Company successfully priced a USD 550 Million Fixed Rate Senior Secured Note for a 3.5 year tenor at 4.4%. The final order book was in excess of USD 1.6 Billion with over subscription of more than 2.9x. The transaction witnessed 38% participation from Asia, 13% from Europe and 50% from US; with 89%

investments from fund managers, 6% from private banks, 3% from insurance & banks and 2% from

others.

M.G.George Muthoot, Chairman, on this issue stated:

“The response from international bond investors in our second issue is quite overwhelming. We are glad to know that global investors have understood our unique credit story acknowledging our long track record in gold loan business. This is a recognition of India’s NBFC sector. This fund raise will enable us in further diversifying and strengthening our > sources of funding. We look forward to strengthening our partnership with global investors”

Trying to gauge the impact of the recent market correction on the business

Will premature diversification negatively affect the NPAs?

We have seen the gold loan business growing at 2-3% rates of late. Will the economic slowdown boost the gold loan segment? Another moot point here is what will happen to the gold loan business once the economy starts recovering? Well in that case, investing in this company is more like taking a contrarian view on economy.

What are the growth prospects of Muthoot in the near future? Can somebody share notes on what has been the growth/branch?

Going by the hit MFI stocks have taken (Bandhan, equitas etc.) growth in the MFI subsidiary also looks bleak. Coupling this with a stagnating gold loan book, I feel the stock is in a precarious position.

I went through a detailed explanation of how the company navigated a turbulent 2013 crisis. But the magnitude of current crisis CANNOT be compared to the one in 2013.

Invite comments from experienced folks in this space.

Disclosure: Just started investigating the company and I hold no shares

Hi, thanks for your post, helped me revise the numbers of the company.

88% of loan book is from Gold loans. Wouldn’t call it premature diversification.

Company demonstrated 26% growth in sales in 9 months FY20. Why do you call it 2-3%? Also, gold loans grow well during economic booms as well. Lots of gold loans are working capital loans of micro-entrepreneurs.

Management has been guiding base case as 15% growth in their conf calls.

Discl: Invested in Muthoot Finance. Added to my portfolio just today morning. This is not a buy / sell recommendation. Please do your own research.

StockAdda has the conference call recordings.

Pasting my notes down here from those recordings, in case you are interested:

Conf Call Q3FY20:

Highest every quarterly growth achieved in last 7-8 quarters. Growth of 19% in AUM.

Seeing very good growth since Q1. Had to slow down in Q2 due to resource constraints. Recovered now in Q3 and Q4 also going good.

Higher impairment due to burglary. Filed for insurance claims. Policed already recovered some amount.

We guide minimum 15% growth.

We plan to maintain higher liquidity than before after going through the NBFC crisis.

Rating update is long overdue for Muthoot Finance. It will bring lots of benefits when that materializes.

We are looking to expand by 100-200 branches per year. However, we are more focussed on per-branch business where are already about 2x our competitors.

Incremental cost of borrowing for us is 9.1%. Average cost of borrowing is around 9.2% and can go upto 9.5%.

We offer homes loans through existing branches and also on-ground sales staff.

LTV of gold is 61% as of Dec 31, 2019. At stable price level, it is 70%. Due to the fast rise in Gold price, LTV fell to 61%.

60% of our portfolio is repaid in first 6 months itself. 10% repay in the first month. 32% repay in second month.

No industry wants to setup factory in Kerala. Kerala has been notorious that way. Some service industries are somehow managing. Our exposure to Kerala is only 3% for now.

We don’t see the need for so many branches in Kerala. We have about 800-900 branches already in Kerala. All these were opened before the massive tech adoption by the country. We are looking to close some of these branches now.

Conf Call Q2FY20:

Consolidated Loan AUM up 13%.

We have 24 crores investment in Nepalese company. They want to do Gold loan business and we are helping them in that.

All our AUM is on bullet payment of one year. Customer has the option of paying at monthly, quarterly frequency.

Q1: 9.17%, Q2: 9.3% and H1: 9.26%. This is because we are getting some borrowing from foreign exchange borrowers.

Going forward, we should expect yield of 21.5%.

Kerala contributes 3.4% of our total portfolio.

Auctions were of 58 crores.

GNPA of gold loans shouldn’t be worrying. It just means that the customer has given us gold 15 months old. We don’t loose money in GNPA of gold loans.

Being cautious due to NBFC crisis last year. So we grew slowly this quarter and waiting to get more resources.

Average home loan size is 10 lakhs. We don’t do any LAP. We don’t do any builder financing.

