In Gold loan financier has the upper hand by holding 40% remaining gold value with him, Hence from client point of view he needs to be trusted party to give 100 rs worth of goods and take 60 rs as loan. Simple.

Q1 FY21 results are in. Considering the Covid related challenges, they seem to have done fairly well.

Consolidated PAT is at 857 Cr, up strongly by 52% on YoY basis. Sequentially on QoQ basis, its up marginally by 2%, which in itself a significant feat, given the covid storm. There seems to be some negative impact arising from hedging.

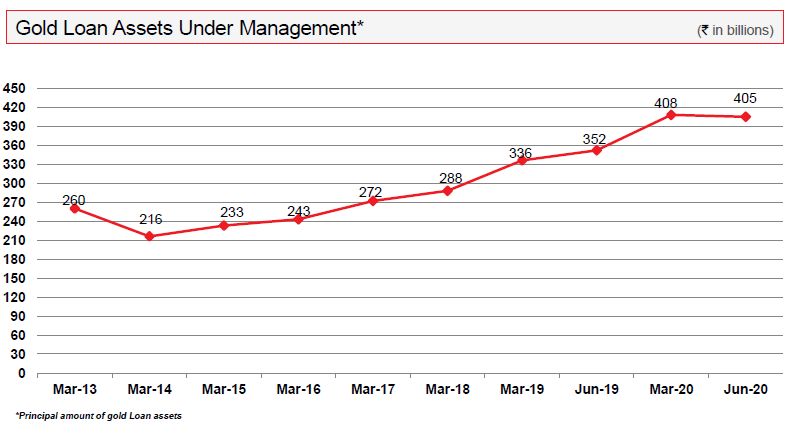

Though the Gold Loan AUM has shrunk marginally, from Rs 408 billion to 405 billion, its not had any impact on the bottom line, reflecting that margins / efficiency have been improving.

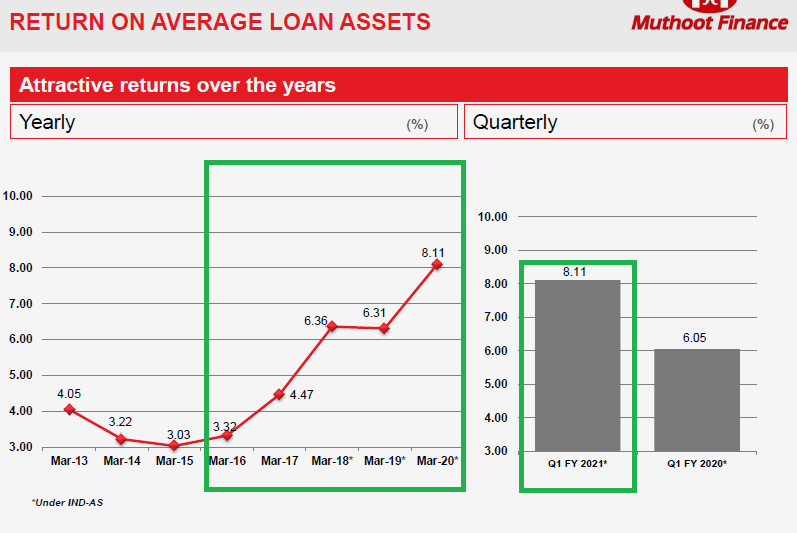

But the true cornerstone of Muthoot’s performance over last 3-4 fiscals has been its NIM and Spread, and they have continued to do well on that count

Cost of funds has been squeezed consistently, while their loan interest rates to customers have been rising, realising generous spreads.

Delinquencies continue to be well under control, and the rising gold prices have only improved the margin of safety on the loans.

