up query to be answered to FDA. Expecting approval in FY’18. Possibility of early launch (under certain conditions) from FY’19 subject to other competitor product arrive in the market.

API: Recent capacity expansion to significantly improve API capacity. Even otherwise API export is growing at a faster pace from 212 MN USD on Q1’17 to ~800 MN USD by Q1’18.

![]()

Copaxone: Natco feels that Mylan will most likely will go for at risk launch since legal position is very strong. Though one PTAB hearing is still pending but company is positive about outcome.

brand sales for the 20 mg/mL dose of approximately USD 700 million and for the 40 mg/mL dose of approximately USD 3.64 billion for the 12 months ending July 31, 2017. Natco will receive 30 percent profit share from Mylan for the 20 mg product and 50 percent share for the 40 mg product.

Edelweiss projections: We were expecting launch (of 20 mg product) in Q4 FY18 (Jan-Mar) with USD11 million of revenue (for Natco) in FY18. Given the earlier-than-expected launch, this could now contribute USD 25 million-USD 30 million in FY18 and around USD55 million in FY19,” Edelweiss said in a note. “For the 40 mg product, the launch is likely to be in the second half of fiscal year 2018-19 due to certain patent issues. This product could contribute USD 125 million to Natco’s

FDA Approval status:

Export formulation facility Kother: Approval received in Jan’17.

Export formulation facility Vizag: Under development

API facility Mekaguda: US FDA approval Jan’15

API Chennai – US FDA Feb’16

New verticals: New C&D vertical will focus on niche products. First of kind types. So far 3 launches with more in the pipeline. Overall 10 Products targeted to be launched in FY18E (this number covers both domestic and Export formulation).

Fund raising: Fund raising of ~1,500 Cr. By cometary, they are very very clear not to pursue any me-too generic opportunity with the changing time. Rather would prefer to invest for complex generic where gestation period is long however the windfall more than well offset for the effort worth. Those opportunities may be in the area of Novel Drug Delivery Systems (NDDS) or complex chemistries. Will NOT go for Bio-similar/biological etc. Subtle expectation setting for beyond 2024-25 for complex generics.

Are there some surprises in store with the fund raising? Existing balance sheet is getting better riding on Hep-C, Copaxon etc profit flow. The cash flow is expected to improve further with Copaxone effect trickling in for full year in FY’19. On the other hand, Rajeev specifically commented that CapEx projection is for ~350Cr. only for FY19. Putting these two together, I am speculating that the fund to be used for some big ticket acquisition. Nirmal Bang security speculating about possibility of acquisition in the complex Onco space.

Any Natco experts got any insights/view specifically on the proposed fund raising of ~1500 Cr and implication of the same.

Thanks,

Tarun

Disc: Invested

11 Likes

Though amount is not really big however hoping that management don’t get drawn into trivial things.

1 Like

Also mystery behind 1500 cr capital raising is not giving comfort. We have to understand capital allocation plan.

Disclosure -Invested

1 Like

Revlimid news update

http://www.ipwatchdog.com/2017/11/21/celgenes-new-revlimid-lawsuits-shows-shifting-tactics/id=90357/

can any expert in pharma patents analyze its effect

1 Like

Some speed breaker on thriving domestic Hep-C franchise for Natco.

Sofosuvir+velpanet prices set at ~15500 AGAIST current 18,500. More than 15% haircut

Hep-C, Cancer and Hemophilia drugs to cost less as regulator caps prices of 51 formulations

The new price caps are likely to hit many Indian drug makers’ domestic formulation businesses

Also, I suspect some oncology products also in purview. Anyone got a Chace to see the most recent notification? We can assess the impact by comparing notified price vs. current MRP (can find current MRP from NPPA site:)

3 Likes