NPAs in home loan business has risen from 0.8% to 1.1%. This is due to poor economic growth in the country and poor people are losing jobs.

Our average LTV is 60%.

This quarter, we had a burglary and lost gold. We wrote that off and also claimed insurance. As prudent measure, we wrote that off and write it back as income when we receive our insurance proceeds.

Advertising will go up in the next two quarters once we receive funding and as we also expect high growth in those quarters.

I think we will not leverage more than 5x.

Discl: Added to my portfolio last week. Not a buy / sell recommendation. Please do your own research.

I don’t have such detailed write-up for Muthoot. IndiaMart was my first and only (so far) attempt at that Deep dive template.

Due to time constraints, I plan to write up such deep dives only for small cap / newly listed companies due to lack of history one can learn from.

If you are seriously interested in Muthoot, please feel free to give an attempt to writing that yourself. There are lots of insights in the conf calls of Muthoot and Manappuram. You can learn from there. Or we can connect offline for any discussion.

Hey guys

I was renewing the thesis for investment in Muthoot finance. Overall, there are a lot of great components to this business (as mentioned earlier in the thread). However, while analysing the regional spread for Muthoot and Mannapuram, I discovered that there might be quite a headwind towards growth in future. Sharing here for feedback from community for thoughts and critique.

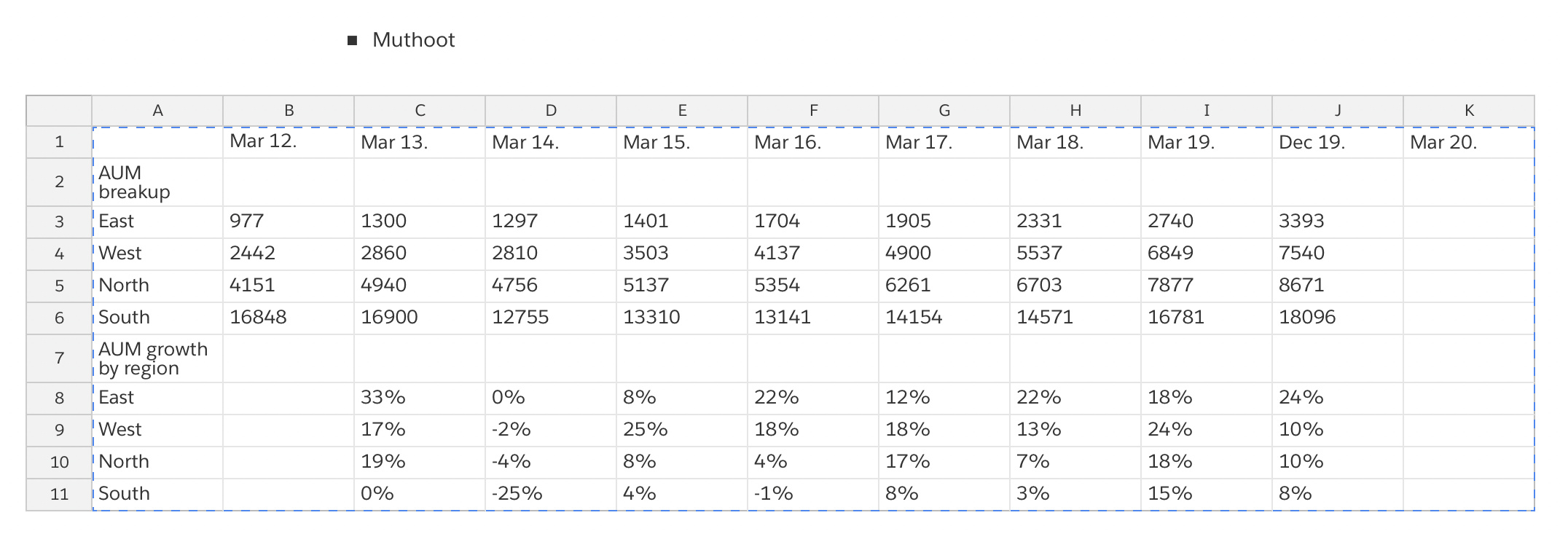

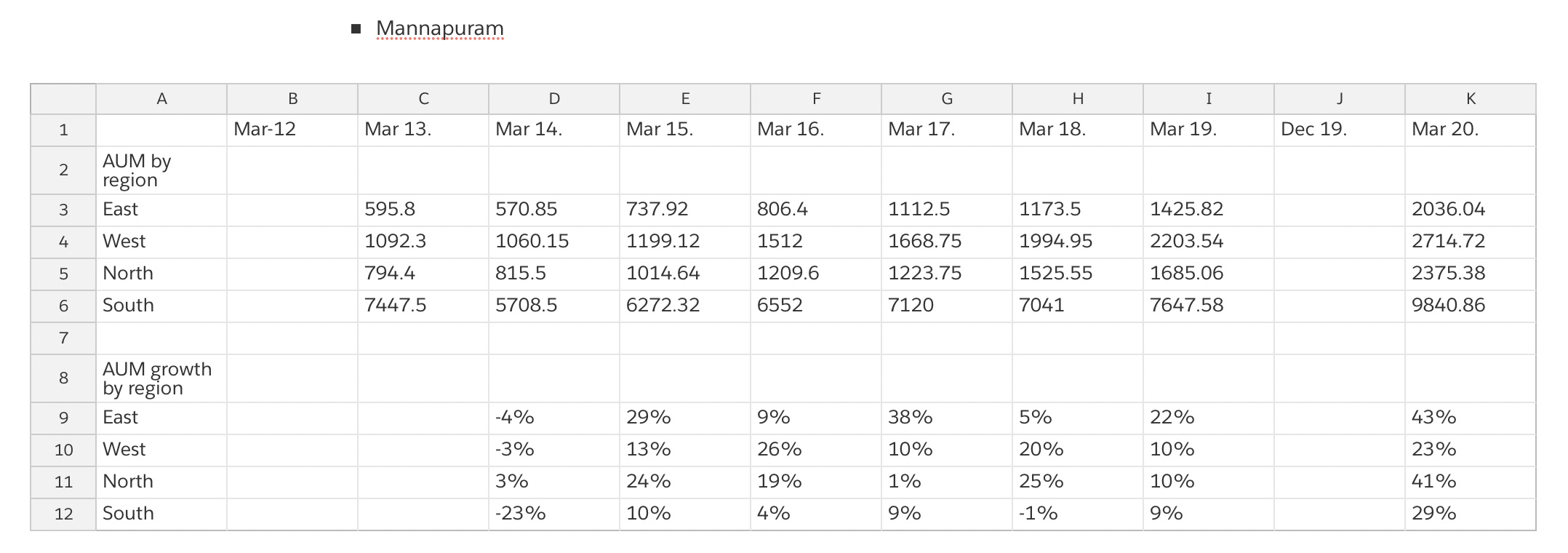

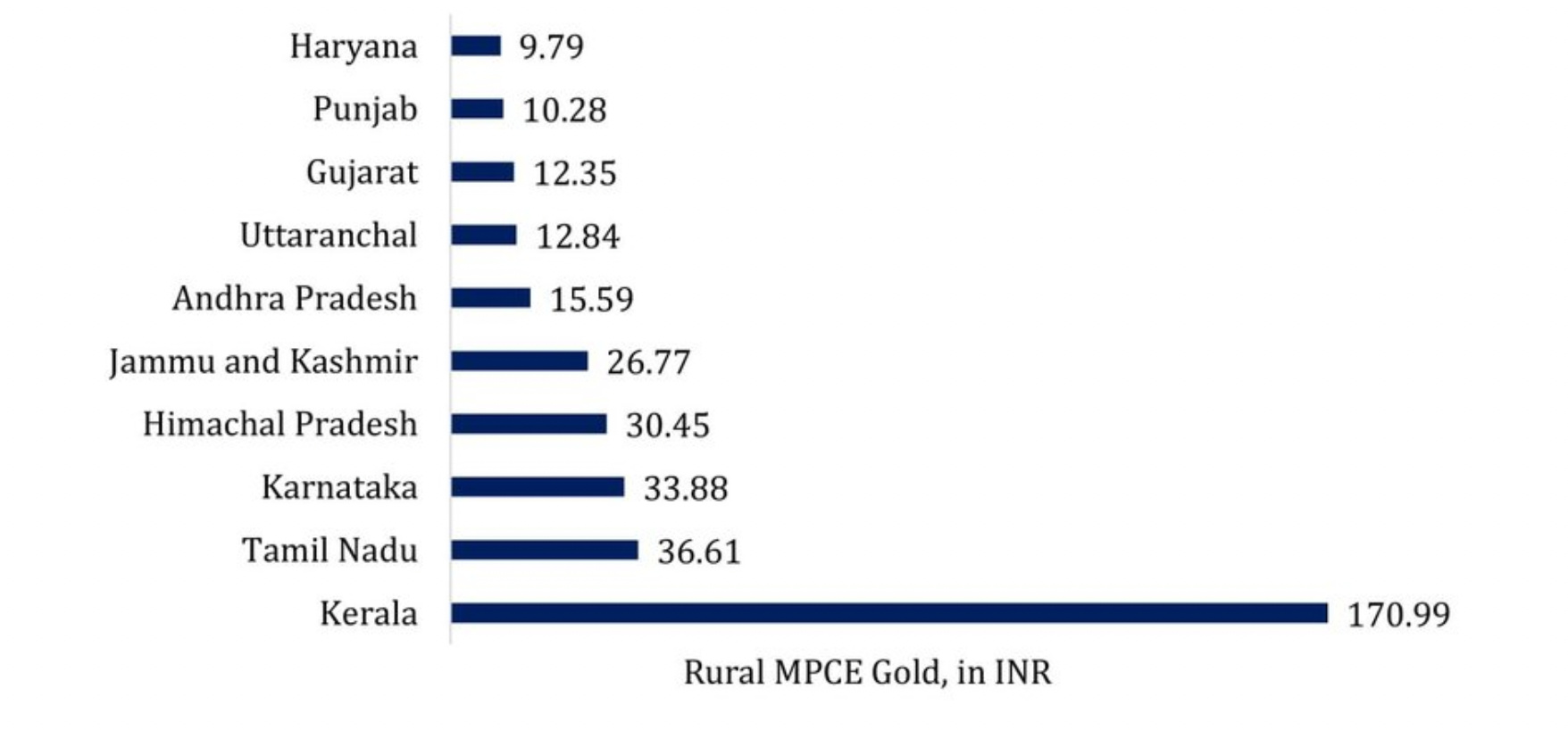

Here is regional growth of Muthoot and Mannapuram over last 8 years split by region. Along with that I have uploaded a chart showing monthly per capita expenditure on gold by states.