All of the key metrics above work together well to boost the RoA

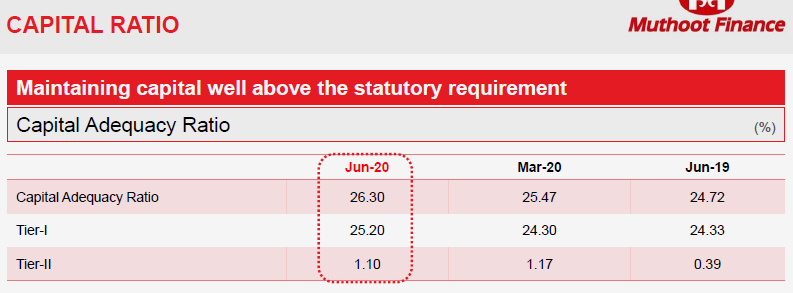

Capital structure continues to be robust. Net worth is steadily rising, statutory ratios are all healthy

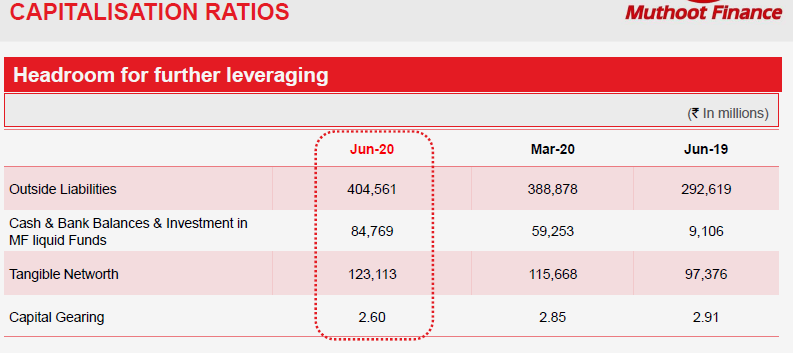

They had raised a big tranche of capital at the beginning of the year, and the gearing remains at one of the lowest in the industry.

With capital in hand, they can continue to press the pedal to boost the growth without taking too many undue risks. Though the stock has run up significantly over last 3-4 months, even now its available at decent TTM multiple of about 14.

Disc: Not invested, but actively tracking

4 Likes

Summary

- Underperformance in tonnage was because of lockdown as Customers usually visit branches to pledge their gold.

- Rollover concept does not apply for Gold loans.

- Major customers include SMEs, Kirana stores and small entrepreneurs who avail gold loans to restart their businesses as well as to stock up stuff for the upcoming festival season

- On track to comfortably surpass the 15% growth guidance for FY21. 15% is the worst case scenario

- Slightly pained by the step-motherly treatment for NBFCs wrt LTVs. But still feels LTV of 75% is optimal for this business. Even if RBI permits 90% internal risk metrics will not permit such high LTVs

- Difficult to take a call on subsidiaries now as they are struggling with collections like other companies. Focus is more on gold loans and 15% target is for gold business which contributes to 90%

- Will continue to work with 10% spread in the future (because gold loans are small ticket size and customers are not that interest sensitive) and as cost of Capital is down almost by 100bps, yield might also come down by 100bps.

- Expecting ROEs to stay at 25% in the upcoming years.

8 Likes

Sharing a presentation based upon my recent analysis, esp. taking into account the historical surge in Muthoot Finance share prices and the latest regulatory announcements…as I am intrigued by this unique gold loan business and plan to track it over long term.

Thoughts/suggestions are welcome! MUTHOOT FINANCE.pptx (1.6 MB)

8 Likes

Prof. Sanjay Bakshi recently presented one of his video lectures. It seems he is referring to Manapurram Finance here. Sharing as FYI.

9 Likes

Management comments / concall takeaways

#Management maintained its guidance of 15%+ growth in Gold AUM for FY21, while

maintaining cautious approach in non gold book. Expect Rs5bn of disbursement in MFI

in H2. Not doing any business in Home loan segment and hence expect book to de‐grow

in FY21.

# The company is comfortable on liquidity front (Rs78bn) and will continue to maintain

**higher cash levels in balance sheet. **

# Collection efficiency in MFI / Home finance / Vehicle finance in September at 86%/

84%/82% vs 76%/ 87%/ 75% in July.

#Opex saw increase led by higher rent expense due to payment of April rent during the

**quarter. **

# GNPA improved as company closed earlier contracts and entered into new agreements

at higher LTV. Auction during the quarter at Rs100mn.