Looks like south book is stagnant and caught up with 2013 levels only last year. And the book growth seems to be quite related to gold price movement. Largely growth is coming from West, East and North.

The per capita expenditure on gold tapers down quickly after few Southern states. Other research on internet suggests that South accounts for 40% of overall gold demand.

If we assume that other regions would also achieve same level of penetration as south, we can see that non southern regions have potential opportunity to grow to contribute 60% of overall book. Which means

North/East/West growing by 40% from current levels.

Beyond that the book growth would be driven by a. Growth in gold demand b. Increase in prices for gold.

Essentially it appears that beyond this growth that I talked about for non southern regions, this is more of a bet on gold prices and a secular growth on the consumer demand.

The bigger picture is that what happens when most NBFCs, PSU Banks and some private sector banks cant expand their balance sheet (no more incremental lending) then share of gold loan in bridge loan segment (less than 1 year short term duration loans) may increase disproportionately.

counter to above argument is what if some biggie like bajaj finance enters the sector.

so there might be growing pie of gold finance business but with higher competition.

but valuations are not demanding at all and size of opportunity may be too large for everyone.so keep tracking actively. there might be some re-rating of valuation upwards from here.

Muthoot finance Price has doubled from the day message was written. Feel that it still has a long runway:: Factors helping stock price and business of this company are as following

a) Distress times for business -people take more gold loans ( check the years after demonetization, gold loans increased by 30% per annum ).The current period is more distressful than demonetization

b) No NPAs, increasing gold prices make sure that old loan takers come back to pay the loan to take their gold back

c) Increased gold prices also encourage people to take a higher amount of loan with the same quantity of gold

d) St0ck is getting split - whatever be the ratio- it would become available to more number of retail investors (especially the ones who relate high stock price to high valuation)

Feel we are in early days of the bull market in Muthoot Finance

Disclaimer: Invested, it is number 2 in the portfolio.

Positive for banks . However the nbfc’s giving gold loans should not get affected as the dynamics of gold loan like - time taken to disburse gold loans and the lower amount of loan, which a nbfc does easily - will not be viable for banks.Also the relaxation is only till March 2021.

A tweak such as this, is actually a double edged sword.

With increased LTV, Muthoot (and other gold loan providers) can of course lend more against the same collateral, which theoretically can mean bigger ticket size, higher disbursal, bigger loan book and more interest income, and this is a very positive scenario.

Things however start going bad, if the gold prices drop in short span of time (say 6 to 12 months). With LTV of 90%, if gold prices drop more than 10%, then the borrower has no incentive whatsoever to repay and close the loan, since the collateral value is now lower than what he borrowed. So if he simply defaults, he will pay less. The lender, even if they auction the gold, still stands to lose on the loan value, depending on when exactly the default happens in the loan cycle, which of course is not a good scenario for financial performance or stock price.