5 Likes

Key Highlights for Sep 2020 Result Discussion:

- Consolidated Loan AUM increased by 29% to INR 52,286 Cr. for H1 FY2021

- Consolidated PAT increased by 21% y-o-y to INR 1,788 Cr. for H1 FY2021

- Standalone Gold Loan AUM for Muthoot Finance increased by 32% to INR 46,234 Cr. for H1 FY2021

- Standalone PAT for Muthoot Finance increased by 25% y-o-y to INR 1,735 Cr. for H1 FY2021

- Branch Network for Muthoot Finance increased from 4500 to 4600. Plan to add another 100-150 branches by this year itself.

a. New branches mostly outside Kerala

b. Plan to merge a few branches outside Kerala, due to insufficient prospects - Credit Losses have come down from INR 17 Cr. to 4 Cr. % of Credit Loss to Gross Loan AUM stands at 0.008%

- Avg gold loan/branch increased from 7.7 Cr. to 10.04 Cr.(30% increase)

- No. of Gold Loan accounts have decreased from 81 lakhs to 76 lakhs y-o-y

- Total Gold weight tonnage has decreased from 171 Cr. to 163 Cr.

- Avg Gold Loan ticket size has increased from 43% to 61% LTV

- Employee count steady at 25,000

- This qtr. Has seen the highest ever Q-o-Q gold loan AUM outstanding - Delta of 5,739 Cr. is the record growth for the company

- Avg. Gold Loan Outstanding/Branch crossed 10 Cr. – Big milestone

- 92% Q-o-Q growth in branch footfalls

- 50% Q-o-Q growth in mobile app transactions

- 103% Q-o-Q growth in online gold loan disbursement

- Loan at Home services crossed 100 Cr. disbursement this October, 2020.

- HNI Loans above 10 lakhs grew by 229%

- Disbursals this quarter was focused on New customer addition, Fresh loans to Active & Inactive customers and top up of loans to existing customers

a. Disbursed fresh loans to 4.4 lakh new customers, amounting to INR 3363 Cr.

b. 4.67 lakh inactive customers amounting to INR 3460 Cr. (inactive - not having loan at the beginning of this qtr.)

c. Even though total number of customers are not increasing, a lot of churn is happening within the customer base. This is significant as gold loan is a very short term loan - 66% of loans are repaid back in the first 6 months

- Maintained Liquid buffer of 7,846 Cr. in the form of cash & bank investments, as of Sep 30th, 2020.

- Non Gold Loan portfolio constituted about 11%(from 13%) of the total loan AUM

- Collections in gold loan portfolio significantly improved m-o-m after COVID

- Mgmt. confident of annual Loan growth to exceed 15% supported by good offtake of gold loan even in Oct, 2020. Firm has already achieved 14% increase by October.

- Maintaining sufficient liquidity and access to new funds to support the significant increase in gold loan aum

a. Recent NCD Issue of 2000 Cr. to the retail has been fully subscribed

b. Started Market link Debentures

c. Bank Loan constitutes only 41%(from 47% a year back) of total borrowing.

d. Increase has come from NCDs(constituting 47% from 31% a year back)

e. All the above shows that the firm has been able to diversify its funding mix, and reduce its over-dependence on banks - Need to maintain a Higher liquidity to meet any uncertainties and support the increased loan demand

- All branches are now open after COVID

Questions by Analysts: - Decline in Gold Tonnage for the past 2 quarters? New Loans are getting priced at the new LTV/gold value and the new gold value is currently higher. So, for the same loan amount, the borrower needs to pledge less gold ornaments. This leads to decline in tonnage growth. However, this doesn’t have any impact on the profit as the profit is solely dependent on the gold loan AUM and that has seen continuous growth.

- Cost of funding for borrowing is 9%. However, it should come down in the 3rd quarter as a lot of churning of funding sources happened this quarter, esp. public issues of NCDs.

- Incremental LTV disbursed during this quarter – 70%

- Reduction is Stage 3 assets mainly due to customers paying the interest and refinancing the loan at the new LTV due to higher gold loan prices

- Very negligible auctions this qtr. – approx. 10 Cr.