Though most macro indicators overwhelmingly point to the fact that gold will continue to rise in near future, a trend reversal cannot be ruled out. If the reversal is sudden and rapid, it can pile up pressure in the short term.

In fact, if we see historically, something similar happened in 2012 - 2013, when gold prices fell by more than 20% and all gold loan companies landed in a mess. The current RBI regulations around gold loan products, including the LTV were laid down and enforced around then. Muthoot had to reduce its book drastically by about 20% over the next 3 years, before rebuilding the growth again.

So, my personal view is that higher LTV can introduce a mild element of NPA risk in a business, which currently is almost risk free, as far as NPAs are concerned. Not aware of the nitty-gritty in regulation around LTV, but it would be prudent for Muthoot (and other NBFCs) to continue capping their LTV at levels lower than 80%, if the regulation allows them to do, especially given the current fragile economic scenario.

In these times, focus should be on balance sheet / capital protection not on aggressive expansion. RBI has of course tweaked this to encourage more capital / liquidity to masses, specially those who do not have an access to formal banking system.

The higher LTV rule is applicable to banks only and that too till 31.03.2021. The idea is to improve the net NPAs of banks. But it is an injustice on NBFCs like Muthoot and Manappuram, as their cost of borrowing is already higher and now they have to work with existing LTV of 75% vs 90% allowed to banks. Nevertheless the demand for gold loans would be very high. So Muthoot and Manappuram can still log in 15 to 20% of growth. In terms of professionalism and speed, Muthoot compared to other gold security lenders is what HDFC is to other housing finance companies. Gold has not peaked as yet as the US- China cold war and Covid pandemic scenario would take some time to normalize. So Muthoot & Manappuram would be riding smooth for another 6 months.

Yes I agree- I don’t think banks would be getting any substantial benefit out of this step, that too only for few months. Besides the gold loan forms a very small percentage of bank loans . Also the ticket size and time for loan disbursal is against what banks do .

Has Bajaj finance lost business due to banks giving loans. Banks cannot Match the franchise model of Bajaj finance . Right.

Higher LTV is definitely beneficial for banks, however Gold loans are a very operationally intensive and trust-centric business and therein lie the moat of a Muthoot Finance. I am not sure how much banks will be willing to invest in this business to capture market share from gold loan NBFCs other than in the current environment where it is one of the few avenues to lend safely. That being said, as an investor in MF, I would love to see higher LTV — I don’t agree that if Gold prices fall the customer will walk away from the loan, remember: his collateral is not some off the shelf item but generally family jewellery that has immense sentimental value.

Recently wrote about moats of gold loans NBFCs here.

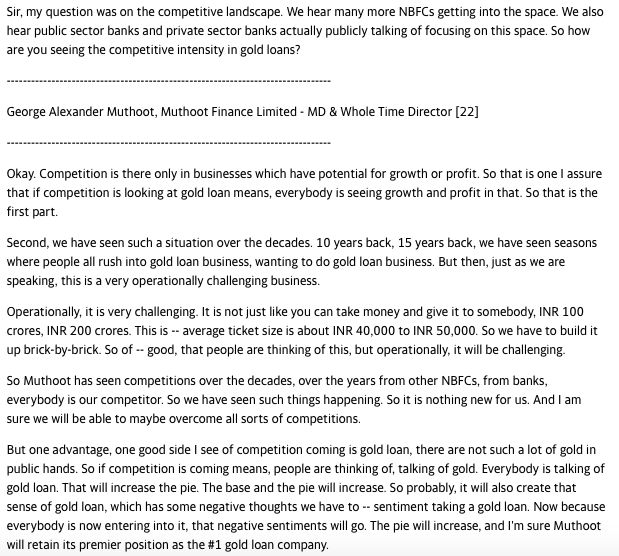

Mr. Muthoot on competition from banks in the last con call -

Currently the average LTV of Muthoot is around 58 %, whereas Mannapuram commands average LTV of around 62 %.

Banks, on the other hand has been on a lower side of this band with LTV of around 45 - 50 %. As put forward by you, the increase in LTV is like a double edged sword. Increasing the LTV by RBI doesn’t necessarily mean the banks are going to take that additional risk of going up to the brim, which if they do, might peak the NPA risk in their books.

And, given the penetration Muthoot/Mannapuram enjoys in Tier II and Tier III cities, I don’t perceive the change LTV for the banks can have any meaningful impact in these two gold loan franchisees.