- Any Plan for rapid Branch Expansion - Mgmt. more focused on increasing per Branch business, rather than sheer branch count to optimize costs and increasing operating leverage

- Plans for MFI & Housing business?

a. No significant disbursements for Housing finance; present focus is on collections – Flat or little de-growth this year

b. MFI has started lending post COVID, plan to grow about by 500 Cr. this year - Penal Interest Amount – Not material, as penal interest comes only after 12 months and very few loans cross the 12 month time period

- Rent Cost Higher this qtr. – In April, company withheld some rents as offices were closed; thus, paying the April rent this quarter has led to an increase in rent costs

- Any difference in the end use of gold loan – Majority for agricultural & trade purposes; only 5-10% for domestic use

- Increased competition – Competition may be a bit more intense as banks have also started advertising heavily; however, overall market pie is increasing as well as more & more people are availing gold loans.

- Firm comfortable at 75% LTV max. LTV comprises of only Principal; Interest accrued is not included within LTV. Interest might account for an additional 2% of LTV

- Interest Cost rises by 38% but interest income rises by 19% only - The positive effect of additional interest income and reduced finance cost will be seen in the 3rd quarter

- The count of 48,28,505 customers does not include any inactive customers; all of them have an active loan as of Sep 30th, 2020.

- Gold Prices going up or down doesn’t have much impact on the loan size, as that depends on the needs of the customer.

- Cost – Cost of Operations are under control; however, firm gives a lot of incentives to its staff. Rent and other costs, incld. staff costs, goes up approx. 6% every year, due to inflation. Opex in 2nd quarter is around 4%. This has always been the case and will remain stable at 4-4.5%, going forward.

- Collection Efficiencies in the Non Gold Loan Portfolio – 84% in Muthoot HomeFin, 93% in personal loans, 82% in Vehicle Finance, 86% in Belstar

- Total Funding raised in Q2 – 4,133 Cr. of fresh funding

- Limit of per Branch business – Highest per Branch is approx. 25Cr. 10 Cr. is avg. business/branch

- A better offtake for gold loan this year is due to other non gold/conventional loan providers becoming more conservative in restricting such loans/reducing loan ticket size to the public. Mgmt. feels that this demand will continue for a longer time, even when economy picks up.

- Plans to reduce interest rates to acquire more customers? – Firm policy is to keep the Interest Margin intact. Thus, only when cost of fund comes down, the lending rates are reduced.

- Comfortable unwinding the surplus liquidity on balance sheet – Its an ongoing process and firm wants to maintain this liquidity level going forward.

- Why would customers requiring a bigger loan come to Muthoot instead of a bank whose interest rates charged are much lower – Primarily because of comfort, convenience & reach; not all branches of a bank offer the same set of loan portfolios throughout

- Gold Price Fluctuation Reserve – This got merged and is not accounted for separately during transition to IND AS. However, a provision of 295 Cr. is maintained separately over & above the ECL. All provisions put together exceeds 1000 Cr. Although, mgmt. feels strongly that these provisions are not essential for a gold loan company due to the security of the gold ornament collateral.

20 Likes

With the Farm Bill coming in there will be a drastic change in the understanding and reach of the small farmers, this can be a Big Negative for Muthoot Finance as these farmers will now be in direct connect with various corporate houses.

1 Like

That is an interesting point; Yes, there may be an impact and we have to keep a close look on the same. However, Muthoot trying to venture into the urban space with new gold loan monetization schemes and online disbursal may hopefully help to offset the agricultural impact.

The other contention is that the trade part will grow when the economy improves and esp. with more entrepreneurial initiatives in the future(boosted by the ‘Make in India’ initiative). This may encourage further demand of gold loans.

1 Like

Related Party Transactions:

1 Like

Muthoot Fin should consider buying out the South Indian Bank for bootstrapping the banking operation as the latter is now available at a very affordable valuation! … a win-win transaction certainly.

Valuation is just one of the many parameters for an acquisition. They also have to look at the profitability of the underlying asset, strategic fit, cultural fit, and sources of funding, to name a few.

3 Likes

1 Like

https://www.icra.in/Rationale/ShowRationaleReport/?Id=99758

Rating sensitivities

Positive triggers – ICRA could change the outlook or upgrade the rating if MFL demonstrates a track record of good quality and profitable performance in the non-gold asset segments while limiting the share of the unsecured asset segments to 15% of the overall AUM. A sustained asset quality, capital profile and earnings performance, as per the expected levels, would also act as positive rating triggers.

Negative triggers – ICRA could change the outlook or downgrade MFL’s ratings if the asset quality weakens significantly, thereby impacting its earnings, or if the consolidated gearing increases beyond 4.5 times on a sustained basis

2 Likes

I have a couple of basic questions (not sure if these have been asked earlier).

- Is there an annual/semi-annual audit of (a) the gold reserves and (b) safety measures in place, by an independent third party?

- Does the Muthoot gets the gold jewellery insured to prevent against any liability due to damage/theft?

Investment status - Invested in FY20 NCDs of the company

- Yes, the gold holdings are insured.

1 Like

2 Likes

Muthoot Finance Q3FY21 Concall Highlights:

- Crossed the 50,000 Cr. of Gold Loans for the first time – Big landmark

- Standalone Gold Loans stood at 50,391 Cr., whereas Total AUM stood at 55,800 Cr.

- Muthoot Finance AUM grew by 2,203 Cr. in Q3 alone

- Active customer base crossed 50 lakhs in gold loan

- Achieved a growth of 22% in Gold Loan AUM over the 9 months; by March21, AUM growth may stand at 25-26%

- Disbursed gold loan to:

a. 3.88 lakh NEW customers amounting to 2796 Cr.

b. 4.38 lakh INACTIVE customers amounting to 2960 Cr. - Standalone PAT – 2,726 Cr. for these 9 months with a 24% y-o-y increase

- Gold Holdings – 166 tons

- Consolidated PAT – 2,795 Cr. for these 9 months with a 20% y-o-y increase

- Added 150 branches for this year; total branch count – 5417

- Home Finance business reduced AUM

- Muthoot Best(microfinance) grew by 2880 Cr. (as compared to 2285 Cr. last year)

- Collections in Microfinance at 98%; whereas in Homefinance at 88.7%

- Muthoot Insurance 9M Profit of 12 Cr.(as against 5 Cr. last year)

- Muthoot Sri-Lankan subsidiary reported profit of 1331 Cr.( as against 1301 Cr. last year)

- Muthoot Money(Vehicle Finance) has AUM at 421 Cr.; shrunk by 42 Cr.; recovery at 83.8%

- Share Capital/Net Worth reached 14,178 Cr.(vs 11400 Cr.)

- Healthy CAR ratio – 26.38%

- Employee count remains stable at around 25,800. Able to increase business without a proportionate headcount increase.

- Public issue of Non-convertible Debentures raising 2,000 Cr. during Dec,2020.

Analyst Questions: - Loan growth target going into FY22 – min. of 15%

- LTV as of Dec’20 – 67%(with accrued interest); Incrementally, it should be in the range of 68-70%

- Avg LTV tend to increase over a period of time due to gold price fluctuations; however, it will never cross 25%(as highest LTV is 75%)

- Gold Loan Stage 1, 2&3 – 98.21%, 0.4%, 1.3%, respectively

- Stage 3 is based on 90day dpd; doesn’t include Supreme Court order

- Provisions – 73.39 Cr.

- Avg. Yields – 22%

- Gold AUM geography-wise share – South:49%, North:23%, West:19%, East:9%

- Avg. Ticket Size –70,000 INR

- Greater than 3lakh ticket size: 22% of overall portfolio

- Reasons for high cash balance – High AUM Growth, RBI’s LCR target and NBFC fund crisis

- Avg. cost of funds – 8.45%

- Incremental cost of funds – Bank: 8%, NCD: 7.5%, Overall, its near to 8%

- Increase in Other Income – Insurance claim of 8Cr. due to a past burglary incident and some recovered write-offs

- Increased Competition – No pressure on yield; Gold Loan customer base is increasing overall in India with more acceptance by new customers

- Funding from Commercial Paper decreasing? - Company is trying to move to longer sources of funds to maintain balance sheet stability as AUM is growing

- Muthoot doesn’t need any intermediaries as it has rich customer contacts and deep reach

- Primarily, Provisions have increased due to increase in overall AUM

- Avg. ticket size has grown up from 35,000 to 50,000 due to increase in gold prices

- Stage 3 provisions for Q3 – 73 Cr.; Stage 3 provisions for Q2 – 59 Cr.

13 Likes

May his soul RIP!